Dec 31, 2025

What a Huge Wall of Filings Tells us about the Next Wave of US Crypto ETFs

A massive raft of filings points to US crypto ETF launches accelerating in 2026, with many familiar trends continuing - and a surprising new one emerging.

“Tidal Wave” Coming

Approaching the two-year mark of the first U.S. spot Bitcoin ETFs seems like a reasonable juncture to review the current state of live crypto ETF filings for the last time in 2025.

Here’s the best-known list, as shared by Bloomberg’s James Seyffart and Eric Balchunas:

NEW: Have an updated version of this chart. Corrected some dupes and added at least one missing filing. Honestly -- I'm almost certainly missing filings. The total number is likely higher than 125. https://t.co/lhcHScensJ pic.twitter.com/NaAMhZy6sv

— James Seyffart (@JSeyff) December 11, 2025

Bitcoin Malaise

The backdrop is overshadowed by the market’s anchoring asset Bitcoin floundering ~0.9 of a standard deviation off its ~$126k record. (NYU’s GARCH model. Note: ~1𝛔/1-year BTC drawdowns are historically normative for BTC.)

The market might look different by the time the SEC works through this wall of filings. At least for now though, this is the climate into which issuers are intent on pumping more inventory.

Liquidations Likely

That adds backing to a first high-probability assumption on the trend of listed crypto products in 2026, as noted by the Bloomberg analysts: liquidations are likely to increase.

With moderate U.S. crypto ETF attrition already emerging over the last several months, further ‘wastage’ would not be surprising.

It is the concentration of interest in specific assets, the overall tenor of the filings slate, plus the regulatory undercurrents facilitating this stepped-up wave of paperwork that are more interesting.

We’ll take a closer look at these points a little lower down.

GLS Triggers More

It was the instigation of Generic Listing Standards (GLS) in September that formalized the more accommodative but still prudent regulatory pathways needed for the asset class to grow way beyond Bitcoin and Ether within exchange listed wrappers.

Click below to read a concise overview of Generic Listing Standards by CF Benchmarks Head of Research Gabe Selby, CFA

As the list we shared above shows, issuers are building a dense pipeline across dozens of tokens—anchored by persistent demand for BTC and ETH, and an ascendant second tier led by SOL and XRP.

This means the competitive edge is migrating away from “getting exposure” and toward how exposure is engineered: including eligibility signals, governance-grade benchmarks – like those published by CF Benchmarks, with demonstrably representative liquidity – increasingly all alongside staking and yield design.

Worth underlining: Bloomberg’s early-December tally was only a snapshot. At the time of writing at the end of December, the count has risen, if not materially.

Concentration

With a broader palette of ETF-eligible crypto assets now fully telegraphed by the SEC, it’s helpful to take a closer look at the filings slate to get an idea of what applicants are doing with this broader permission—i.e., where issuer focus has been concentrating.

Where filings are clustered

Issuer attention is now split between what we can describe as:

- Core allocation exposures: the assets and structures issuers expect to sit at the centre of mainstream portfolios—high-liquidity, institutionally legible exposures where competition is increasingly about wrapper design (fees, structure, distribution) rather than “does this belong?”

- Second-tier exposures: the next set of protocol bets that sponsors are positioning as plausible “portfolio primitives” beyond BTC and ETH—still relatively liquid and widely held, but where regulatory eligibility, market-structure maturity, and standardization (benchmarks, custody, surveillance) are more determinative of the path to scalable distribution.

- “Optionality” filings: these are a ‘long tail’ of opportunistic filings, aiming to test the eligibility boundary, and distribution appetites.

