Jan 02, 2026

Data Delays & Defensive Tilts

Key takeaways for the month

The year closed with cautious easing and ongoing market-structure upgrades. The FOMC cut rates by 25 bps, while meeting minutes revealed a deep divide among voting members of the committee. Bitcoin remained choppy and range-bound, oscillating around $90k, as risk-off sentiment persisted. The month was shaped by a swath of key macro releases, including a surprisingly strong GDP print and softer-than-expected inflation alongside delayed payrolls and retail sales, blurring the growth-inflation picture amid seasonally low liquidity and year-end tax-loss harvesting. With visibility low, investors de-risked: flows turned selective, relative strength narrowed to mega-caps, and bid-ask depth thinned across higher-beta tokens. Implied and realized volatility compressed relative to last month, consistent with low-conviction investor sentiment, while discretionary risk budgets were conserved pending cleaner data and clearer guidance on the 2026 easing path.

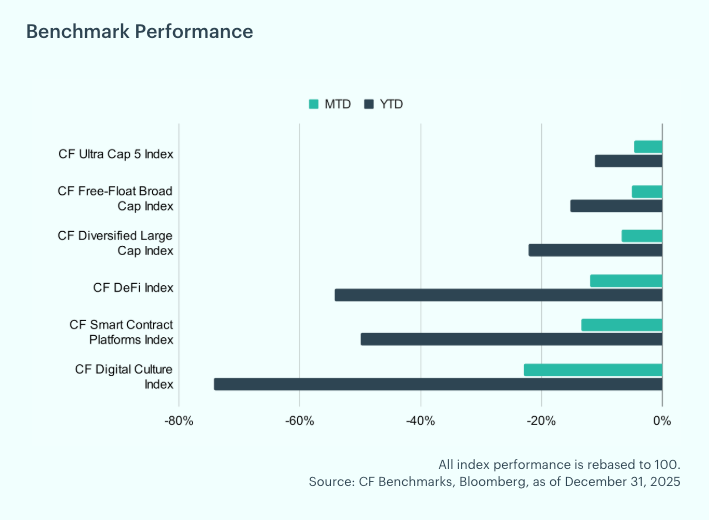

Higher Beta, Deeper Drawdowns: Index performance reflected this defensive posture. The CF Ultra Cap 5 Index fell 4.63% month-to-date (YTD: −11.24%), while the CF Free-Float Broad Cap and CF Diversified Large Cap declined 5.11% (YTD: −15.25%) and 6.72% (YTD: −22.14%), respectively. Higher-beta cohorts led losses: CF Smart Contract Platforms −13.44% (YTD: −50.00%), CF DeFi −12.02% (YTD: −54.25%), and CF Digital Culture −22.90% (YTD: −74.26%). Mega-caps again proved relatively resilient, but the complex finished the year materially lower across risk tiers, with leadership narrowly concentrated in the most liquid, institutionally held names.

