Feb 03, 2026

Policy Paralysis, Fed Fog & Shutdown Risks Extend Sell-Off

Key takeaways for the month

The year kicked off with heightened macro and geopolitical uncertainty that weighed on digital asset risk appetite. While the Federal Reserve held rates steady, attention quickly shifted to leadership risk as President Trump announced Kevin Warsh as the next Fed chair, which introduced uncertainty around the the potential for future rate cuts and the central bank's reaction function. Bitcoin traded defensively, consolidating near the lower end of its recent range before continuing to sell off into month-end. Regulatory momentum slowed at the margin as crypto legislation stalled out, and geopolitical tensions further dampened sentiment, reinforcing a risk-off posture. With policy clarity delayed and macro data distorted by geopolitical and seasonal effects, investors de-risked, liquidity thinned, and conviction remained low across higher-beta tokens as markets awaited clearer signals on monetary and regulatory direction.

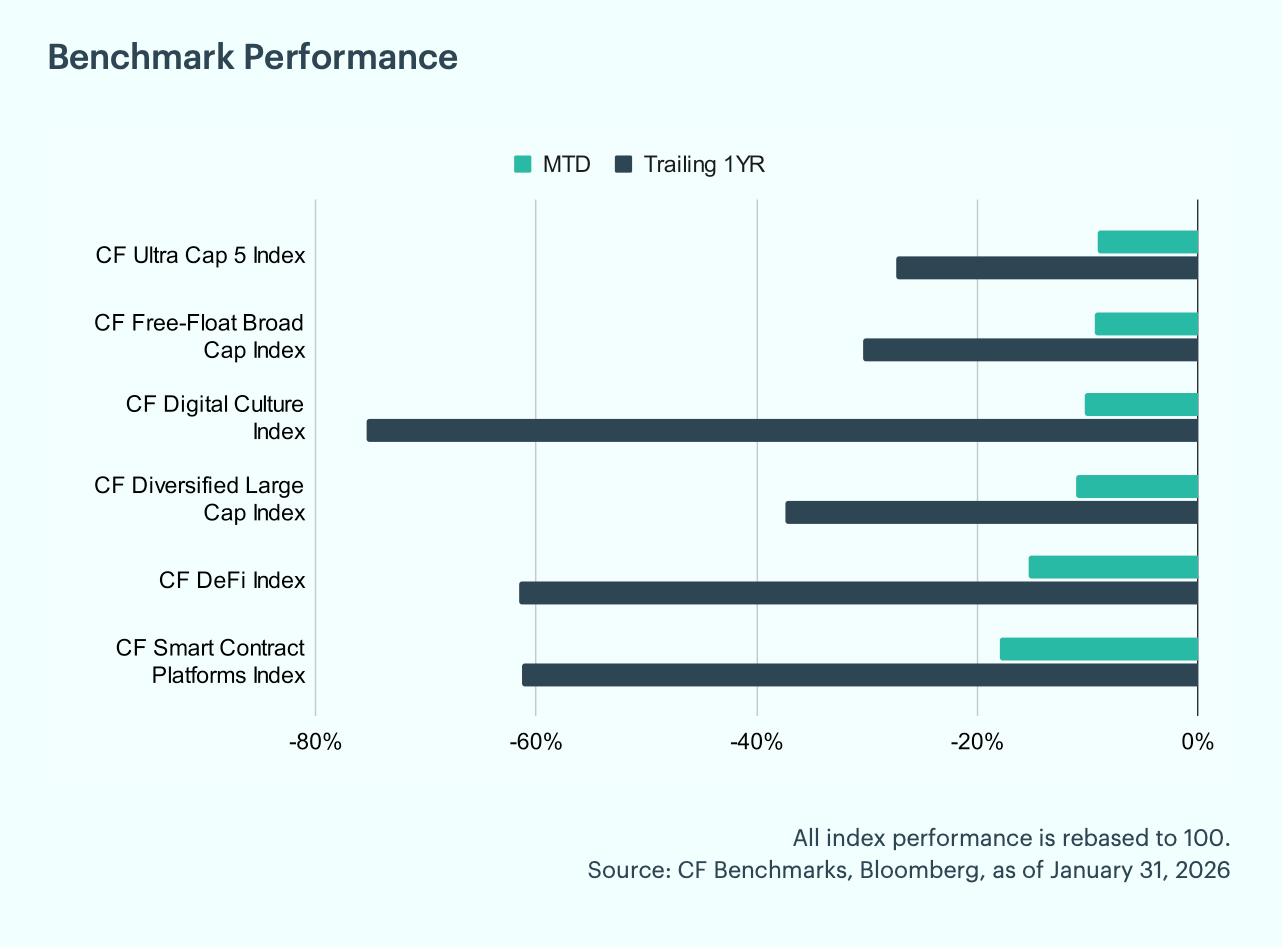

Risk-Off Rout Deepens: January 2026 extended the late-2025 drawdown, with digital assets broadly lower amid a risk-off backdrop. The CF Ultra Cap 5 and CF Free-Float Broad Cap indices each fell 9% month-to-date, while the CF Diversified Large Cap Index declined 11%. Higher-beta segments underperformed materially: the CF Smart Contract Platforms Index dropped 18%, the CF DeFi Index fell 15%, and the CF Digital Culture Index lost 10%. On a trailing one-year basis, losses remain severe across speculative cohorts, with DeFi and smart-contract platforms down more than 60%. The pattern reinforced investor preference for liquidity and network fundamental strength, as positioning stayed defensive and leadership remained narrow.

