Nov 03, 2025

Policy Progress & Portfolio Pressures

Key takeaways for the month

October 2025 was defined by another wave of new product access and easing policy. The SEC's recently released generic listing standards green-lit new U.S. spot ETFs beyond BTC and ETH, headlined by Bitwise's Solana staking ETF, which gathered over $400M in fund flows in the first five days of trading. CME launched options on Solana and XRP futures, expanding tools for hedging and directional strategies. The FOMC delivered a 25 bp cut to 3.75–4.00% and signaled a tapering of quantitative tightening, modestly easing financial conditions. Fund flows set early-month records, then turned choppy before firming into month-end as investors rotated across BTC, ETH and SOL-related ETPs.

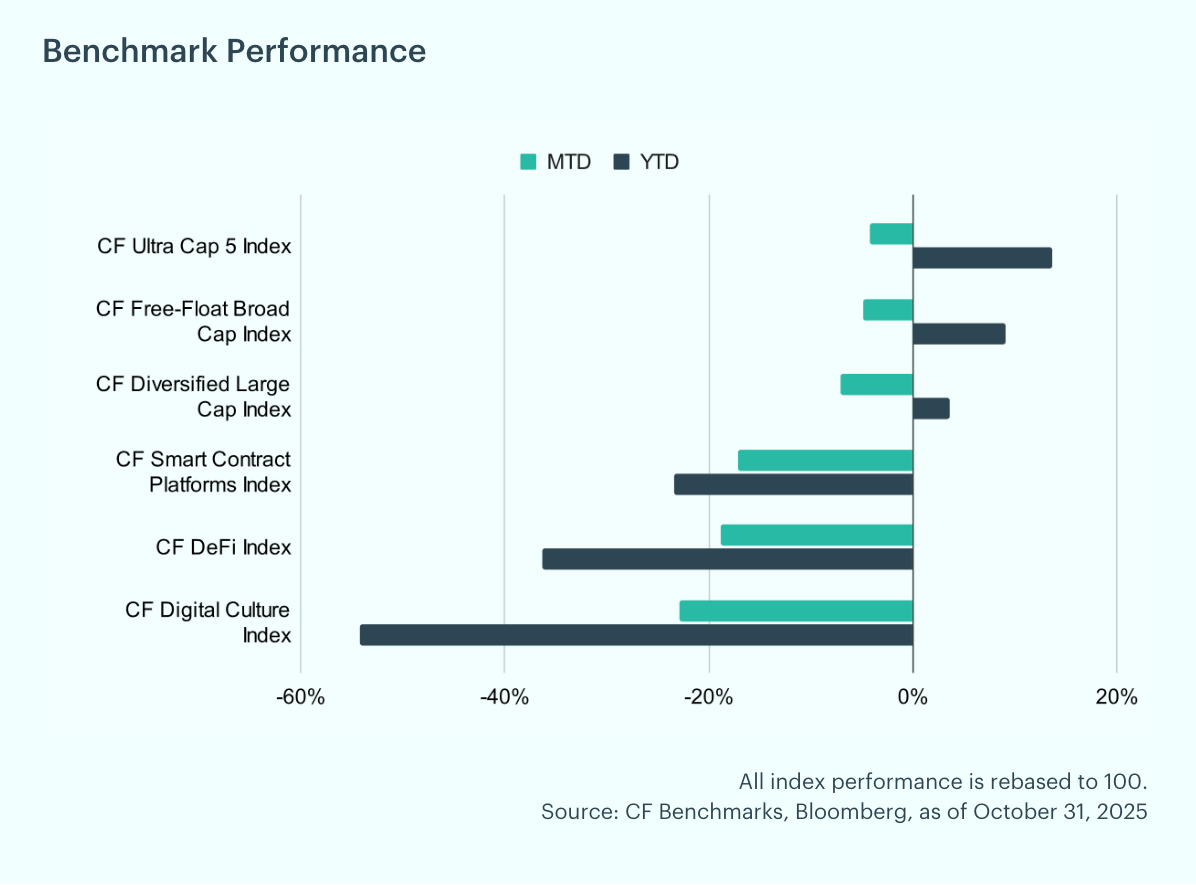

Risk-Off Rotation: However, product breadth and incremental monetary easing failed to reinforce confidence. The Fed Chair's post-meeting remarks dampened sentiment and boosted market volatility, leading digital assets lower in October with broad declines and a renewed tilt toward defensiveness. The CF Ultra Cap 5 Index fell 4.19% for the month but remains up 13.64% YTD. The CF Free-Float Broad Cap Index slipped 4.87% (+9.13% YTD), and the CF Diversified Large Cap Index declined 7.15% (+3.62% YTD). Higher-beta cohorts led the drawdown: the CF Smart Contract Platforms Index dropped 17.09% (−23.38% YTD), the CF DeFi Index fell 18.82% (−36.31% YTD), and the CF Digital Culture Index plunged 22.92% (−54.21% YTD). Overall, mega-caps proved relatively resilient while riskier segments materially underperformed.

Individual Movers: Bitcoin demonstrated notable resilience amid a broad market downturn, declining only 4.5% as approximately $5 billion in ETF inflows provided a steady bid during the selloff. Hedera’s HBAR token also exhibited relative strength, falling just 6.6%, supported by positive sentiment following its October 28th ETF listing, which provided a notable boost to the token’s price. General-purpose smart contract platforms Avalanche (AVAX) and Fantom (FTM) were among the weakest performers in October, declining 39.4% and 37.6%, respectively. Despite continued developments in both ecosystems, the persistent impact of low liquidity following the liquidation event on October 10th remains a significant headwind.