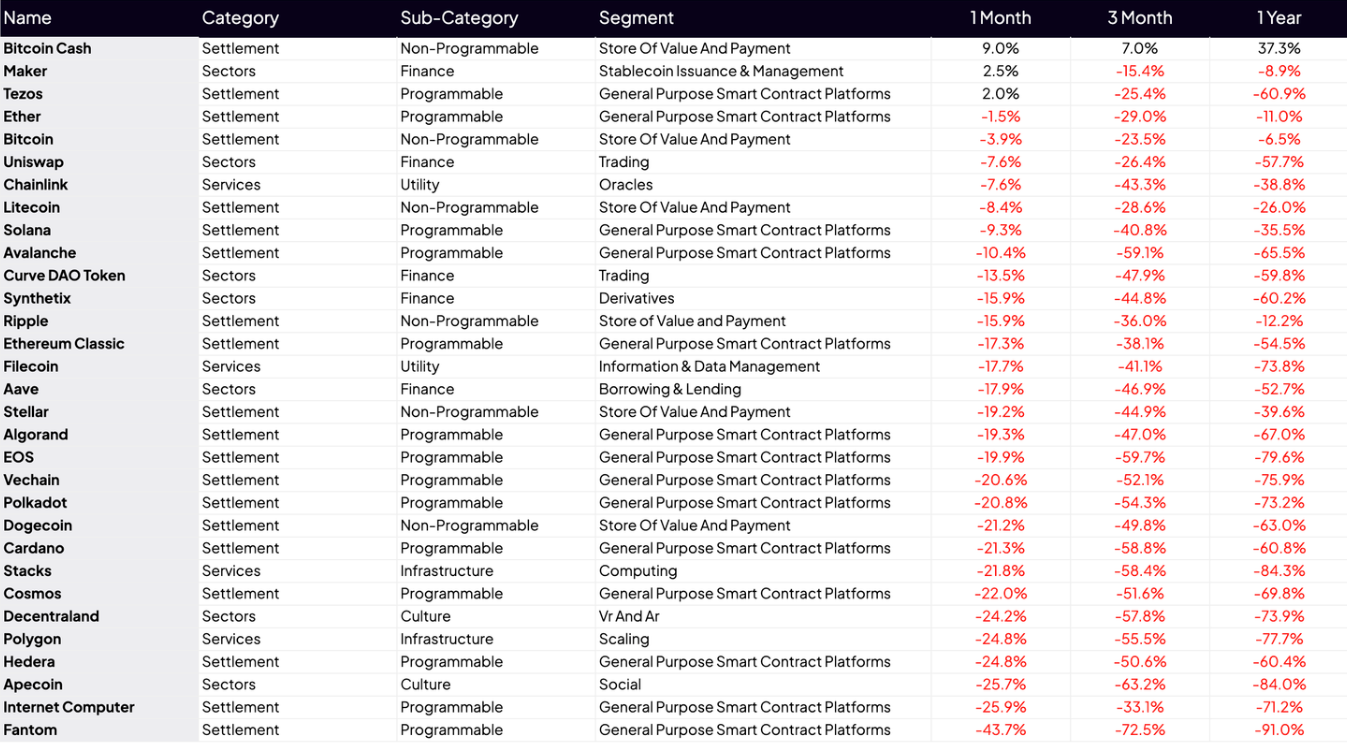

Individual Movers: Bitcoin Cash (BCH) led the pack in December with a 9.0% monthly gain, supported by renewed network attention tied to inscription activity. The Blue chip DeFi protocol Maker (MKR) followed, up 2.5%. Tezos (XTZ) rounded out the top performers with a 2.0% advance, helped by a late-month upgrade aimed at higher throughput and faster confirmations. Fantom (FTM) was the weakest performer, down 43.7%, pressured by ecosystem liquidity/TVL erosion. Internet Computer (ICP) fell 25.9%, weighed by lingering a supply unlock overhang. ApeCoin (APE) declined 25.7% as governance uncertainty and ongoing token supply dynamics continued to dampen sentiment.