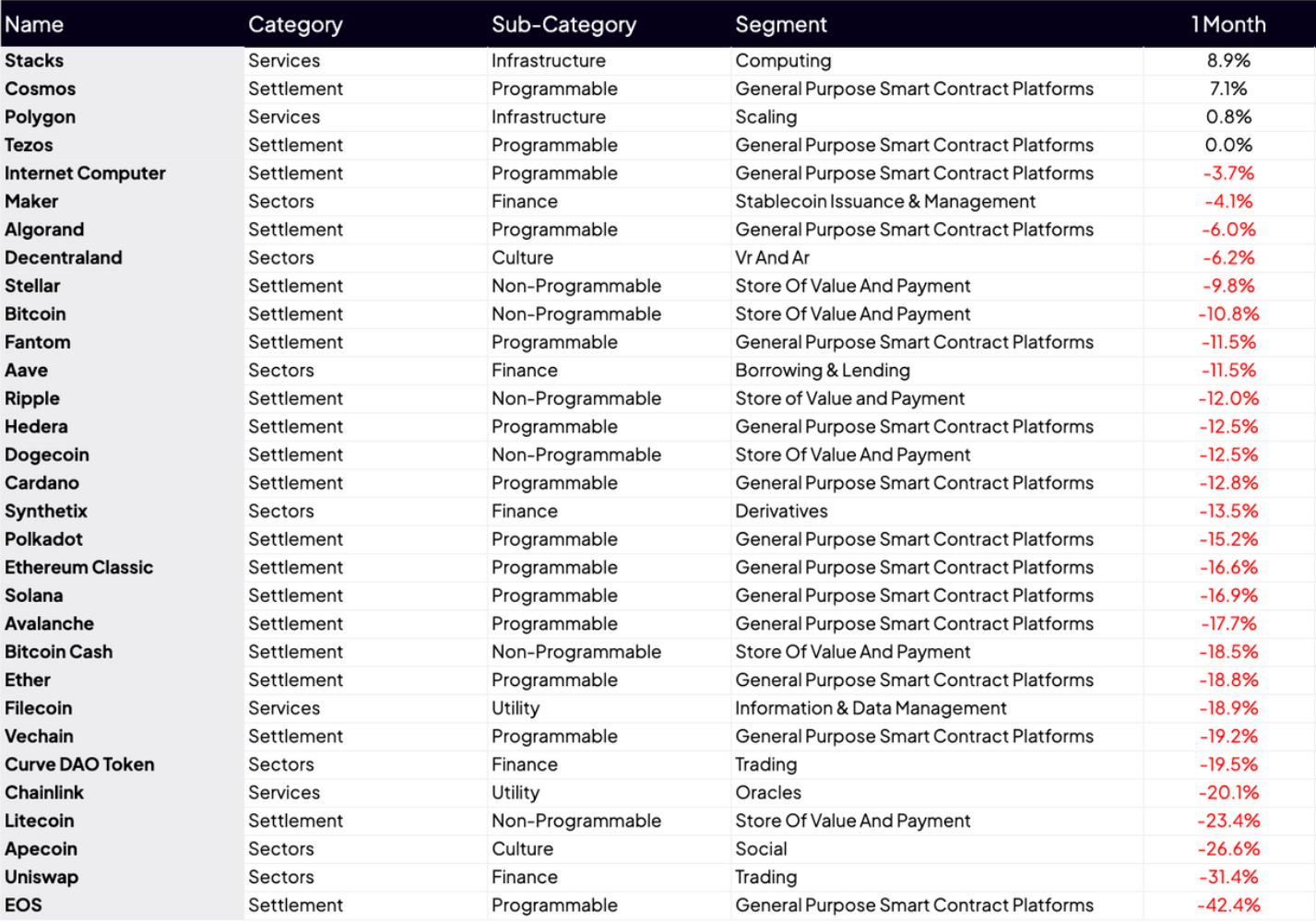

Individual Movers: Stacks (STX) led January's major crypto performers with an 8.9% gain, driven by an early-month Bitcoin Layer-2 rally and hints of institutional adoption. Cosmos (ATOM) followed at +7.1%, lifted by critical tokenomics reform proposals ahead of the mid-month deadline. Polygon (POL) held resilient with +0.8%, supported by soaring transaction volume and AggLayer unification progress. EOS trailed January's majors with a -42.4% plunge, hit by persistent ecosystem stagnation and zero meaningful updates. Uniswap (UNI) followed at -31.4%, pressured by collapsing DEX volumes in risk-off conditions. Apecoin (APE) rounded out the laggards with -26.6%, suffering ongoing NFT/metaverse apathy.

