Dec 19, 2022

The CF Broad Cap Index

The Broadest Institutional Measure of the Crypto Market

Introduction

The CF Broad Cap Index is a liquid, investible, benchmark portfolio index that is designed to track the performance of up to 99% of the digital asset universe. The index currently represents the broadest exposure of any institutionally investible benchmark. We have designed our CF Broad Cap Index to feature two different weighting schemes (or variants): a market cap weighting methodology (CF Broad Cap Index - Market Cap Weight) and a diversified weighting structure (CF Broad Cap Index - Diversified Weight). For the market cap, the weighting is determined by the adjusted free-float market capitalization. Meanwhile, the diversified weighting mechanism adjusts the free-float market capitalization by a harmonic-series diversifying factor. This allows the diversified weighting to discount higher market capitalized assets, thus allowing for further diversification. The CF Broad Cap Index is reconstituted and rebalanced on a quarterly basis.

Key takeaways from this report:

- The CF Broad Cap Index is designed to serve as a true barometer of the cryptocurrency market, thus providing the broadest and most institutionally investible ‘beta’ market gauge

- The CF Broad Cap Index allows researchers and investors the ability to analyze the crypto market and its historical evolution. Practitioners can also utilize our proprietary CF Digital Asset Classification Structure (CF DACS) for additional context so as to understanding the blockchain economy

- Lastly, the diversified weighting mechanism addresses the most common issues that institutional investors face when dealing with a concentrated asset class while also allowing adding flexibility for a nascent asset class like crypto to evolve and grow

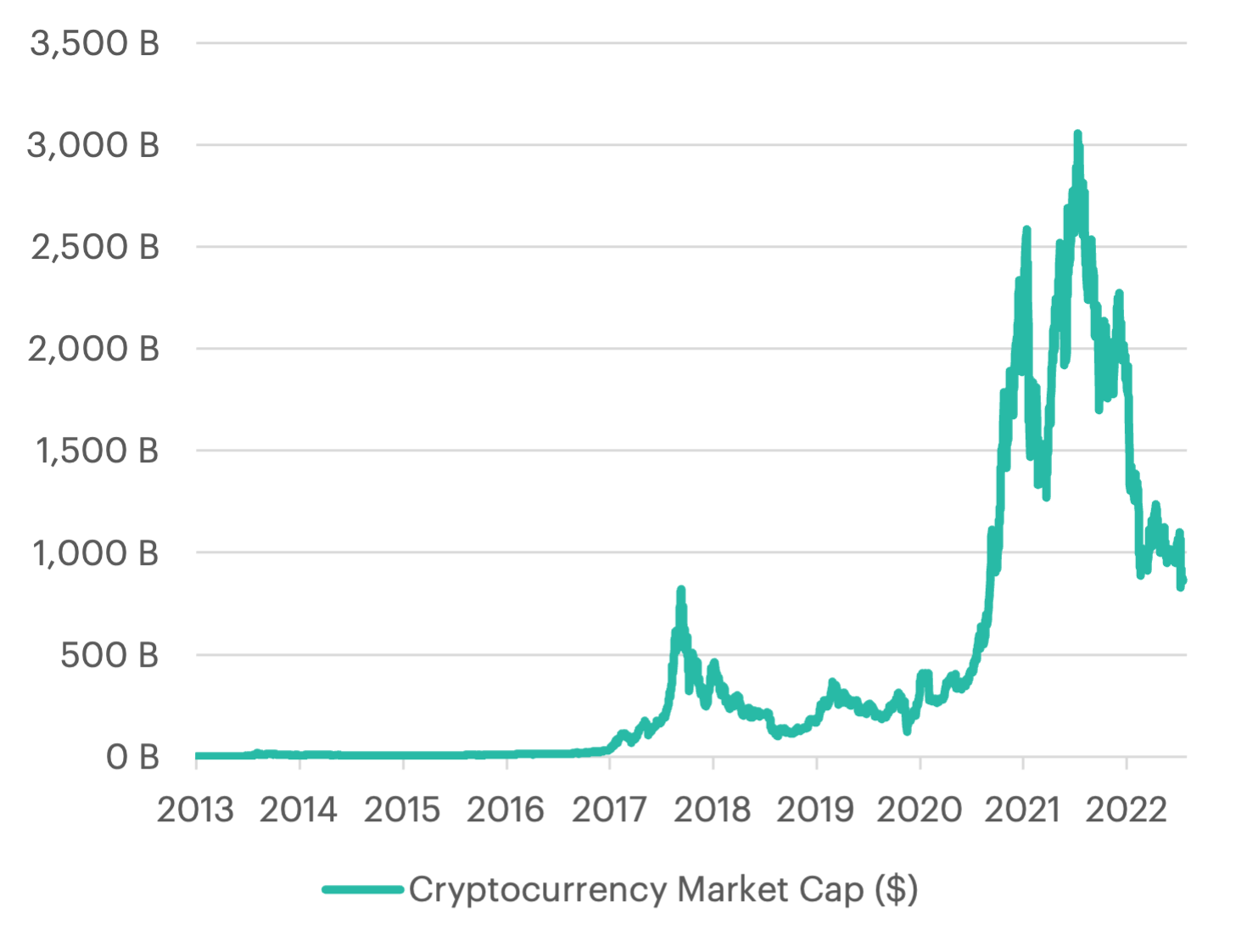

Defining the crypto market

In November of 2021, the market capitalization of digital assets peaked at just over $3T. Since then, the overall size of the market has fallen to just under $1T. These figures are intended to represent the summation of market values for the entire universe, or “Cryptocurrency Market”.