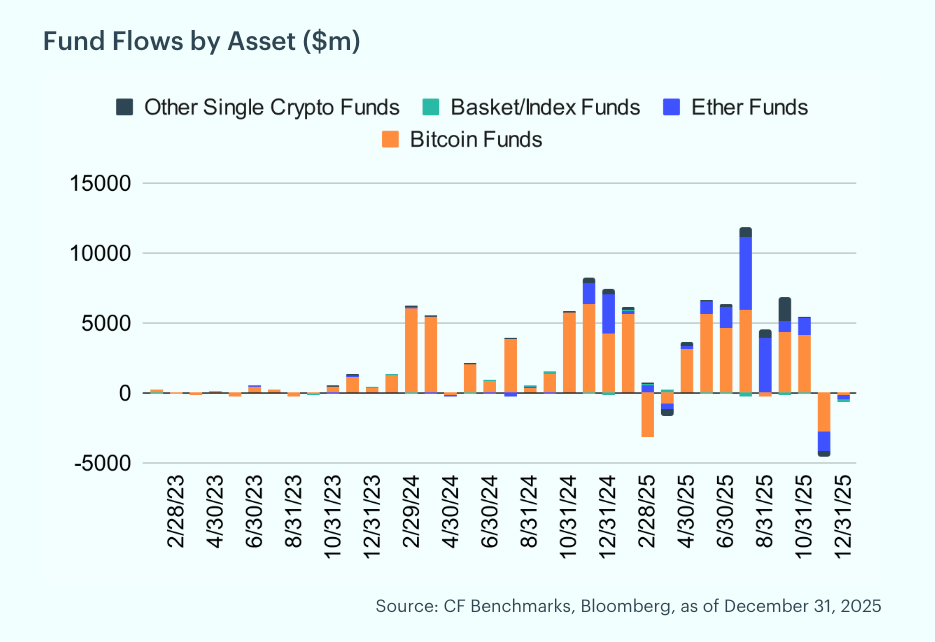

Outflows Persist: December recorded further outflows from digital asset funds, with investors redeeming approximately $687 million. Ether accounted for the largest share at $275 million, while Bitcoin followed at $204 million. Regionally, North America drove the majority of redemptions at roughly $985 million, while Europe experienced inflows of $175 million, underscoring the concentration of selling pressure in U.S. markets.