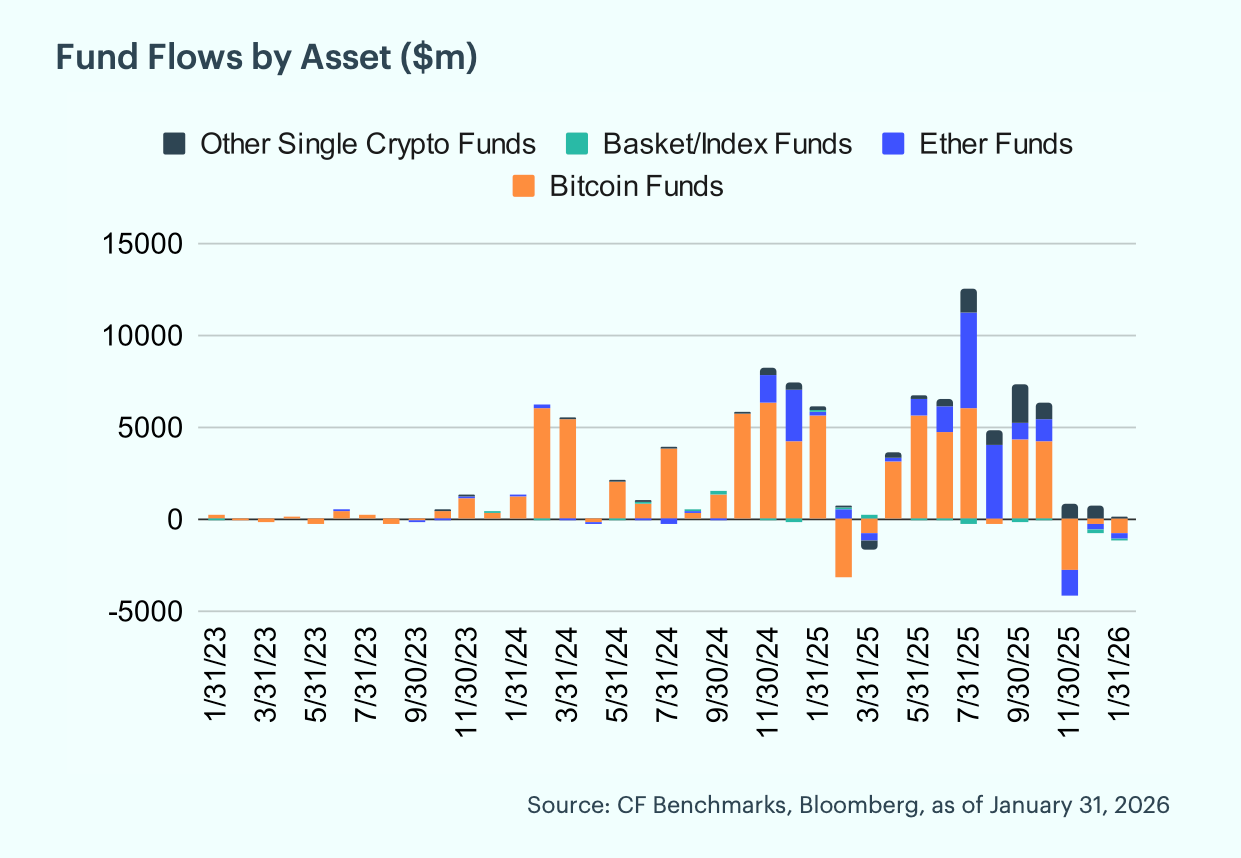

Outflows stabilizing: January recorded significant outflows from digital asset funds, with investors redeeming approximately $1.0 billion. Bitcoin funds accounted for the largest share at $720 million, while Ether funds followed at $370 million. Basket/Index funds saw an additional $64 million in outflows, partially offset by $140 million in inflows to other single crypto funds. Regionally, North America drove the majority of redemptions at roughly $47 million, while Europe experienced substantial inflows of $194 million, suggesting a marked shift in sentiment with selling pressure easing in U.S. markets while European investors added exposure.