However, from an institutional perspective, investors must have a more stringent approach. Asset allocators that wish to invest sizable amounts into digital assets must consider a series of factors such as:

- Investibility: liquidity screens with free float adjustments to ensure reliable replicability

- Accurate Representation: Utilization of only reputable exchanges for pricing data, along with the exclusion of stablecoins

- Robustness: Guardrails that prevent prevailing forms of market manipulation while navigating regulatory matters

Striking a sensible balance

Another common approach for defining the crypto market involves simply using a single token, such as Bitcoin, as a barometer. Although this is pragmatic, the creation of new tokens and protocols over the past few years has dwindled Bitcoin’s overall representation to approximately 37% (down from nearly 90% in early 2017). This trend of diminishing representation is likely to only accelerate, making this approach untenable.

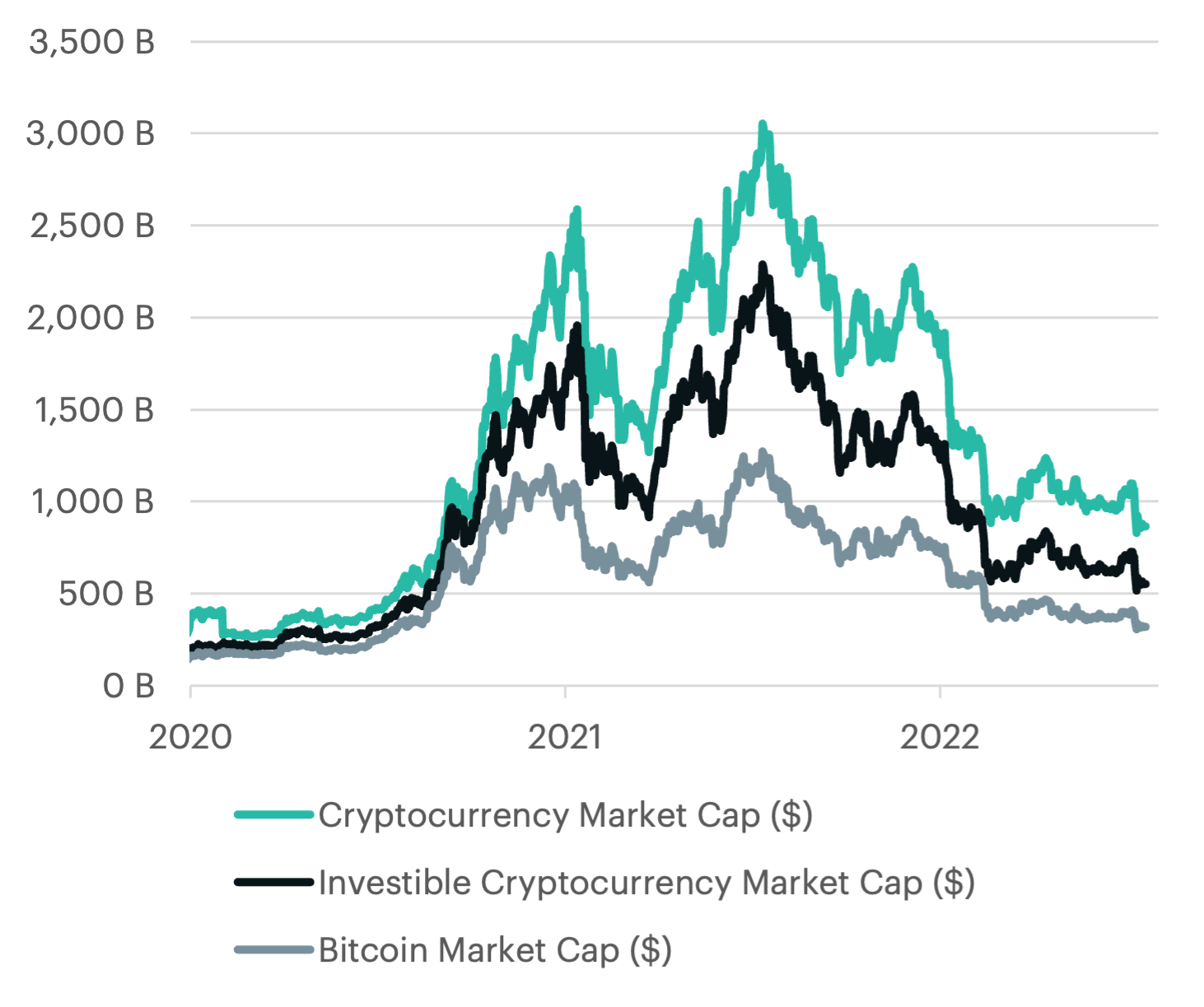

At CF Benchmarks, we believe in striking a sensible balance. Our industry leading liquidity screens and robust guidelines for constituent inclusion are designed to present solutions for institutional asset managers to gain the broadest exposure, while providing sensible guardrails for reducing unnecessary risk. After applying our qualifying approach, the current market cap of investible tokens currently stands at just over $500bn, or 63% of the unfiltered universe. This allows the refined investible market universe to be broadly diversified, while sidestepping the illiquid assets that would plague an institutional investor.

The stablecoin dilemma

