CF Benchmarks

At CF Benchmarks we pride ourselves on providing implementable solutions that drive product innovation, efficiency and robust risk management. See the below case study of how striking NAV to our Bitcoin index, the CME CF BRR simplifies deployment, liquidity management and creation/redemption processes.

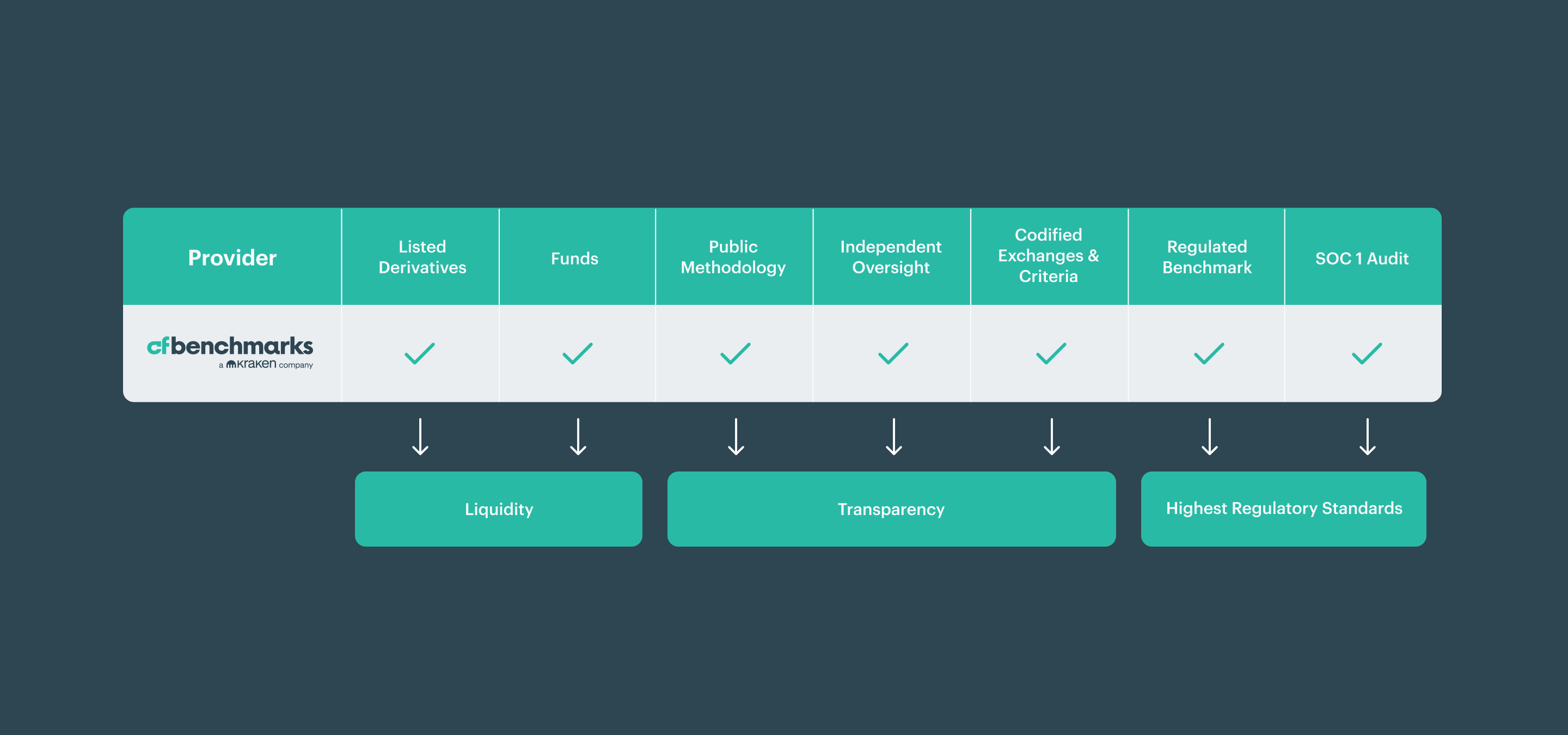

Regulatory certainty

Our CME CF BRR and CME CF Ether digital asset benchmarks strike NAV with our crypto ETF indices for ETFs & ETPs listed in Europe, US, Canada, Brazil, Hong Kong and Australia. Take a look at our ETF & ETP Tracker.

Replicability Minimizes Tracking Error

BRR methodology is replicable with limited slippage- OTC dealers guarantee executions to CME CF BRR at a spread.

Consistent Liquidity - On Tap

CME BTC-USD Futures & Options act as a liquidity rail for the trading of ETF shares tracking BRR due to usage of the same index.