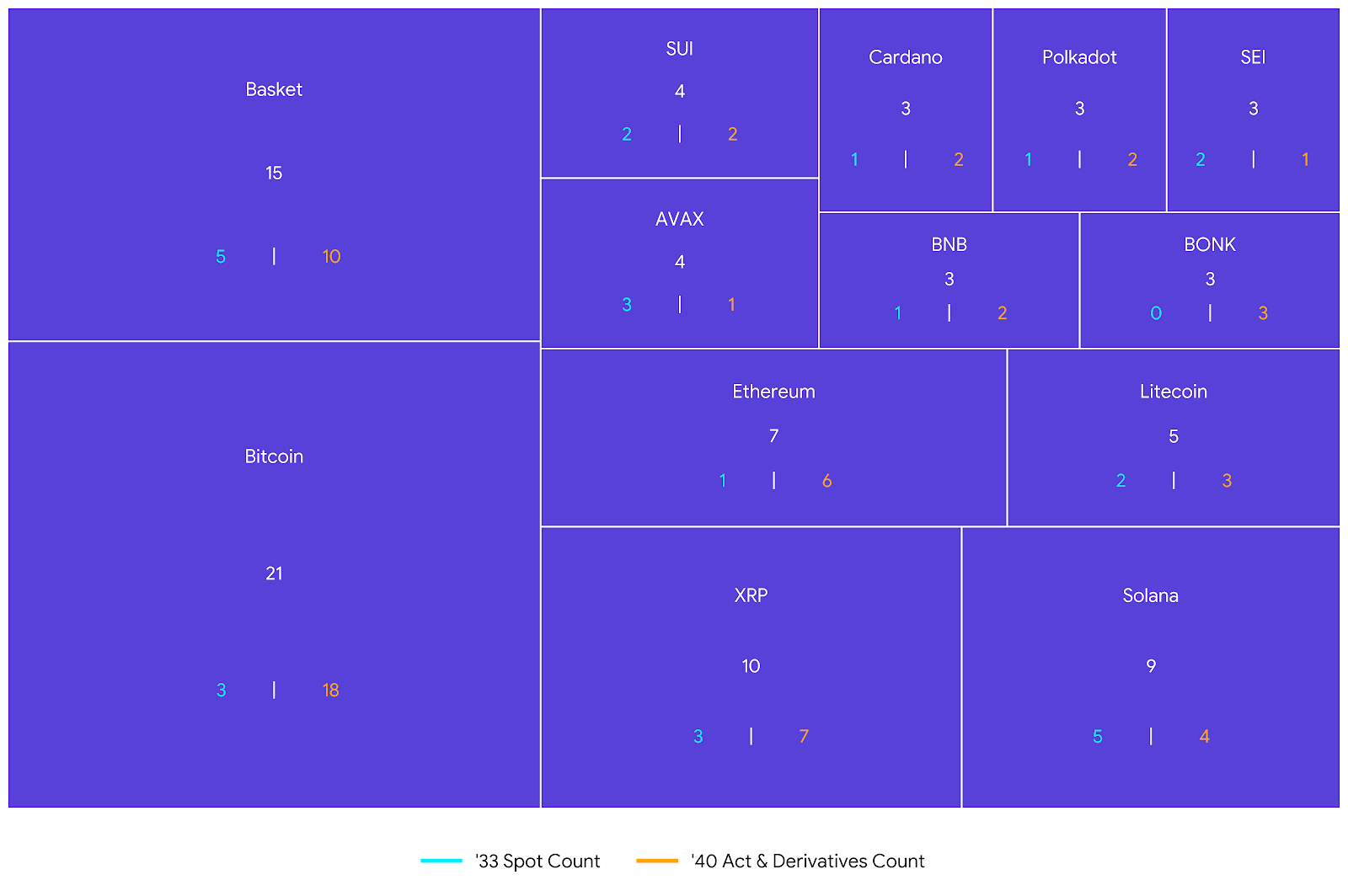

To facilitate absorption of of these clusters further, we’ve repackaged the filings slate into the ‘heat map’ below.

Active crypto asset ETP filings by asset as of December 11th, 2025

The Obvious Takeaways

They're still worth noting.

- Catalogue expansion: This voluminous filing count reflects the impact of the hard-won regulatory gains of the past few years: chiefly evidenced by strengthened issuer confidence. Sponsors now view crypto ETPs as a repeatable manufacturing process.