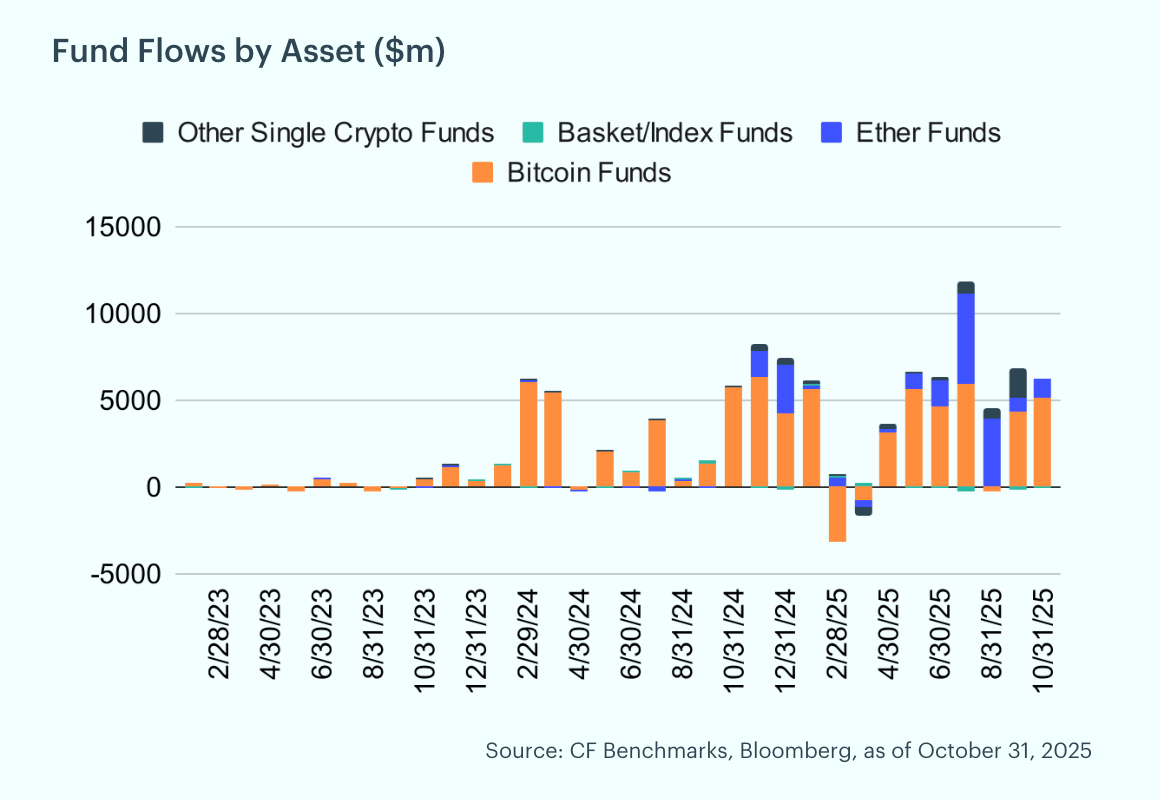

Fund Flows Remain Robust: October saw continued inflows into digital asset funds, with investors allocating roughly $6.2 billion. Bitcoin accounted for the lion’s share at $5.1 billion, while Ether lagged with a more modest $1.1 billion. Regionally, North America dominated activity, recording net inflows of about $9.1 billion, compared to Europe’s $120 million, highlighting the relative strength of U.S. investor demand.