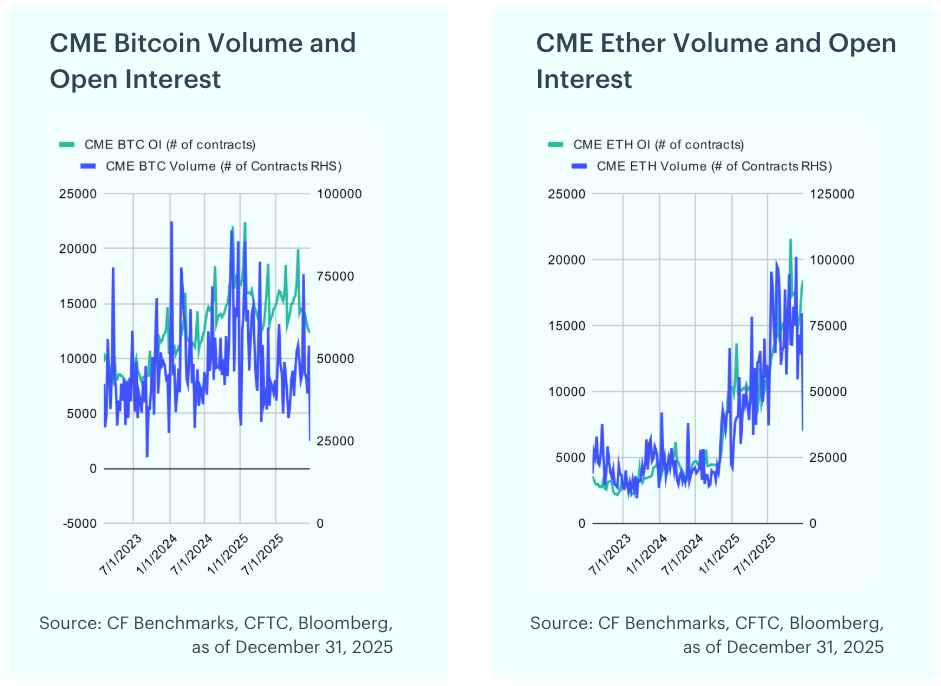

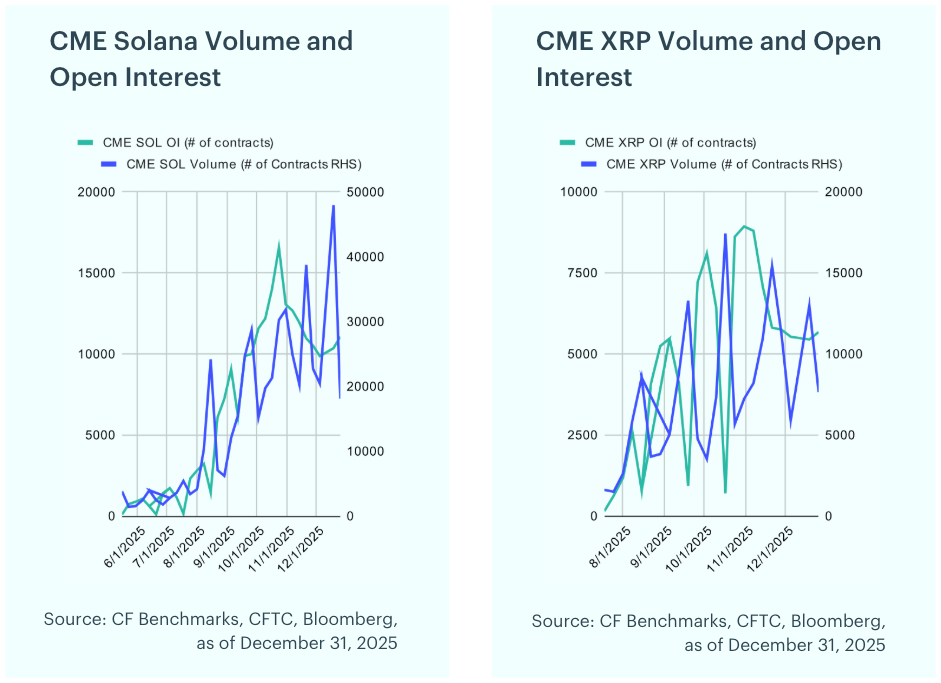

Mixed Signals Across Futures Markets: Bitcoin futures saw a modest decline in open interest during November, falling 11.7% from 14,029 to 12,383 contracts. Ether futures recorded a notable increase, with open interest rising 14.9% to 18,452 contracts, despite a modest decline in trading activity that peaked at 79,818 contracts toward month end. Meanwhile, Solana and XRP futures posted smaller changes following November’s pullback. Solana’s open interest rose 5.3% to 11,067 contracts as volumes approached 48,000 contracts, while XRP’s open interest declined 1.3% to 5,671 contracts, with volumes edging modestly higher.

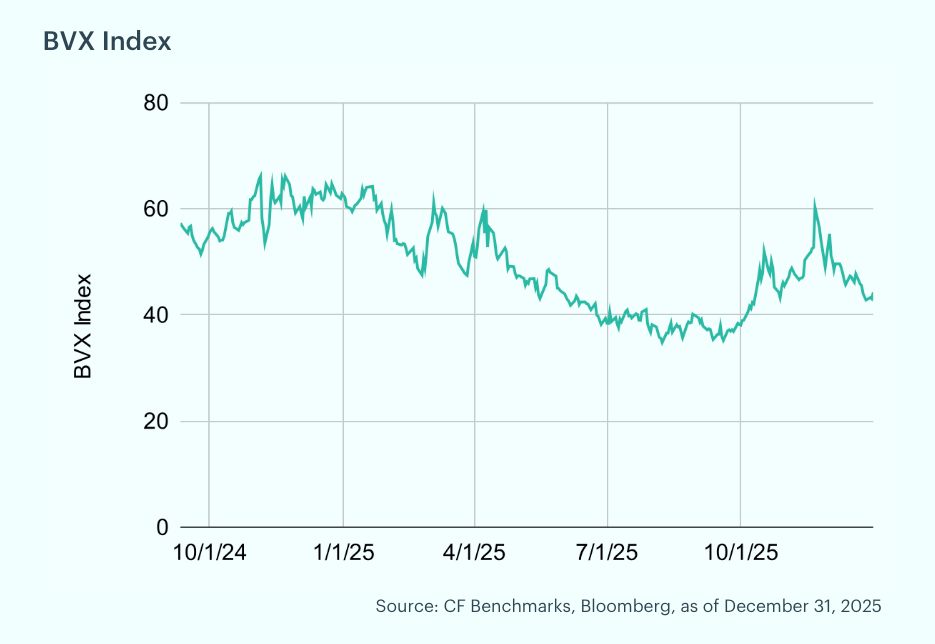

Bitcoin Volatility Compresses: The CF Bitcoin Volatility Index Settlement Rate (BVXS) is a daily benchmark that provides a forward-looking, 30-day constant-maturity measure of implied volatility, derived from CFTC-regulated Bitcoin option contracts traded on the CME. The BVX reflects the fair strike of a variance swap. Over the past month, the BVX ranged between 42.8 and 55.3. During this period, volatility declined significantly, with the BVX recording a -1.7 sigma move (based on our rolling 30-day z-score) late-month.