- ‘Core beta’ additions: While BTC and ETH axiomatically remain ‘core beta,’ it’s also clear that SOL and XRP have become the next most crowded tier of mainstream demand.

- Baskets are the institutional format: The rise of rules-based multi-asset construction is coinciding with indications that distribution is slowly beginning to move onto platforms and model portfolios. No causality can be claimed for now, but fiduciaries’ historical preference for diversified exposure is well documented.

The Surprising ’40 Act Fightback

It’s when we examine the ‘regulatory lanes’ where live filings are pooling that the most surprising and counter-intuitive concentration emerges.

With the snapshot showing 124 filings, split between 42 ’33 Act spot applications, and 82 proposed ’40 Act spot and/or derivatives-based funds, the bias is clear.

It’s important to outline why these new signs of ’40 Act prevalence go against the grain and the direction of travel for crypto ETPs.

Crypto’s ’33 / ’40 Inversion

First off, note that for traditional assets (stocks, bonds, etc.) – investors have historically favored ’40 Act ETPs over ’33 Act ETPs. Crudely speaking, investors have generally regarded investor safeguards as higher in the former vs. the latter.

One major observation from the relatively short history of crypto ETPs though, is that the trend and apparent market preference have generally been in the opposite direction.

The first crypto-related U.S. ETF, ProShares’ Bitcoin ETF (BITO) was a futures-based ’40 Act ‘strategy’ fund, followed by several others.

But with Bitcoin’s longstanding categorization by issuers as a commodity, and the widely held view that futures-based commodity exposure is essentially less efficient than spot, the bigger push in crypto has been to list spot-based crypto ETFs. The sense of achievement in the space when the first Bitcoin ETFs came to market in January 2024 underlines this inverted preference.

So, the apparent emergence of the opposite prevalence among live crypto fund filings – a move towards the ’40 Act structure – is a surprise; and worth watching.

’40 Act Hints in ‘25

The numerous ’40 Act crypto ETFs listed in 2025 could count toward this counter trend.

Note: many of these funds, reference our regulated benchmarks, e.g., REX Osprey’s, ESK, SSK, DOJE and XRPR.

Why ’40s are favored

It’s notable that the REX funds stole a march on all ’33 Act filings by making their market debut earlier than rivals.

This was largely due to specific regulatory idiosyncrasies of the ’40 Act that can permit effectiveness to be triggered automatically after statutory windows have lapsed.

One tentative suggestion is that a structural rotation back towards the ’40 Act wrapper might be emerging. Key attractions would include:

- Potential for faster, nimbler, and lower-friction issuance

- More customizability for shaping payoff profiles (i.e., funds aren’t limited to spot)

- The expectation that some platforms may favor the more familiar compliance and risk framework of ’40 Act funds

This all suggests the enactment of Generic Listing Standards – in itself – did not enable the wider expansion of fund asset types and other desired facilities as quickly as expected.

Firms may be hoping that a combination of ’40 Act flexibility and GSL permissiveness could turn out to be the clincher.

What the Paperwork Says

Let’s now examine the raft of paperwork from the perspective that it should continue to signal where investor appetite is now, and where it’s seen heading.