More than just a number

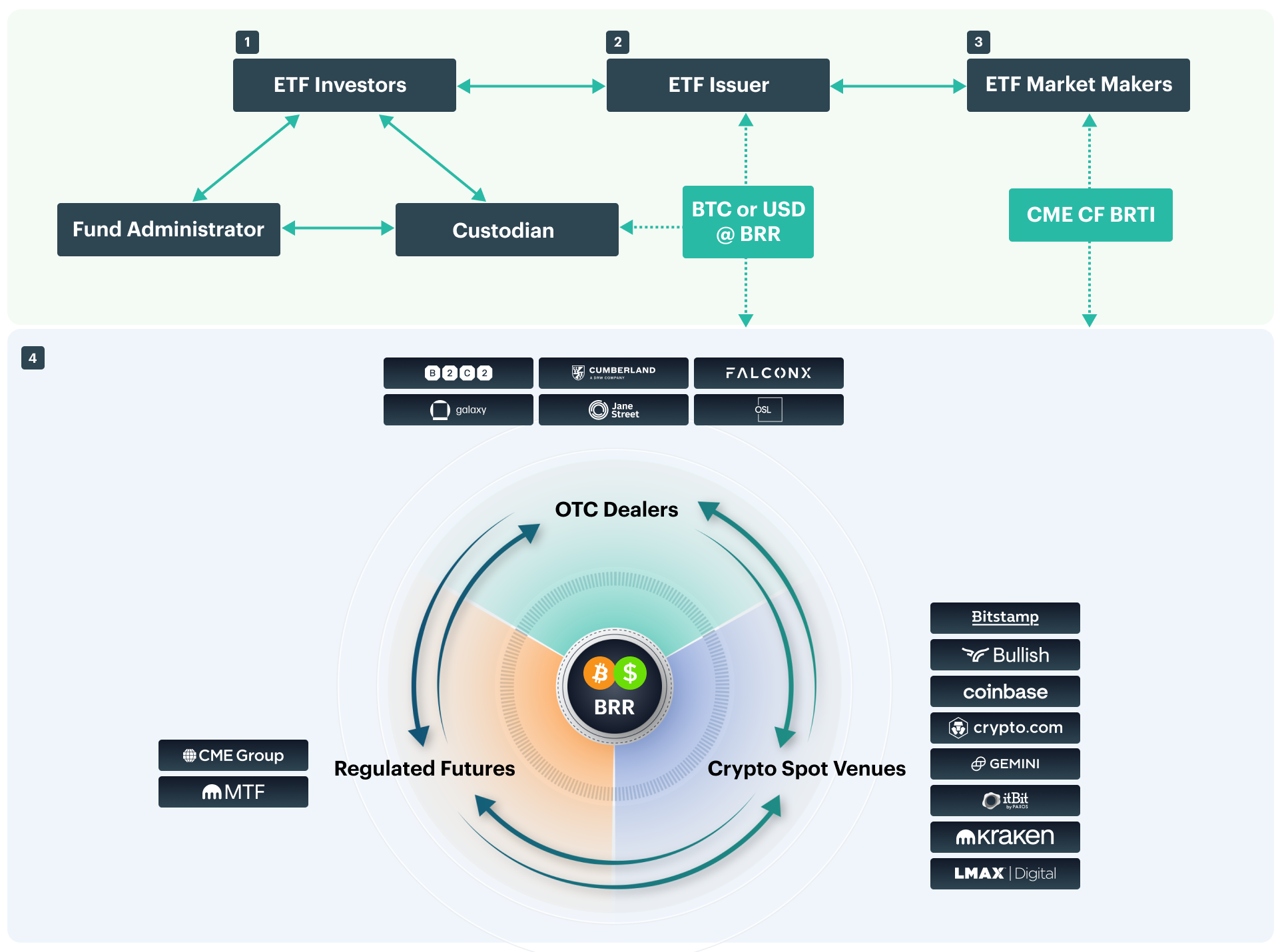

The BRR liquidity complex ensures perfect tracking and abundant liquidity.

The CME CF BRR ties the spot markets to the regulated futures markets, creating a powerful liquidity complex that ETF issuers can rely on to ensure orderly creations and redemptions of ETF shares. Managers can buy and sell Bitcoin through major OTC dealers at the CME CF BRR with abundant liquidity, ensuring perfect tracking and eliminating NAV drift.

- ETF investors have full visibility on fund NAV and crypto holdings from regulated providers.

- ETF issuers can buy and sell Bitcoin through major OTC dealers at the CME CF BRR with abundant liquidity, ensuring perfect tracking and eliminating NAV drift.