Stablecoins are crypto tokens that attempt to keep their market value stable, or pegged, to a fiat currency like the U.S. dollar. The popularity and usefulness of stablecoins cannot be ignored. For example, the market cap of the top five most popular stablecoins has grown almost fivefold, from just $23.5bn to $115.8bn in the past two years. Users find stablecoins to be practical for de-risking their asset-allocation during times of volatility since these tokens have a lower volatility profile. Additionally, stablecoins provide a way to transfer assets from one wallet to another in a way that keeps costs and volatility to a minimum.

However, at CF Benchmarks, we find the use cases to be less prudent for inclusion in our indices. Firstly, the risk/return profile of stablecoins has historically been shown to artificially reduce risk and sacrifice return potential. This is because stablecoins are intended to remain permanently pegged, thus reducing pricing volatility. However, stablecoins have had a history of facing issues that can cause them to de-peg or collapse entirely. In other words, this can be viewed in a binary sense since a stablecoin should have an expected return of zero but can still have the same potential drawdown risk of any other digital asset. Therefore, we do not believe that the inclusion of stablecoins makes sense as a strategic allocation in any index that is designed to provide an accurate representation of the crypto market for an investor's portfolio.

Stablecoin market cap growth (from 12/2020-12/2022)

Providing a better ‘beta’ measure

The CF Broad Cap Index is intended to definitively define the broadest measure of the crypto market. Our proven index methodologies allow for institutional caliber investors to create products for any type of client that wants to participate in investing into crypto. For the first time, practitioners can feel confident in the broadest investible representation of the market, providing the most refined ‘beta’ to benchmark against.