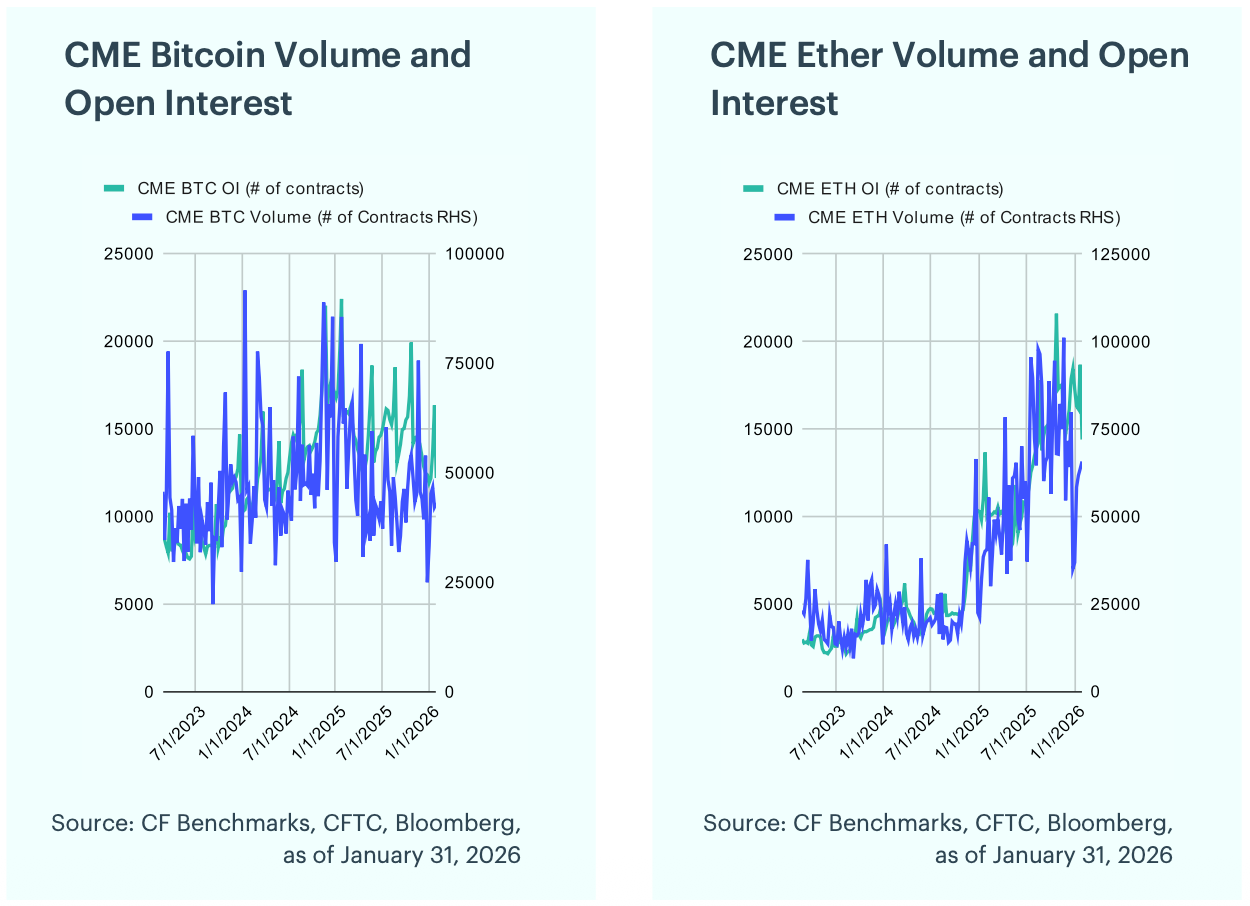

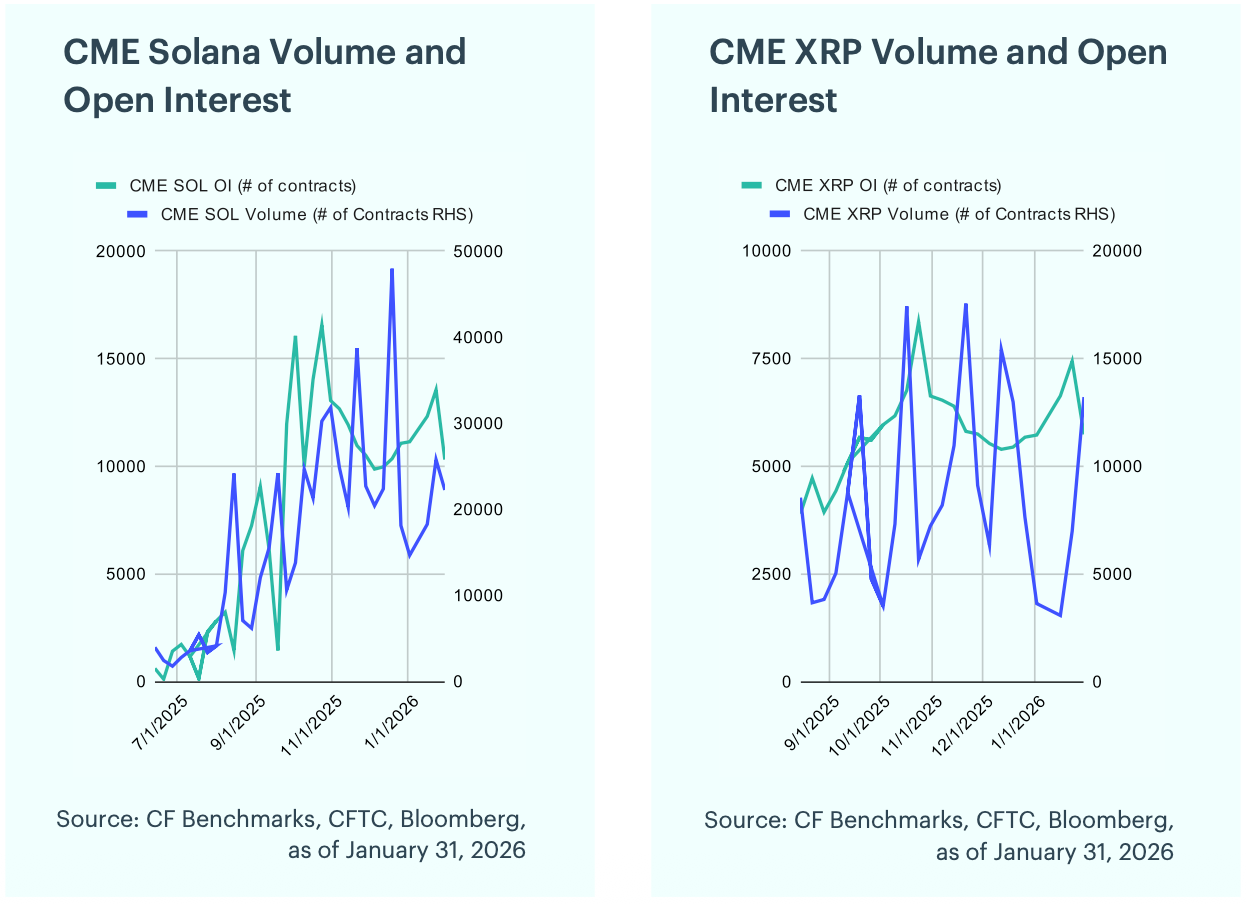

Futures Positioning Shifts with ETH Unwinds, XRP Builds: Bitcoin futures saw a modest decline in open interest during November, falling 11.7% from 14,029 to 12,383 contracts. Ether futures recorded a notable increase, with open interest rising 14.9% to 18,452 contracts, despite a modest decline in trading activity that peaked at 79,818 contracts toward month end. Meanwhile, Solana and XRP futures posted smaller changes following November’s pullback. Solana’s open interest rose 5.3% to 11,067 contracts as volumes approached 48,000 contracts, while XRP’s open interest declined 1.3% to 5,671 contracts, with volumes edging modestly higher.