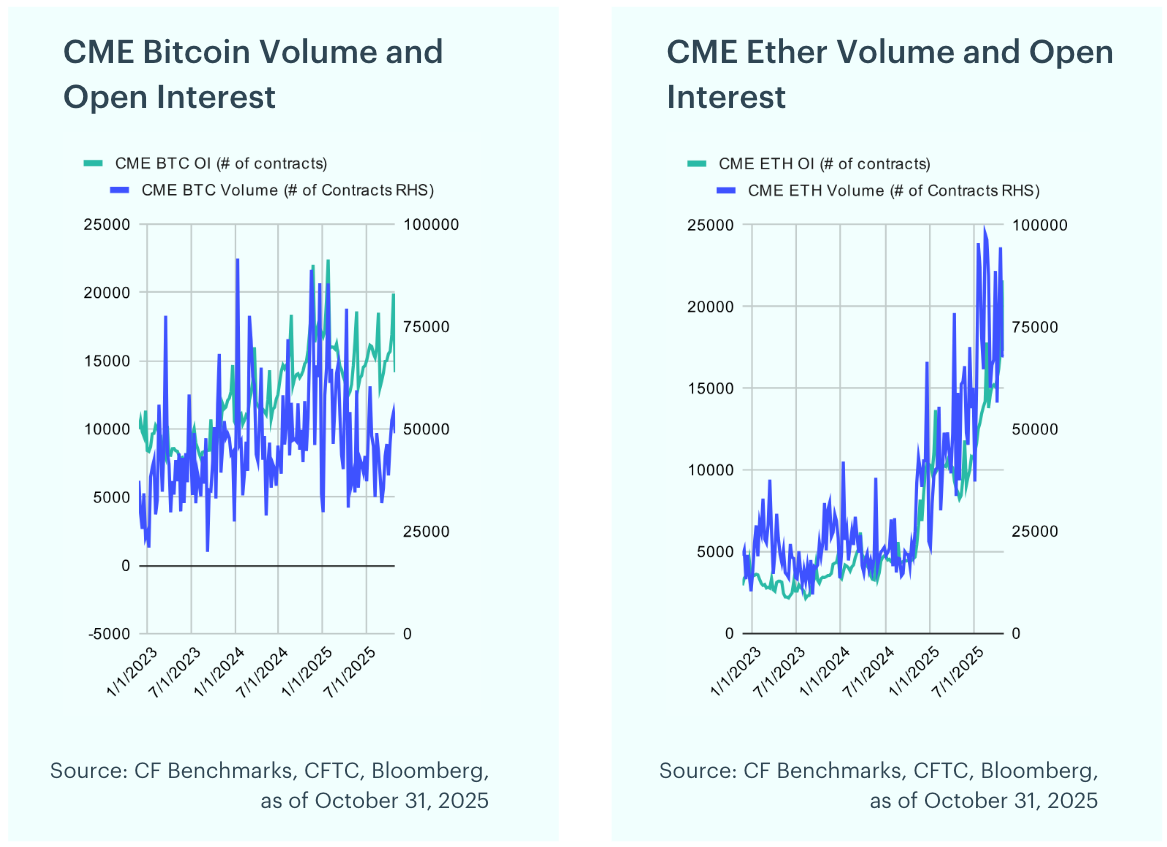

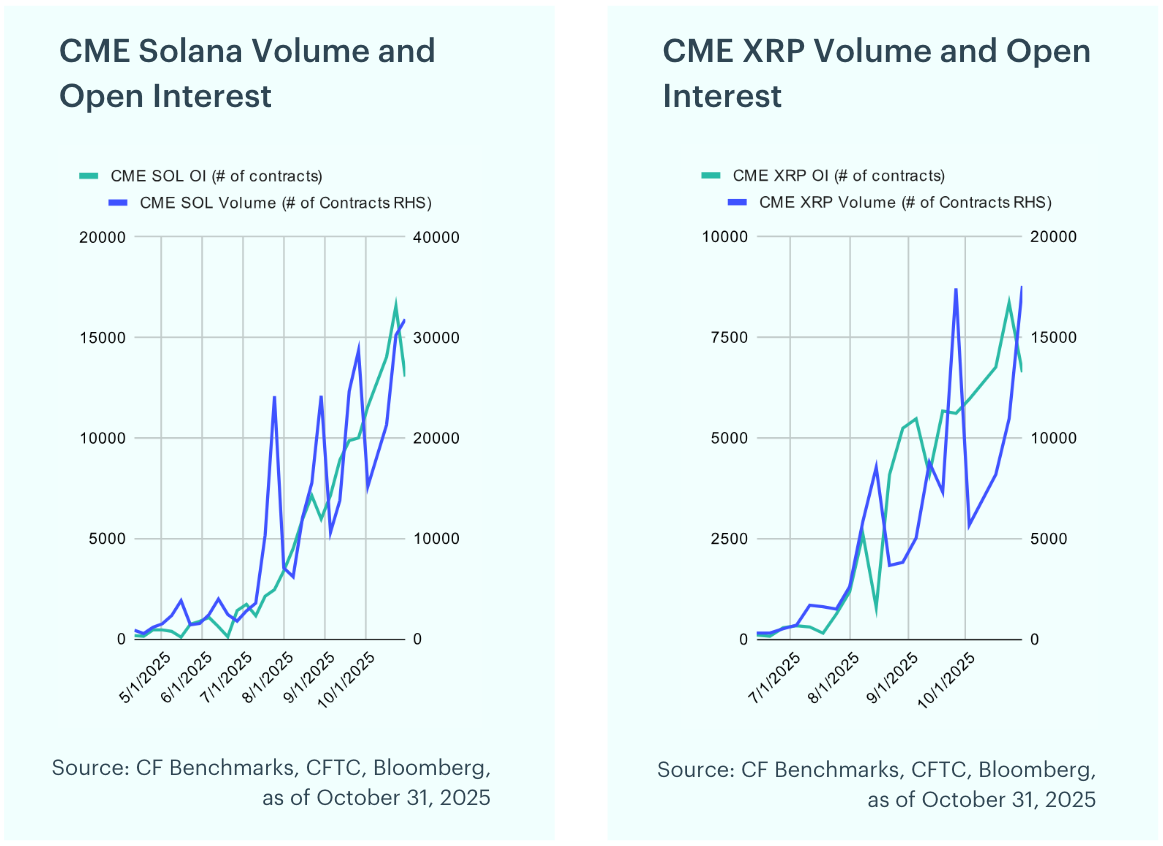

Alt-Futures Activity Surge: Bitcoin futures saw a slight decrease in open interest in September, falling 5.7% from 15,014 to 14,157 contracts. Ether futures also gained momentum, with open interest climbing 14.5% to a record 17,281 contracts, supported by robust trading activity that peaked at 88,733 contracts at month-end. Meanwhile, Solana and XRP futures posted substantial expansion amid heightened investor interest: Solana’s open interest surged 30.5% to 13,053 contracts, with volumes exceeding 31,000 contracts, while XRP’s open interest jumped 18.1% to 6,628 contracts, accompanied by a material increase in trading volumes.