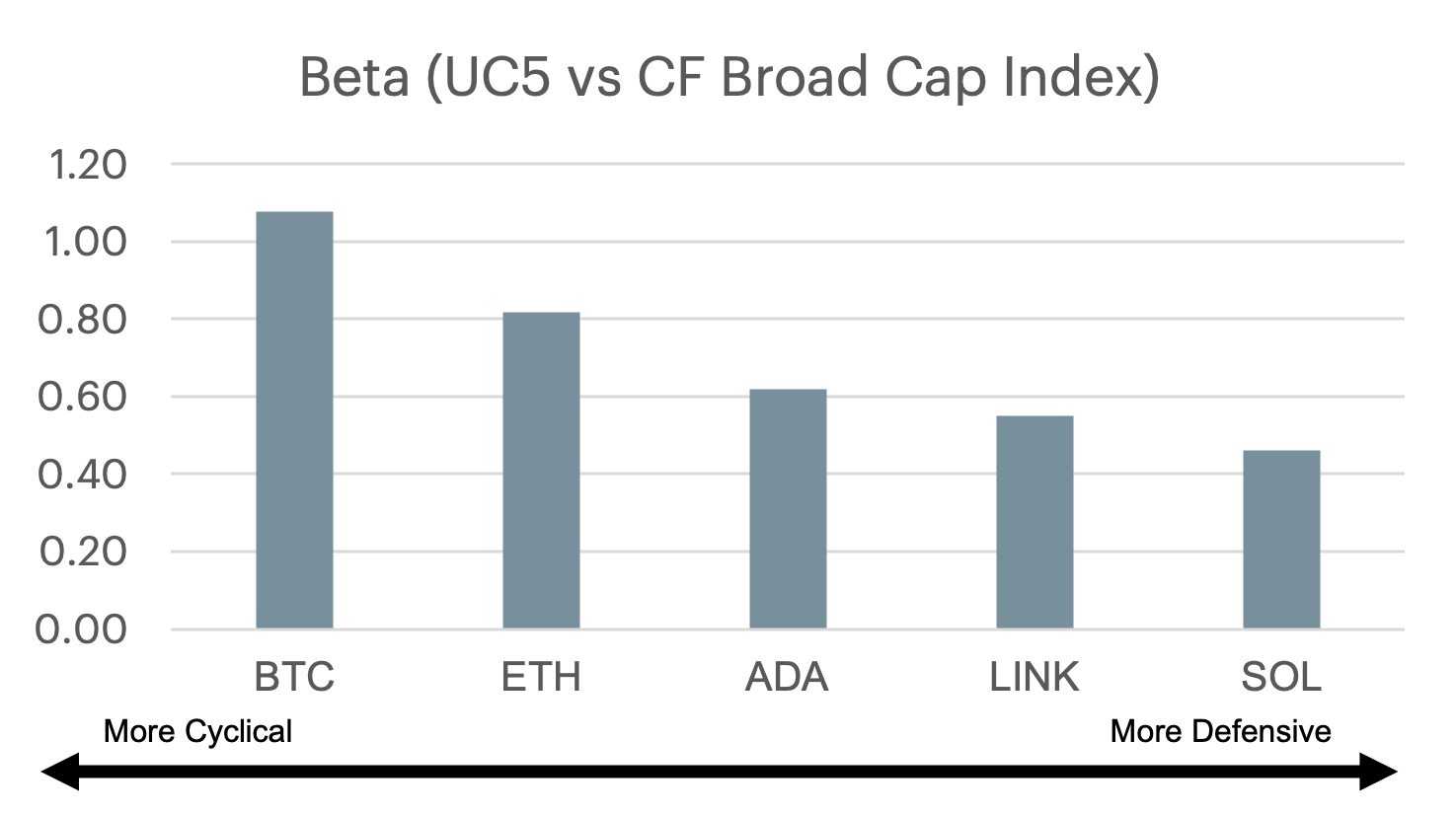

What is beta? Beta is a measure of the volatility, or sensitivity, of an asset when compared to the overall market. Since this measure is typically compared to a widely used benchmark, it is commonly used to reflect systematic, or undiversifiable risk.

When benchmarking the constituents of the Ultra Cap 5 index to our CF Broad Cap Index, investors now have a better comparison for gauging the sensitivity of their holdings to the overall market. In this example, we have identified that BTC is the most sensitive asset to overall market moves. Meanwhile, ETH is about 20% less sensitive to overall market moves but is still relatively highly sensitive when compared to the two most defensive tokens, SOL and LINK. Professional practitioners, from researchers to portfolio managers, can now apply this commonly used risk-framework to our more refined Broad Cap index.