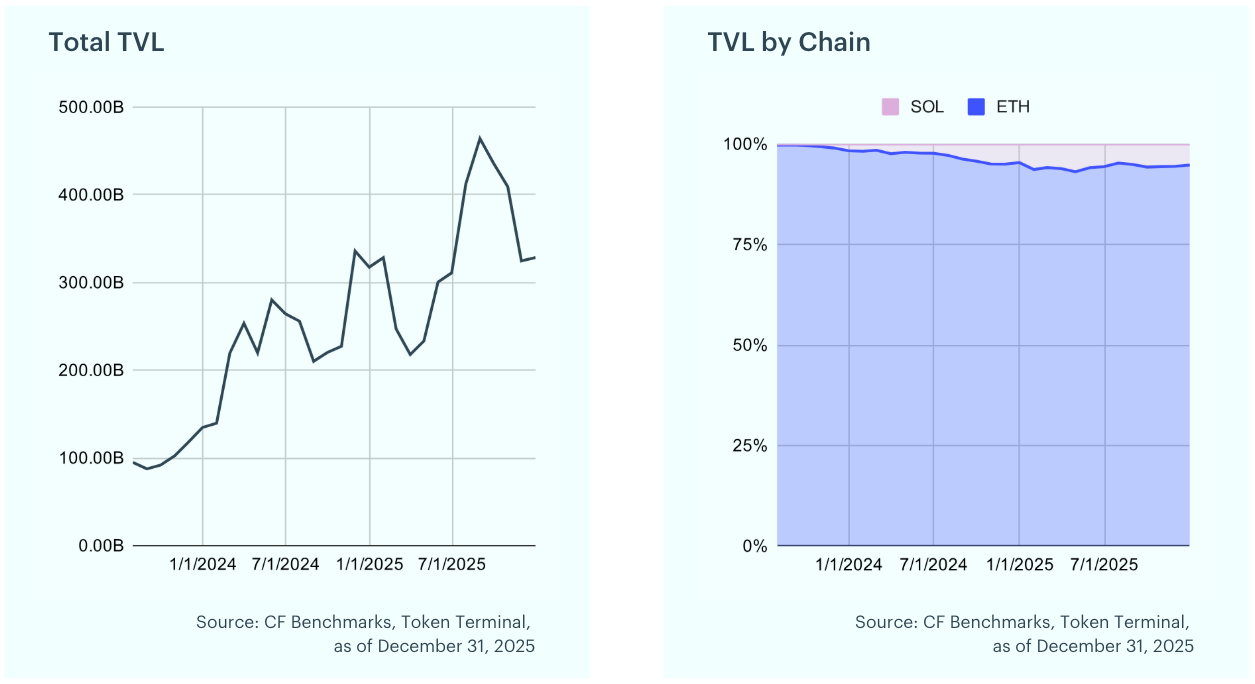

DeFi TVL Stabilizes After November Drawdown: Total Value Locked (TVL) in decentralized finance (DeFi) represents the aggregate value of assets deposited across DeFi protocols, expressed in U.S. dollars. It serves as a key indicator of the sector’s overall health and growth. Over the past month, total DeFi TVL increased by 1.2% to approximately $328 billion, as Ether and Solana began to stabilize following their November pullbacks.