- ETF market makers use the spot Bitcoin market through the once-per-second CME CF Bitcoin Real Time Index and regulated futures contracts as a liquidity rail to ensure liquidity in ETF shares

Learn more

Learn More about CF Benchmarks Portfolio Indices

Readily available data through major data vendors

CF Benchmarks provides key index analytics on its website in real time to give index users an up to date picture of price action dynamics and volume flows.

CME CF BRR is published and disseminated through major vendor platforms

- Bloomberg: BRR GO

- Refinitiv: .BRR

- CME MDP and DataMine

Highlighted products

CF Large Cap Index

CF Large Cap IndexThe CF Large Cap Index (CFFLCLDN_RR_TR) is a liquid investible benchmark portfolio index designed to track the performance of large-cap digital assets.

$LCAP The Large Cap Index DTF ($LCAP) is a fully collateralized token tracking the CF Large Cap Index and offers a transparent, efficient way to gain exposure to the index that brings the benefits of tokenization

The Large Cap Index DTF ($LCAP) is a fully collateralized token tracking the CF Large Cap Index and offers a transparent, efficient way to gain exposure to the index that brings the benefits of tokenization CME CF Bitcoin Reference Rate (BRR)

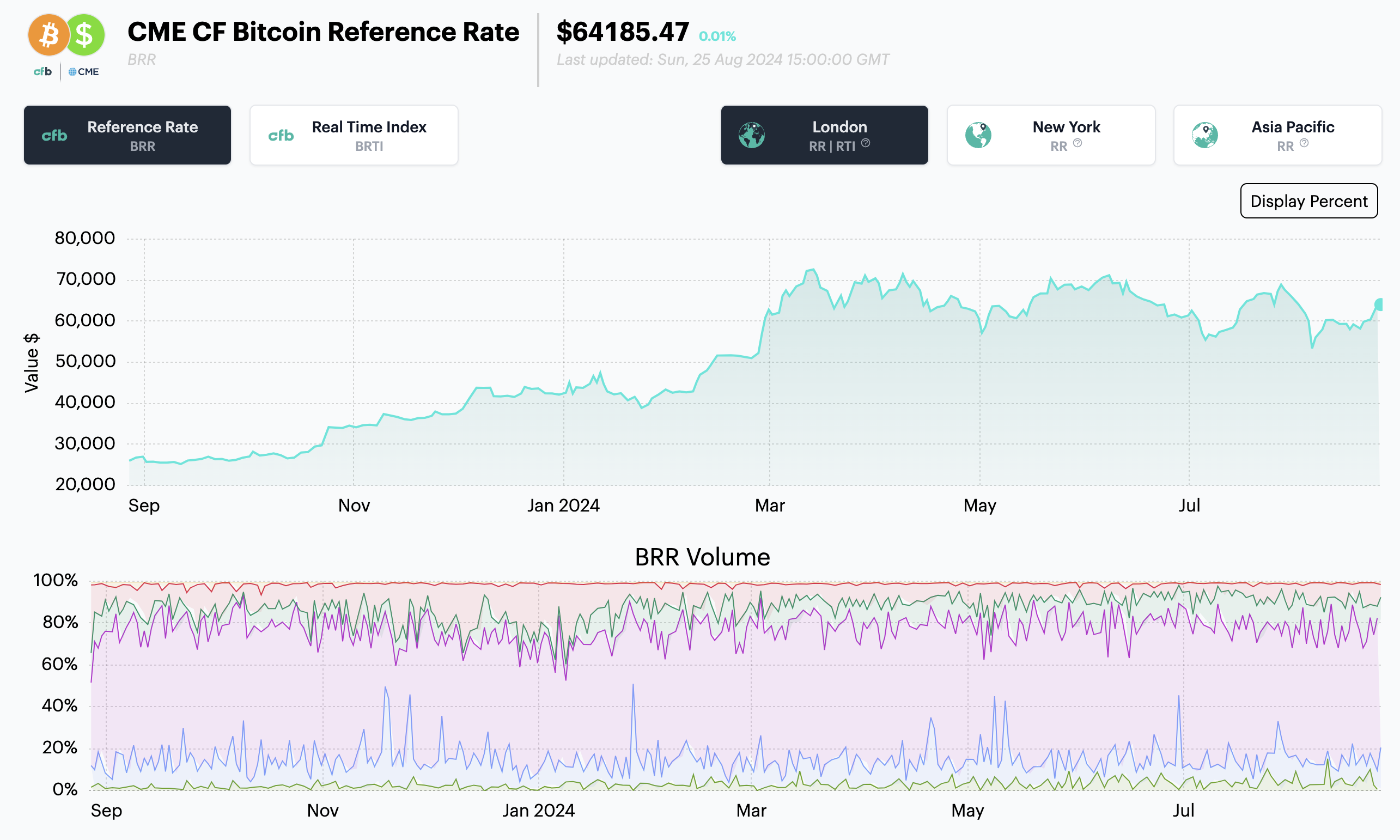

CME CF Bitcoin Reference Rate (BRR)The CME CF Bitcoin Reference Rate (BRR) is a once a day benchmark index price published at 1600 London time for Bitcoin that aggregates trade data from multiple Bitcoin-USD markets operated by major cryptocurrency exchanges that conform to the CME CF Constituent Exchange Criteria.