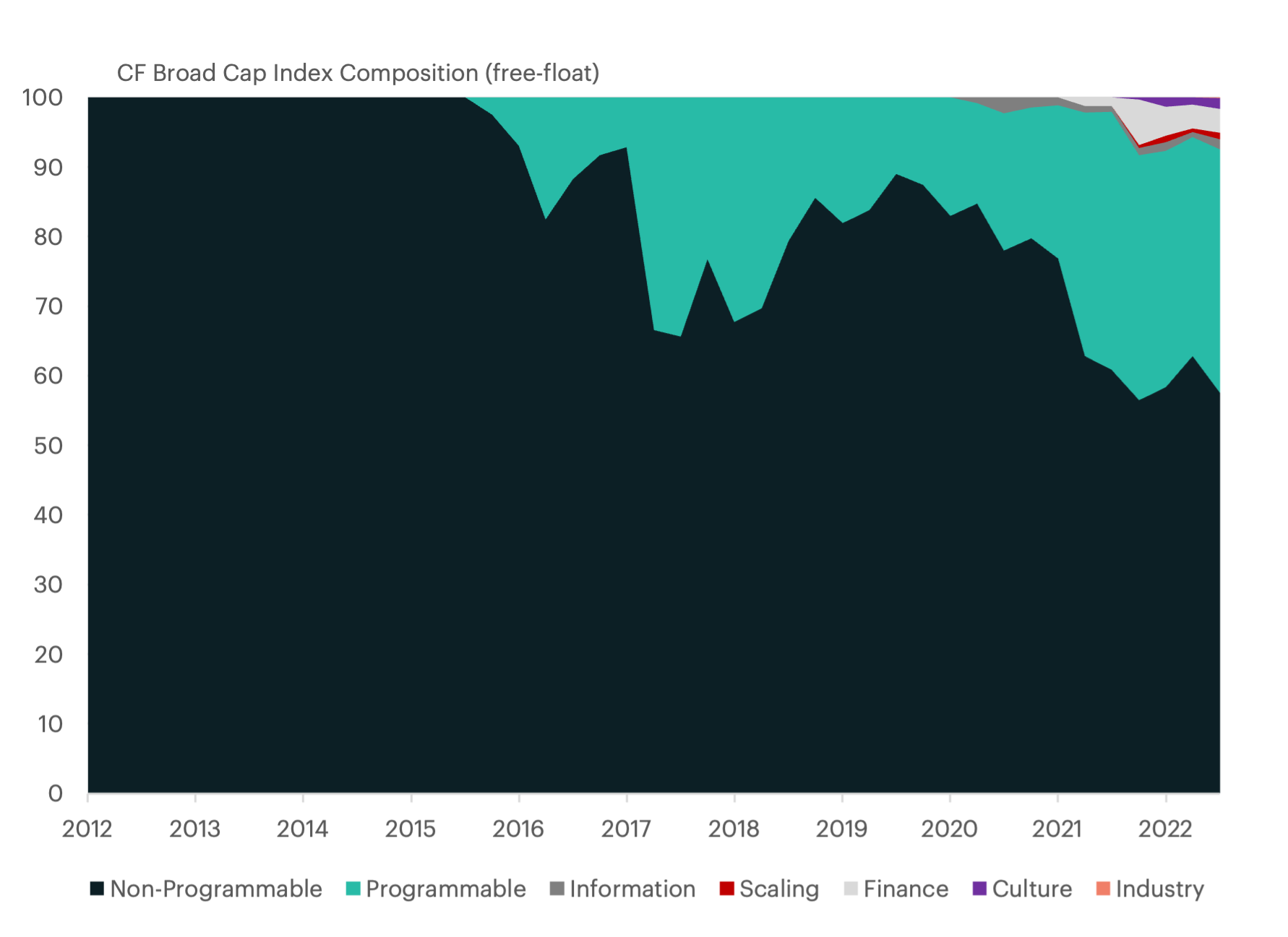

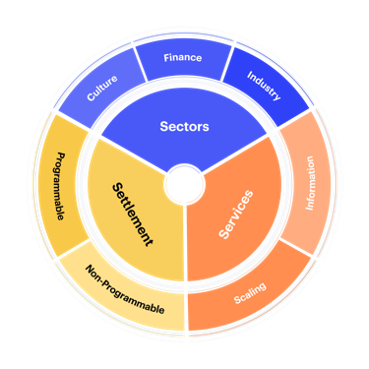

Broad means broad: diversifying with the CF DACS

Our CF Broad Cap Index is designed to provide the broadest exposure to the crypto market while still accounting for the practical limitations that institutional investors face. These limitations involve accounting for ample liquidity so that institutional investors can replicate or scale their portfolio into any of the constituents’ respective markets. Additionally, having safeguards for pricing manipulation, while excluding categories such as stablecoins, will provide a universe that is refined enough to meet institutional standards.