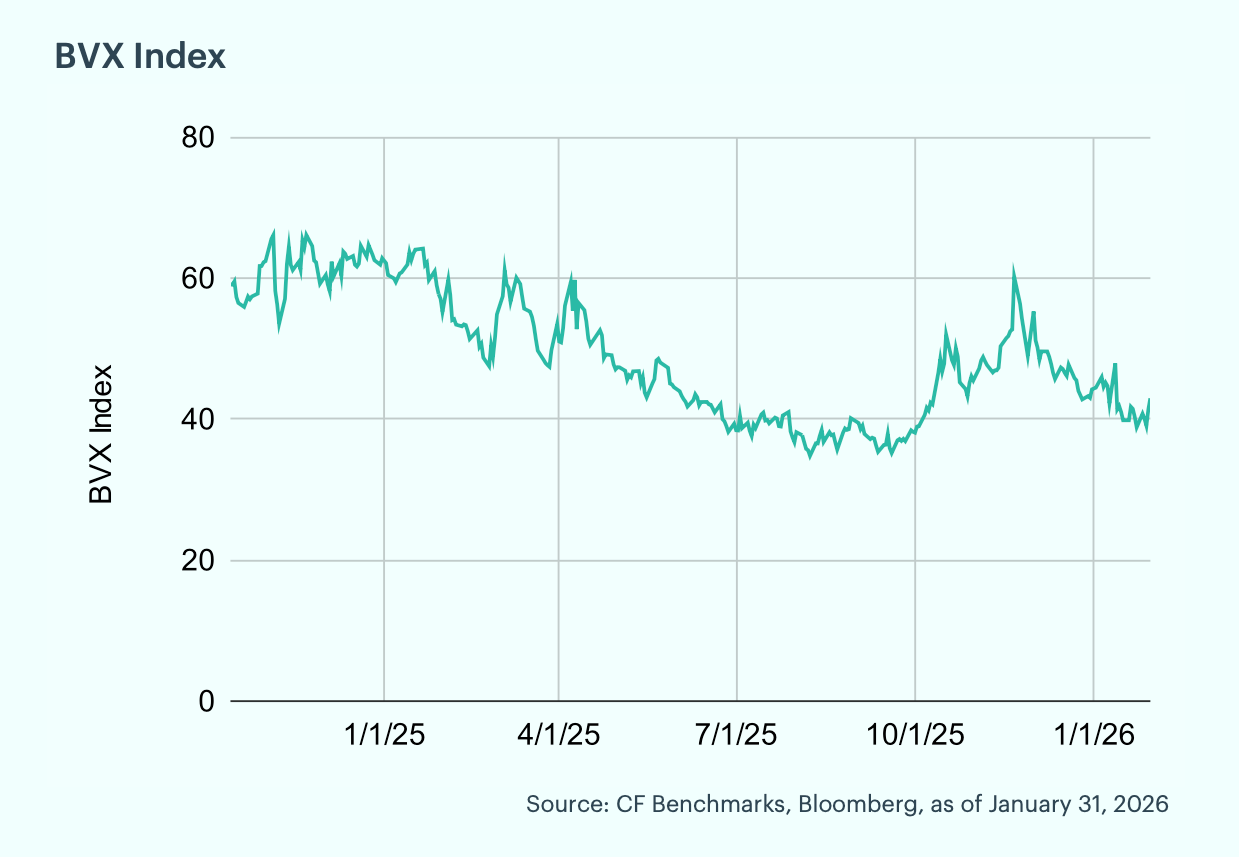

Bitcoin Volatility Continues to Compress: The CF Bitcoin Volatility Index Settlement Rate (BVXS) is a daily benchmark that provides a forward-looking, 30-day constant-maturity measure of implied volatility, derived from CFTC-regulated Bitcoin option contracts traded on the CME. The BVX reflects the fair strike of a variance swap. Over the past month, the BVX ranged between 38.82 and 47.89. During this period, volatility declined significantly, with the BVX recording a -2.1 sigma move (based on our rolling 30-day z-score) mid-month before moderating to close January at 42.94.