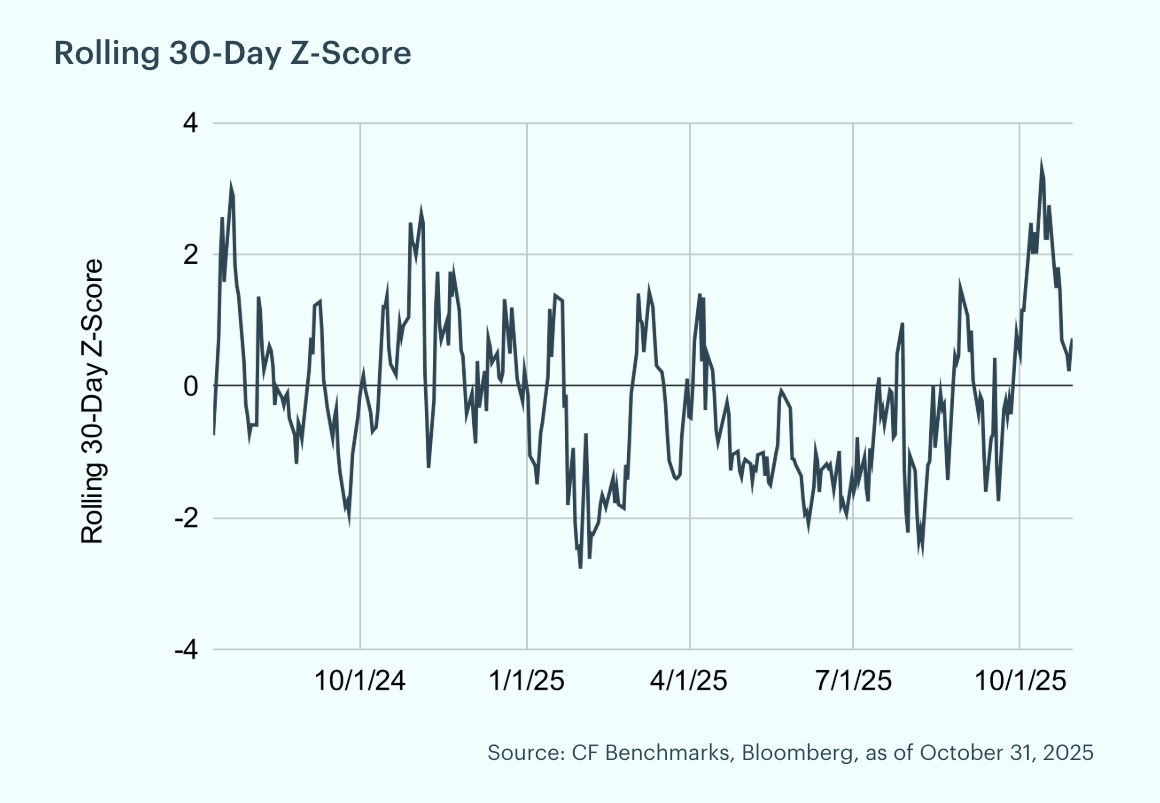

BVX Records 3.2 Sigma Mid-Month Spike: The CF Bitcoin Volatility Index Settlement Rate (BVXS) is a daily benchmark that provides a forward-looking, 30-day constant-maturity measure of implied volatility, derived from CFTC-regulated Bitcoin option contracts traded on the CME. The BVX reflects the fair strike of a variance swap. Over the past month, the BVX ranged between 38.1 and 52.0. During this period, volatility increased materially, with the BVX recording a 3.2 sigma move (based on our rolling 30-day z-score) around mid-month.