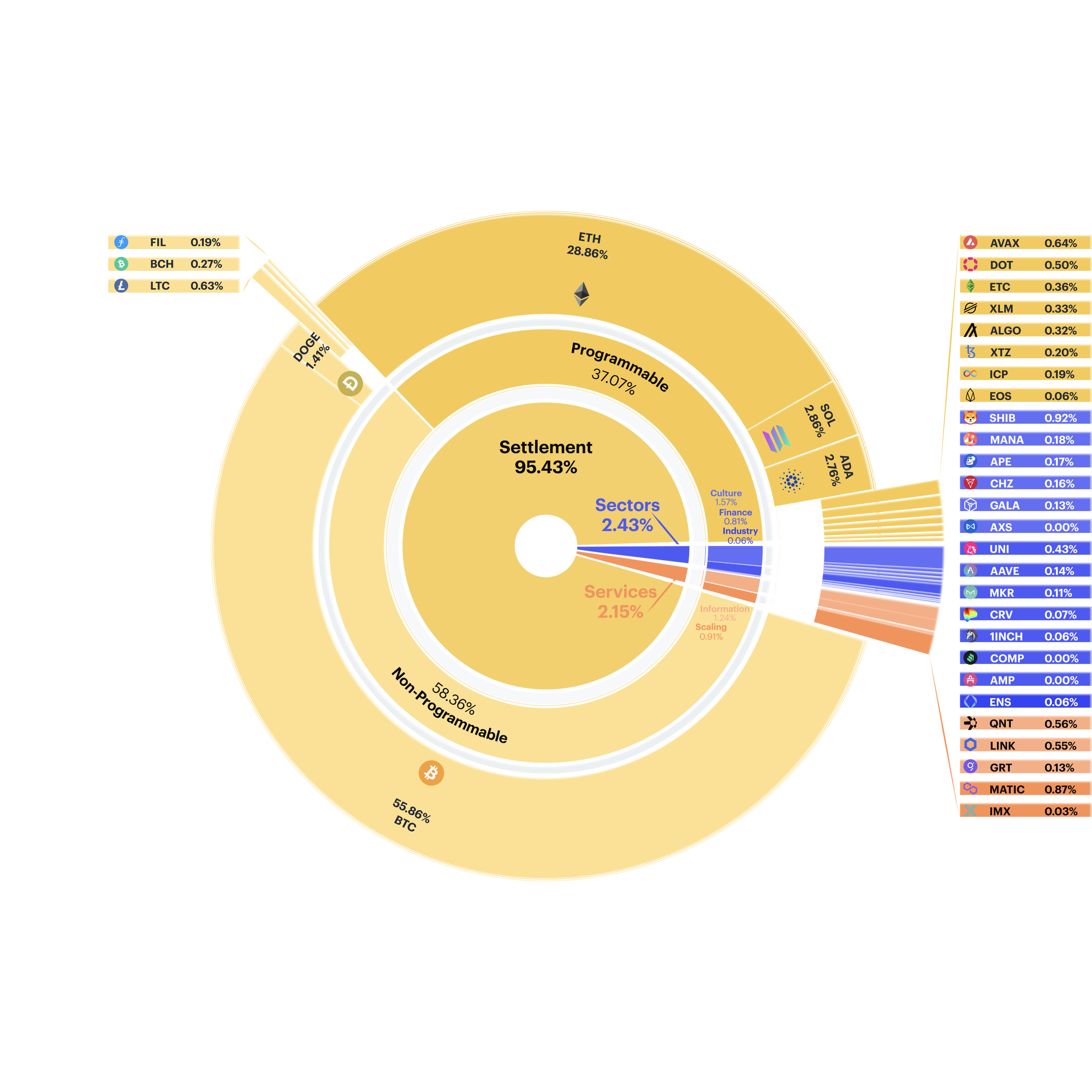

The index allows investors to gain exposure to all facets of the crypto market. Nobel price laureate Harry Markowitz famously said that ”diversification is the only free lunch in investing.” This is because, as an investor, gaining exposure to less correlated assets will allow you to materially reduce the overall risk of your portfolio without sacrificing returns. The illustration above highlights how important exposure to less correlated segments can be. Our CF Digital Asset Classification Structure (CF DACS) uses a purpose centric framework to identify these segments. Segments like Finance, Culture, Industry and Information, are much less correlated, on a short-term pricing basis, to more heavily weighted categories like Non-programmable, Programmable, and Scaling.

CF Broad Cap Index at a glance (Market Cap Weight)