ETFs

BRR exposure is available through ETPs & ETFs offered by: CME CF Bitcoin Reference Rate - New York Variant (BRRNY)

CME CF Bitcoin Reference Rate - New York Variant (BRRNY)The CME CF Bitcoin Reference Rate - New York Variant (BRRNY) is a once a day benchmark index price published at 1600 New York time for Bitcoin that aggregates trade data from multiple Bitcoin-USD markets operated by major cryptocurrency exchanges that conform to the CME CF Constituent Exchange Criteria.

ETFs

BRRNY exposure is available through ETPs & ETFs offered by: CME CF Ether-Dollar Reference Rate

CME CF Ether-Dollar Reference RateThe CME CF Ether-Dollar Reference Rate (ETHUSD_RR) is a once a day benchmark index price published at 1600 London time for Ether that aggregates trade data from multiple Ether-USD markets operated by major cryptocurrency exchanges that conform to the CME CF Constituent Exchange Criteria.

ETFs

ETHUSD_RR exposure is available through ETPs & ETFs offered by:- CME CF Ether-Dollar Reference Rate - New York Variant

The CME CF Ether-Dollar Reference Rate (ETHUSD_NY) - New York Variant is a once a day benchmark index price published at 1600 NY time to synchronise with US equity market close for Ether that aggregates trade data from multiple Ether-USD markets operated by major cryptocurrency exchanges that conform to the CME CF Constituent Exchange Criteria. Index .

ETFs

ETHUSD_NY exposure is available through ETPs & ETFs offered by:  CF Bitcoin Interest Rate (BIRC)

CF Bitcoin Interest Rate (BIRC)The CF Bitcoin Interest Rate Curve (BIRC) is intended to measure the underlying economic reality of cryptocurrency borrowing and lending, whether outright or implied in traded instruments.

CME CF Bitcoin Volatility Index (BVX)

CME CF Bitcoin Volatility Index (BVX)The CF Bitcoin Volatility Real Time Index (BVX) is a once a second benchmark representing a forward looking, 30-day constant maturity measure of implied volatility based on CFTC regulated Bitcoin option contracts traded on the CME.

CF Broad Cap Index

CF Broad Cap IndexThe CF Diversified Broad Cap Index (CFDBCLDN_RR_TR) is a liquid investible benchmark portfolio index designed to track the performance of diversified exposure to a broad portfolio of the digital asset class.

CF Rolling CME Bitcoin Futures Index

CF Rolling CME Bitcoin Futures IndexThe CF Rolling CME Bitcoin Futures Index (CFCMBTCF_BTC) is a means of replicating the USD returns of holding physical Bitcoins through Bitcoin-USD futures contracts that allow investors to seek USD price exposure to Bitcoin.

CF Staking Series

CF Staking SeriesThe CF ETH Staking Series and CF SOL Staking Series serve as a transparent and representative indicator of the daily realised reward associated with the staking of digital assets. They serve investors in providing an accurate measure of the economic incentives associated with a specific PoS network.

CF Digital Asset Classification Structure (CF DACS)

CF Digital Asset Classification Structure (CF DACS)The CF DACS classifies coins and tokens based on the services that the associated software protocol delivers to end users, grouping assets by the role they play in delivering services to end users.

Selective Rotation Drives Wider Sector Dispersion

Digital assets fell as a bloc while individual tokens pulled violently apart. Index moves stayed clustered even as constituent dispersion widened. Defensive factors failed to defend, stress sat in the long tail, and implied volatility gave up its event premium as funding dislocated at the front end.

Mark Pilipczuk

Mark Pilipczuk

10 mins read

Factor Friday - July 31, 2026

July's rally has stalled, with the Market factor flat at +0.02% and its four-week gain down to +0.48% from +7.13%. Momentum led a second straight week at +1.96%, its first back-to-back run since late May, while Growth reversed to +1.74% and Value fell to the bottom at -1.93%.

Mark Pilipczuk

Mark Pilipczuk

8 mins read

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Mark Pilipczuk

10 mins read

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.