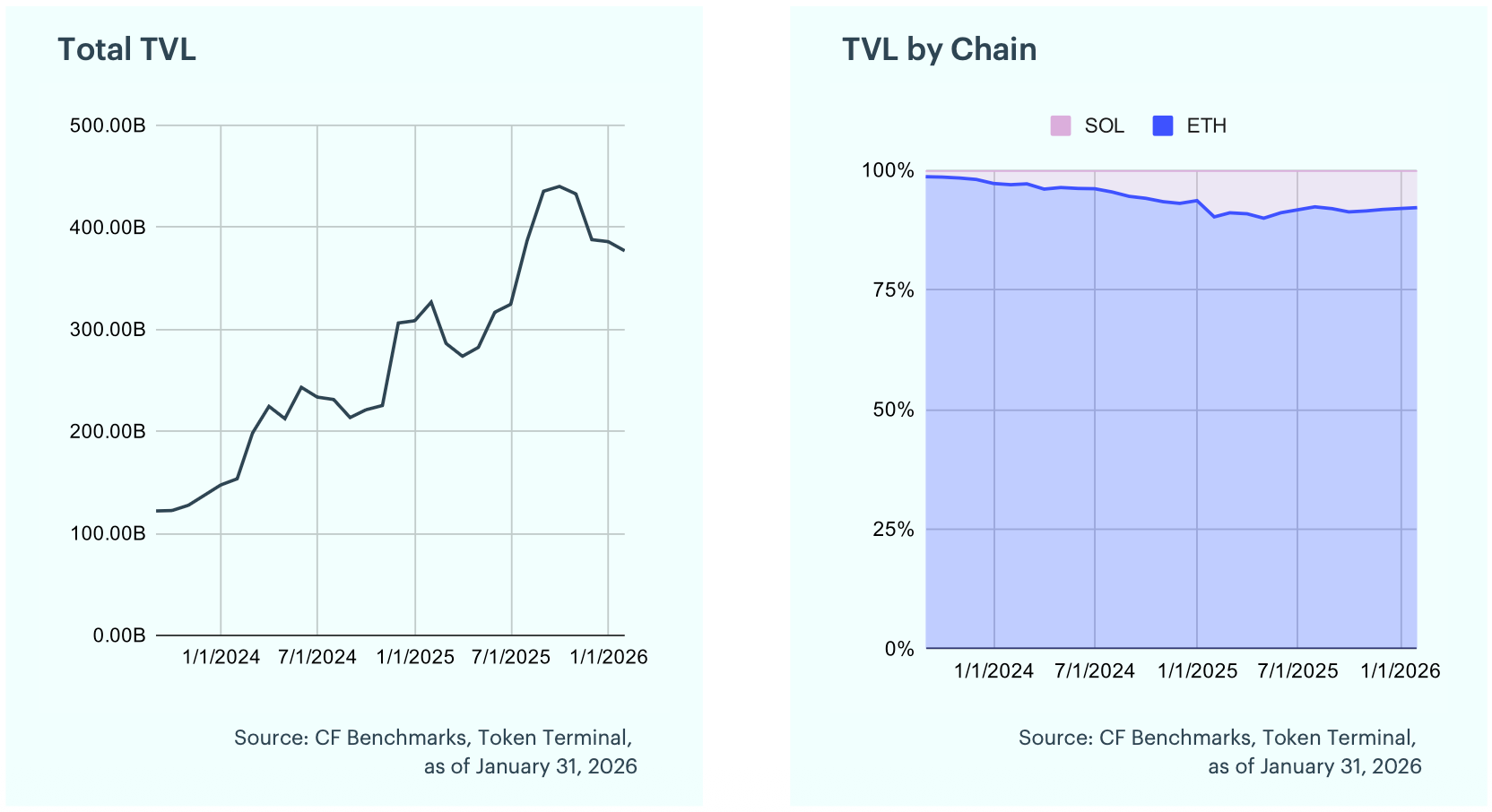

DeFi TVL Slips: Total Value Locked (TVL) measures the U.S. dollar value of assets deposited across DeFi protocols and is a core gauge of the sector’s health. Over the past month, DeFi TVL fell 2.3% to roughly $377 billion, driven by modest outflows from both Ethereum and Solana amid a broader risk-off backdrop. Solana led the decline (-4.6%), outpacing Ethereum’s pullback (-2.1%), in line with higher-beta underperformance.

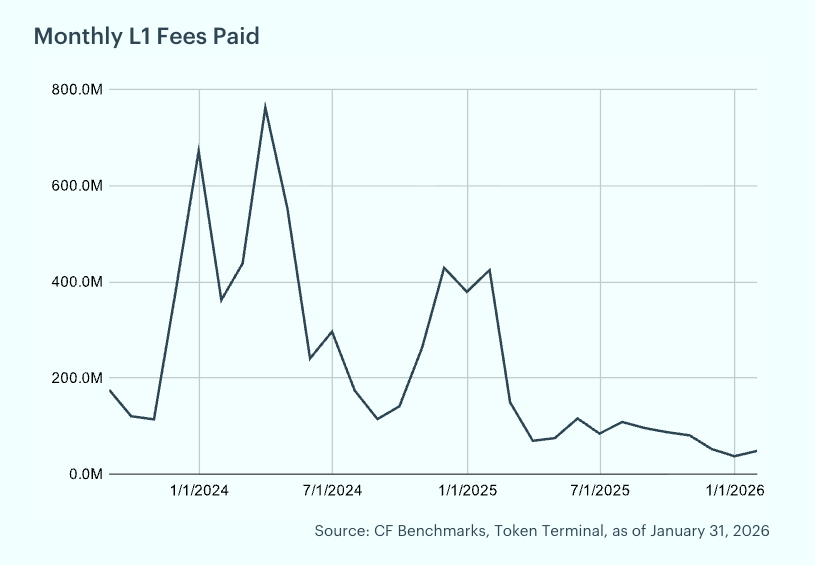

Layer-1 Fees Jump, Solana Dominates: Fees are the charges users pay to record transactions and data on a blockchain and act as a gauge for demand to use these networks. They tend to rise when there is an influx of new users on-chain and can fall when activity wanes or scaling upgrades reduce costs. In January, aggregate layer-1 fees across Bitcoin, Ethereum, and Solana rose to $48.2 million, from $37.2 million in December. Solana led with a 59.9% share, Ethereum accounted for 25.5%, and Bitcoin contributed 14.3%.

DEXs Drive Fee Surge: Breaking down Solana’s fee revenue by sector highlights which applications are driving network usage and value capture. In January, Solana layer-1 fees jumped 59.7% to $28.9 million (up from $18.1 million). Decentralized exchanges dominated, generating 81.0% of fees, while liquid staking and derivatives contributed 16.3% and 2.7%, respectively.

To read the complete report, kindly click on the provided link (or click here to view a PDF version). Additionally, please do not forget to subscribe to our latest news and research for the most relevant institutional insights on digital assets and the top digital assets by market cap.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Factor Friday - August 7, 2026

Factor Friday: beta faded, with the Market down -0.81%, while capital reached down the risk curve. Liquidity led at +1.36% and Size followed at +1.07%, both sign-inverted, and Downside Beta anchored the field at -2.69%. All three point risk-seeking, and selection set returns, not direction.

Mark Pilipczuk

Bitcoin Drives a Rebound as Breadth Narrows

The CF Free-Float Broad Cap Index rose 4.44% in July as Bitcoin and Ether supplied 5.07 points of a 4.44% return. Softer inflation and new Ethereum exchange-traded product access carried the large-capitalization core, while 18 of 32 constituents fell and free-float weighting produced the gain.

Mark Pilipczuk

Changes to the Token Market Price Benchmarks Series - Market Prices – 04 August 2026

Changes to the Token Market Price Benchmarks Series - Market Prices – 04 August 2026

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.