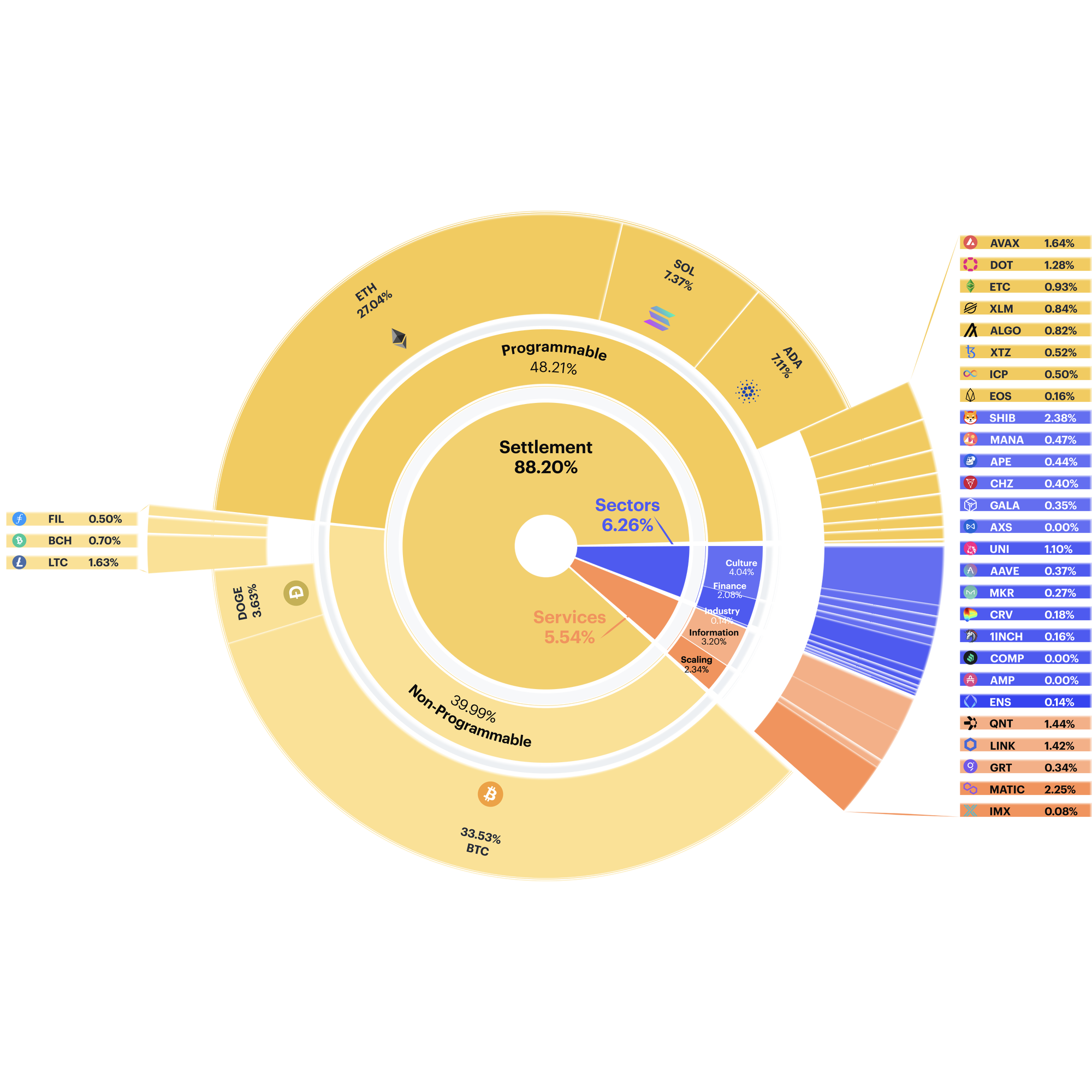

The market cap weighted variant reflects a free-float adjusted market cap weighting, which results in a 95% exposure to the Settlement category of our Digital Asset Classification Structure (DACS). The remaining segments, Services and Sectors, each contain approximately over 2%.

Looking further into our CF DACS categories, we can see that 58% is in Non-Programable, such as BTC (56%), and 37% is in Programmable settlement protocols, like ETH (29%). Other level 2 categories include Culture, Finance, Information, Industry, and Scaling.

The nascent stage of the crypto market has kept the market capitalization rankings concentrated in the most popular tokens, such as BTC and ETH. However, more ”emerging” categories are likely to continue to grow in representation as the industry continues to mature.

An evolutionary tale of an emerging asset class

Bitcoin is born - Bitcoin, a non-programable settlement protocol, represents the first mainstream decentralized digital currency that fully executes asset transfers on a peer-to-peer network. This technology marks the genesis of the cryptographic technology that has spawned the digital asset class. Today, Bitcoin still represents most of the Non-programmable segment, despite the emergence of newer competitors.

Ethereum comes on the scene - The next wave of growth can be seen when Ethereum, a programmable settlement token, arrives. Ethereum took decentralization a step further by developing an open-source blockchain which can fully execute smart contracts. Smart contracts allow computer programs to be built that autonomously execute transactions or actions. As shown, the launch of Ethereum and other programmable protocols, have taken a sizable portion of the crypto market.

A vibrant ecosystem comes to life

The rise of Programmable blockchains since 2015 has allowed the crypto ecosystem to continue its evolutionary course. The last bull market cycle that occurred mostly in 2021, led to exponential growth in emerging categories such as Finance, Culture, Information and Scaling. Some may call this era the DApps (decentralized applications) Revolution.

Decentralized finance (or DeFi) emerged first, with developers building protocols that provide decentralized (or trustless) versions of traditional financial services such as trading venues, borrowing/lending, and even insurance. Next, we saw digital culture applications rise in tandem with the broader concept of a metaverse. These protocols allow users to create digital forms of art, such as pictures, or music, in the form of a non-fungible token (NFT). This category also includes games that allow users to earn tokens as they play.

All this growth in activity ultimately required an upgrade to existing network infrastructure. First, for these financial activities to be executed, developers created oracle networks that supplied data and information for the DApps. This information can include real-world information such as market prices or exchange rates that allow smart contracts to execute upon them. Lastly, scaling solutions were developed to help improving speed, efficiency, and overall bandwidth for the blockchain networks in use.

Price Returns by CF DACS Category (log-scale)