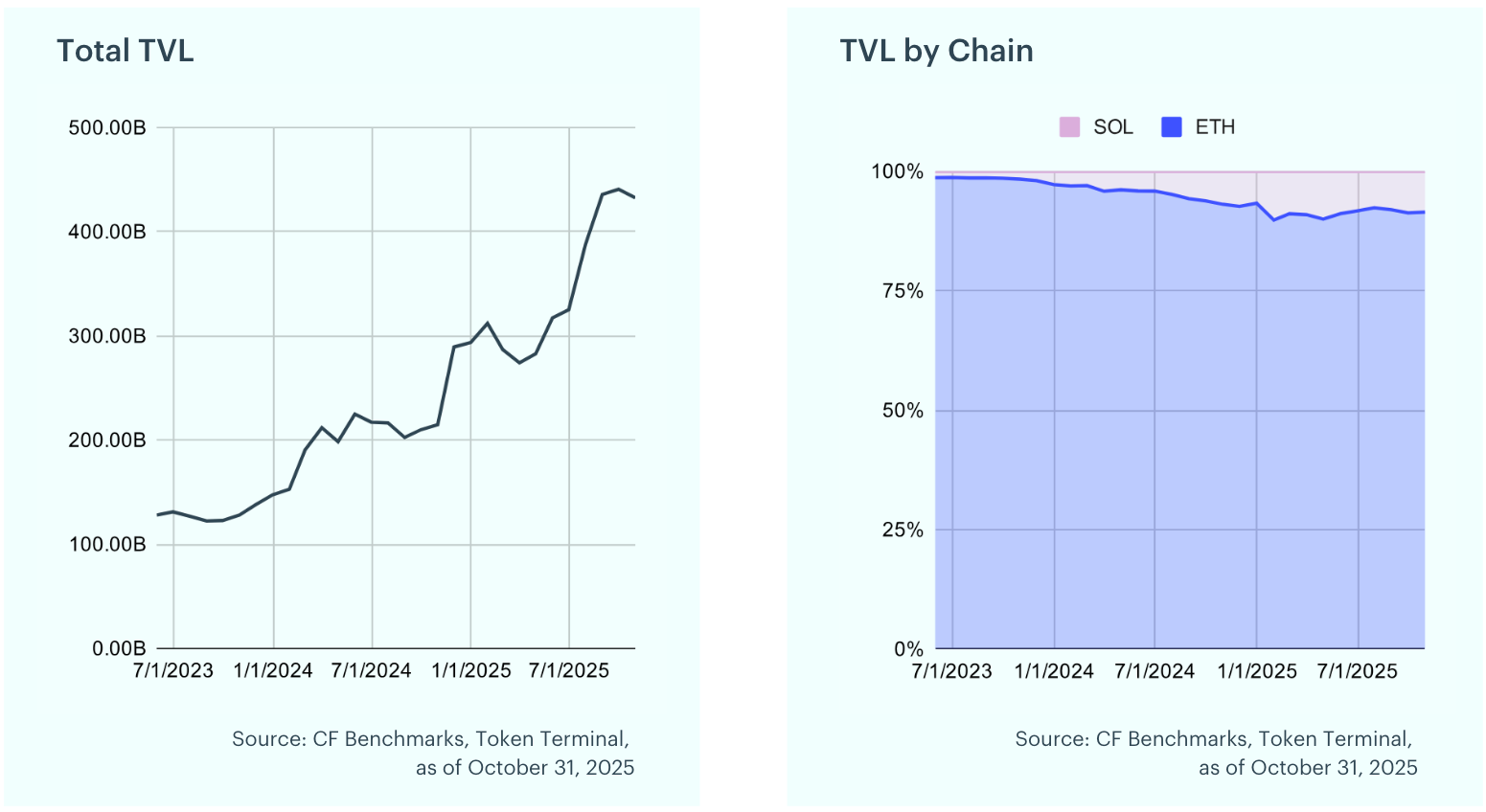

Total Value Locked Slips: Total Value Locked (TVL) in decentralized finance (DeFi) represents the aggregate value of assets deposited across DeFi protocols, expressed in U.S. dollars. It serves as a key indicator of the sector’s overall health and growth. Over the past month, total DeFi TVL declined by 1.9% to approximately $432 billion, as growth stalled amid pullbacks in Ether and Solana following their recent rallies.