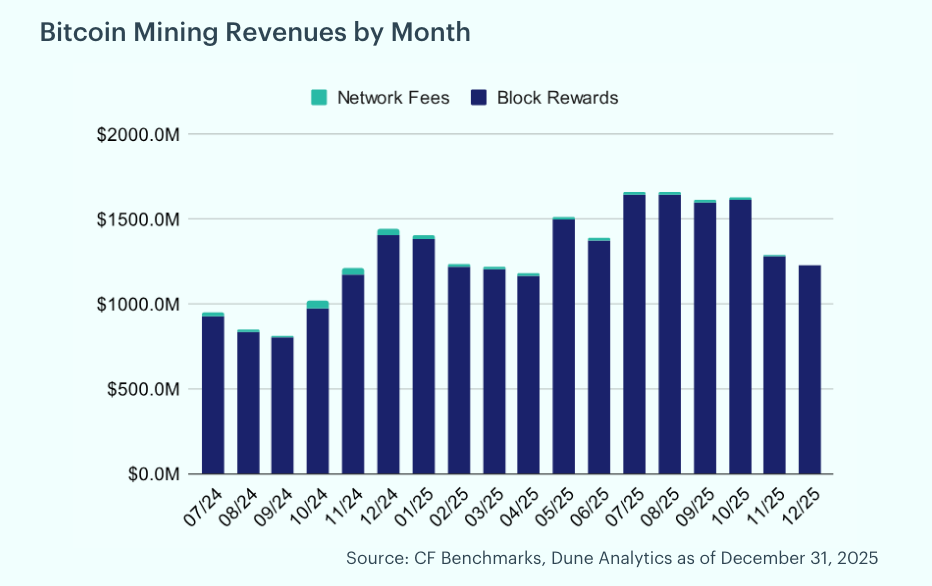

Miner Revenue Slips as Price Pressures Persist: Bitcoin miners saw a 4.7% decrease in revenue in December. Of the total rewards earned during the month, 0.6% came from transaction fees, down from 0.7% in November. The slight decline in revenue was driven primarily by Bitcoin’s price movements during the period.

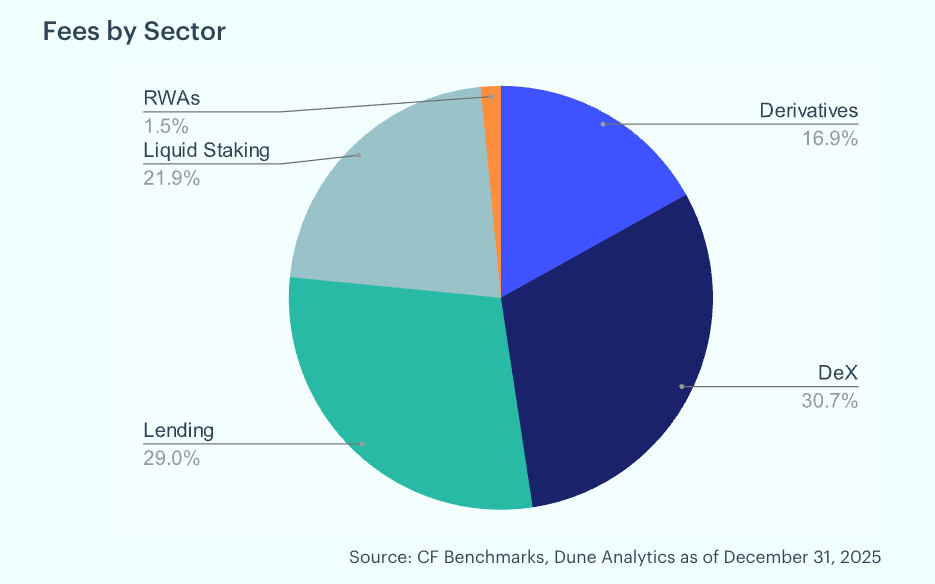

DEXs Still Dominate as Fees Compress: Analyzing Ethereum’s total fees and their sector composition provides insight into the use cases driving network revenue. Ethereum layer-1 fees dropped 51.2% month-over-month, falling to $11.5 million in December from $23.6 million in November. Decentralized exchanges accounted for the largest share at 30.7%, followed by lending protocols at 29.0% and liquid staking at 21.9%. Derivatives contributed 16.9%, while real-world asset tokenization represented just 1.5%, underscoring the continued dominance of DEX activity in network fee generation.

To read the complete report, kindly click on the provided link (or click here to view a PDF version). Additionally, please do not forget to subscribe to our latest news and research for the most relevant institutional insights on digital assets and the top digital assets by market cap.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Factor Friday - July 24, 2026

Beta's four-week grind higher stalled this week as style leadership rotated again: Momentum took the top spot, last week's leader Value fell to the bottom, and Growth stayed July's weakest factor. Size remains the only style factor positive on the year; beta, not style selection, is setting returns.

Mark Pilipczuk

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.