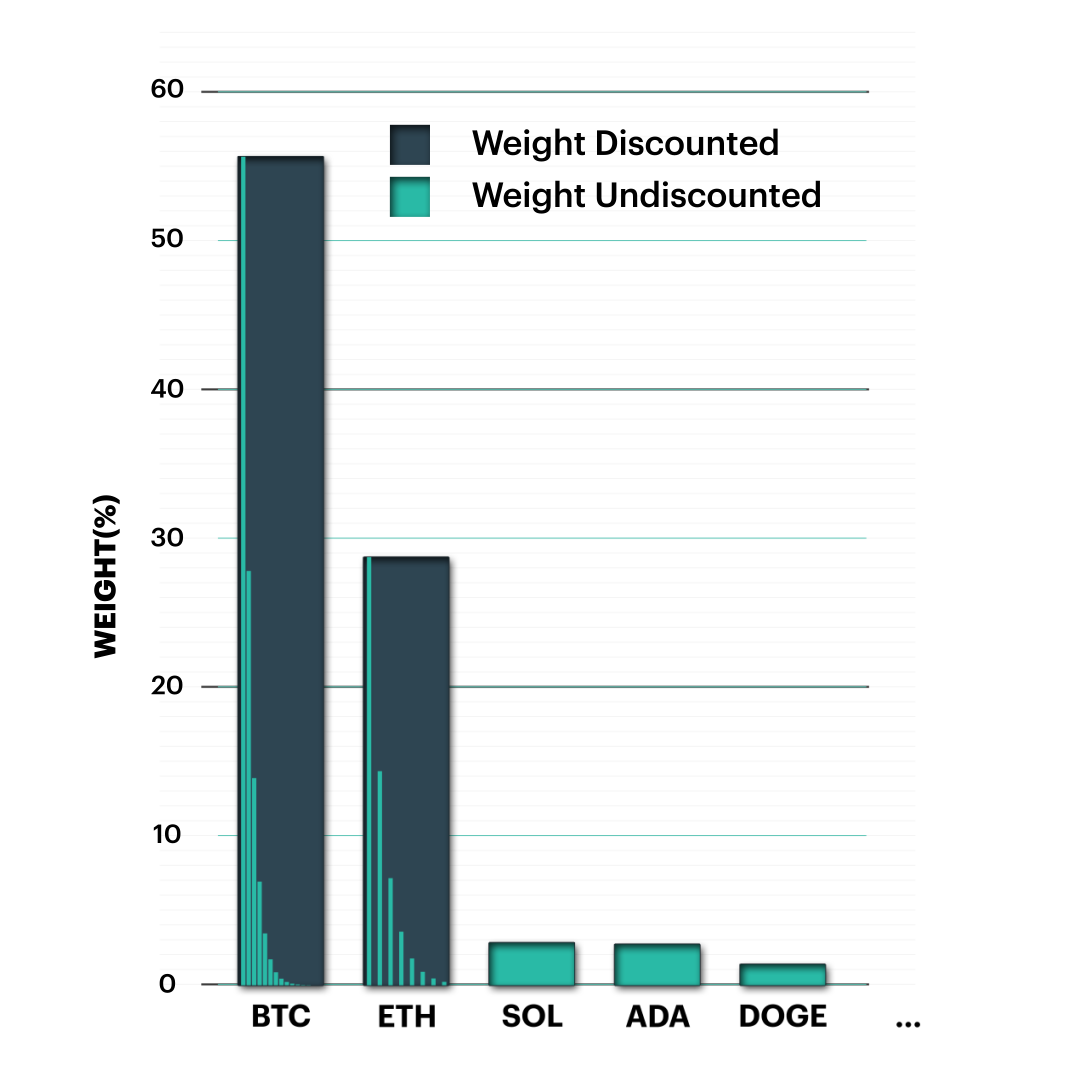

Solving for over-concentration with smoothed capitalization

Free-floating market capitalization is clearly dominated by the two largest caps, Bitcoin and Ether. This is due to multiple factors, including the relative immaturity of the market. In traditional markets, indices tend to use weight caps to mitigate large concentrations in one or multiple assets, with the resultant excess weight distributable through the divisor to the constituents whose weights are below the cap. Prescribing a fixed cap of 25% for The CF Diversified Broad Cap Index would result in the top 2 assets exceeding the weight limit at inception. Alternative fixed capitalization limits would result in the same issue. The index would behave more like a fixed-weight index.

Instead of applying a hard cap, the index will benefit from a ‘smoothed capitalization’ methodology, where each additional weight percentage is discounted sequentially more than the previous one by a defined amount. The procedure is explained in greater detail here. This progressive redistribution from large caps to small caps benefits from keeping final weights adapted to free-float market caps while still achieving a defined diversification.

CF Broad Cap Index at a glance (Diversified Weight)

The diversified weighting variant is designed to address the concentration issue that can arise in a nascent asset class like crypto. Our diversifying factors have been applied to reduce the weight of the two largest positions, Bitcoin and Ethereum. This results in Bitcoin’s exposure falling approximately 12% in absolute terms to 33.5%. By contrast, Ethereum’s weighting is reduced by just 1%

From a CF DACS perspective, the disproportionate reduction from Bitcoin results in the Non-programmable segment seeing a smaller representation (falling from 58.3% to 40%). Meanwhile, the Programmable segment sees sizable increases to altcoin constituents, which brings the new weighting up to 48% from 37%. Lastly, the Sectors and Services segments see the largest relative increase in exposure. Each segment sizes up more than two-fold from 2.4% to 6.3% and from 2.2% to 5.5%, respectively.

Appendix: CF Digital Asset Classification Structure

The CF Digital Asset Classification Structure (CF DACS) classifies coins and tokens based on the services that the associated software protocol delivers to end users, grouping assets by the role they play in delivering services to end users. The CF DACS powers CF Benchmarks' sector composite and category portfolio indices and allows users to perform attribution analysis to better understand the fundamental drivers of returns within their digital asset portfolios.

Additional Resources

For more information about our CF Benchmark indices and our methodologies, please visit the respective web links below:

- CF Diversified Large Cap Index

- CF DeFi Composite Index

- CF Web 3.0 Smart Contract Platforms Index

- CF Digital Culture Composite Index

- CF Blockchain Infrastructure Index

- CF Cryptocurrency Ultra Cap 5 Index

- CF Broad Cap Index - Market Cap Weight

- CF Broad Cap Index - Diversified Weight

Contact Us

Have a question or would like to chat? If so, please drop us a line to:

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Ken Odeluga

Ken Odeluga