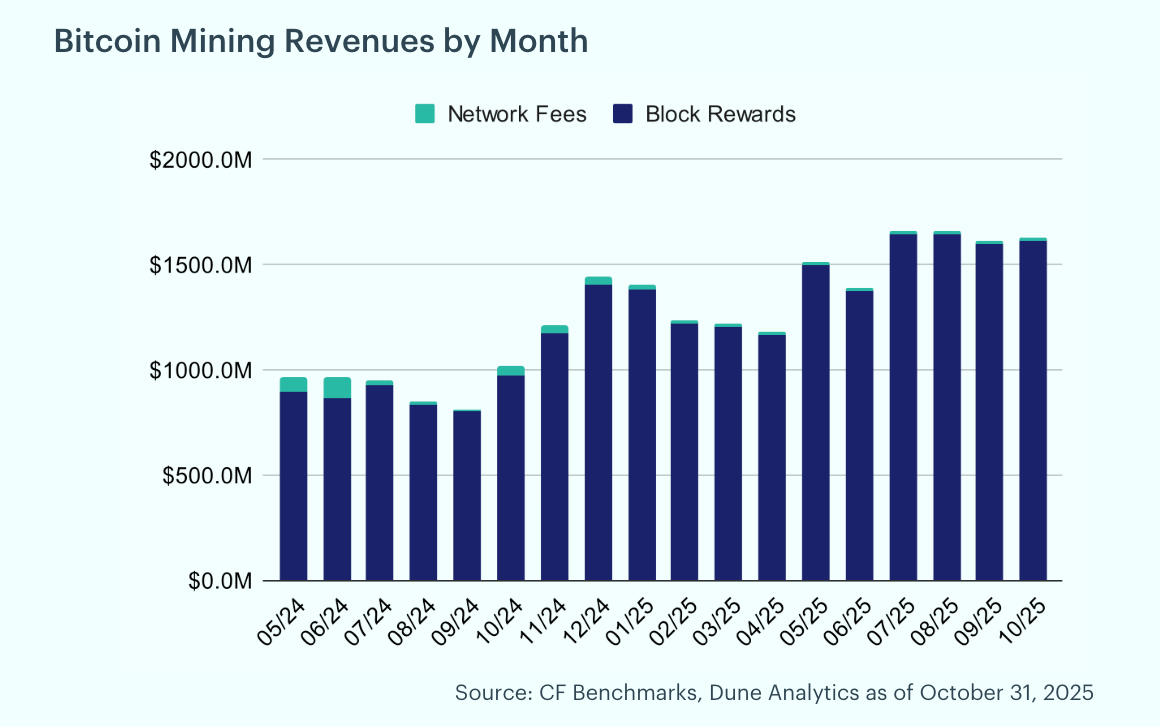

Miner Economics Stable: Bitcoin’s hash rate grew significantly in September, rising 9.7% to 1050 exahashes per second. Mining difficulty, which measures the computational effort required to mine a new block and adjusts to maintain consistent block creation times, increased by 5.1% after a period of faster block times in late September. The next difficulty adjustment, expected in the mid October, is currently projected to be a 0.8% increase.