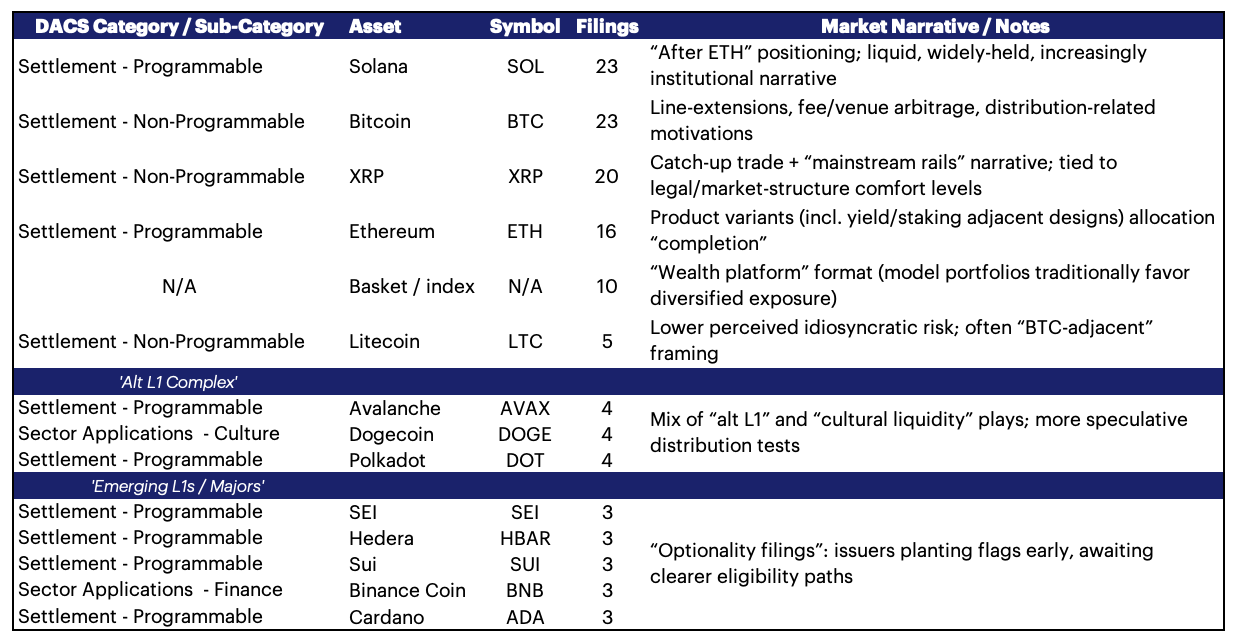

In the table below, we’ve summarized assets per the number of filings, alongside our take on the narratives surrounding each protocol.

For additional clarity on the types of protocols garnering attention, we’ve also specified the CF DACS Category and Sub-Category of each token.

Crypto ETF Filings by DACS Classification - December 2025

Click here to read more about the CF Digital Asset Classification Structure (CF DACS).

The easiest takeaway from this slice: through the lens of CF DACS – the most objective and trusted digital asset taxonomy – it is clear that attention remains tightly clustered within relatively contained themes.

To an extent, this is cogent as the product class enters only its third year of existence.

Four more big crypto ETF trends to watch in 2026.

1. Eligibility is the real battleground: The active-filings split seems to reinforce this: when the market is uncertain about the shortest path to scalable distribution, sponsors increasingly default to structures that can iterate faster—while keeping spot filings alive where they believe eligibility is converging.

2. Staking normalization: With “carry” as the next clearest differentiator in focus as spot beta commoditizes, demand for yield-bearing structures should accelerate a broader adoption of solutions on reward treatment, slashing risk, counterparty exposure, potential conflicts, and similar issues, and how they’re reflected in NAV and disclosures.

3. Payoff engineering: The broader move towards ’40 Act/derivatives structures is consistent with sponsors prioritizing greater flexibility in how gross returns are structured: e.g., buffered, covered-call, and other risk/return mechanisms

4. Indices/baskets as Trojan horse for mainstreaming: The multi-asset format maps more naturally to investment committee logic, and to model portfolio implementation. “Basket” is the second-largest active category, characterized by a meaningful ’33 spot component but still majority ’40/derivatives. That’s consistent with the view that diversified crypto is becoming the default distribution format—especially as advisors and gatekeepers seek committee-defensible allocations.

Conclusion

This wall of filings can be read as a single message: the U.S. crypto ETF space has moved into a scaled product cycle, with issuers building inventory across a clear hierarchy of core exposures, second-tier candidates, and “optionality” tests, while increasingly differentiating through structure and distribution, as much as through the underlying asset. As 2026 approaches, the agenda is standardization—clearer eligibility pathways, more repeatable operational models (including staking and yield, where viable). Plus, greater use of basket/index formats that map cleanly to portfolio construction—placing the premium on institutional plumbing: benchmark integrity, representative liquidity inputs, and governance that can withstand scrutiny at scale.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.