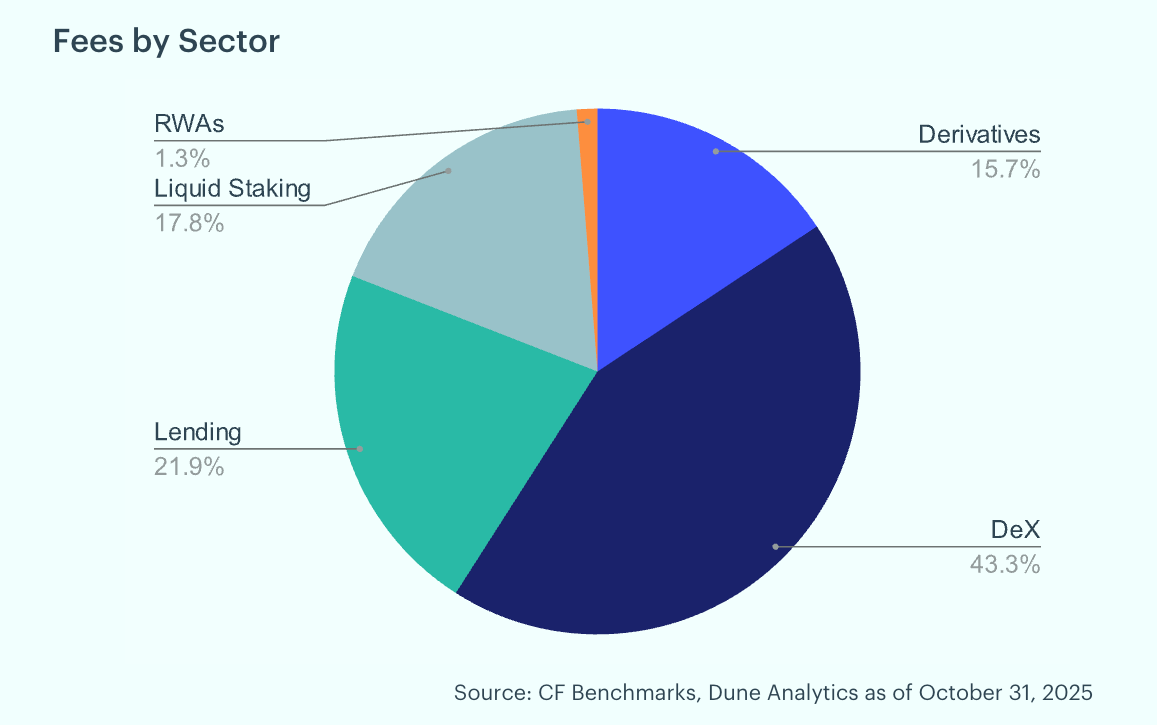

ETH Fees Up 15.3% as DEX Activity Commands 43% Share: Analyzing Ethereum’s total fees and their sector composition provides insight into the use cases driving network revenue. Ethereum layer-1 fees rose 15.3% month-over-month, increasing to $41.1 million in October from $35.9 million in September. Decentralized exchanges accounted for the largest share at 43.3%, followed by lending protocols at 21.9% and liquid staking at 17.8%. Derivatives contributed 15.7%, while real-world asset tokenization represented just 1.3%, underscoring the continued dominance of DEX activity in network fee generation.

To read the complete report, kindly click on the provided link (or click here to view a PDF version). Additionally, please do not forget to subscribe to our latest news and research for the most relevant institutional insights on digital assets and the top digital assets by market cap.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Bitcoin Drives a Rebound as Breadth Narrows

The CF Free-Float Broad Cap Index rose 4.44% in July as Bitcoin and Ether supplied 5.07 points of a 4.44% return. Softer inflation and new Ethereum exchange-traded product access carried the large-capitalization core, while 18 of 32 constituents fell and free-float weighting produced the gain.

Mark Pilipczuk

Changes to the Token Market Price Benchmarks Series - Market Prices – 04 August 2026

Changes to the Token Market Price Benchmarks Series - Market Prices – 04 August 2026

CF Benchmarks

Cooler Inflation Sparks Rebound as Hike Risk Persists

A 3.5% CPI print, three hawkish FOMC dissents, and renewed Iran strikes drove a broad rebound across digital assets in July. Every CF Benchmarks index rose, fund flows turned positive at $409 million after eight weeks of outflows, and crypto diverged from tech as the Nasdaq fell 3.2%.

Mark Pilipczuk

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.