Dec 11, 2025

Kalshi Leads Surging Crypto Event Contract Market, Powered by CF Benchmarks

Kalshi’s CFTC‑regulated event contracts, anchored to CF Benchmarks indices, are standardizing binary crypto payoffs—turning market probabilities into a first‑class dataset.

Prediction Trading Is having a Moment

The exponential surge in prediction trading volumes has been one of the most remarkable turnouts of the year.

Notional combined weekly volumes on the two leading platforms, CFTC-regulated Kalshi and Polymarket (a decentralized blockchain-based platform) hit consecutive record highs in mid-October – reported by Bloomberg here, and cited in a report by Crypto.com here – topping out in the week ending October 20th, at $2.3 billion. That’s above the roughly $1.9 billion prior record set on November 4th, 2024, the day before the U.S. Election.

With January-to-October 2025 nominal prediction market volumes of around $28 billion, total 2025 volumes are likely to be close to $30 billion. That compares with the $16.3 billion annual nominal volume traded on Polymarket alone in 2024.

Building for Continued Explosive Growth

Against this backdrop of surging demand, the seemingly continuous stream of deal news in the space right now is unsurprising.

Whether it’s the recent raft of announcements by leading prediction market operator Kalshi, about deals with Google, CNN, CNBC and others; trading platform operator Robinhood launching a derivatives exchange with market maker Susquehanna, aiming to expand its range of prediction contracts; or London-listed Plus500 becoming the clearing partner for CME Group and FanDuel’s new event contracts platform - it’s increasingly clear operators are building the infrastructure for continued market growth.

Regulated players

This explosive growth has been accompanied by the increasing advent of regulated entities in the space, both established—chiefly CME Group—and emergent—like Kalshi Inc., which received its Designated Contract Market (DCM) authorization in November 2020.

As the first, and so far, the only, DCM focused exclusively on prediction trading, Kalshi has gained an outsized level of attention, and, predictably, the lion’s share of the regulated portion of the market.

This has made Kalshi the de facto model for prospective entrants into that market, particularly those inclined towards the regulated pathway. Potential newcomers may be existing DCMs (or less commonly SEFs) as well as those seeking regulated status, as the most straightforward way of participating in the prediction market opportunity with the least amount of friction.

The Crypto Element

More broadly, digital asset platforms are the most notable subset of both recent and likely upcoming prediction market entrants. Combined with Polymarket’s use of blockchain architecture to offer markets tied to both crypto and real-world assets, a deepening convergence with digital asset markets is among the easiest trends to predict.

Kalshi’s Edge

Meanwhile, founded in 2018, Kalshi's seven-year headstart has provided it with deep market, customer, commercial, and legal expertise, contributing to its significant lead over rivals.

Among a wide range of prediction markets Kalshi offers, its crypto segment—for which CF Benchmarks is the proud provider of regulated indices—is a critical element.

While Kalshi does not publicly break out segment volumes, reported figures (e.g., from Cointelegraph, here) suggest its aggregate trading volume has expanded rapidly in 2025. The platform recorded approximately $4.5 billion in monthly trading activity in late 2025, up from around $1 billion per month earlier in the year and seen running at a multi-tens-of-billions annualized pace by year-end.

With Kalshi’s recent tokenization launch targeting liquidity pools estimated to be billions of dollars deep, the crypto segment is evidently non-trivial, even if, for now, it’s smaller than the firm’s core macro, politics, and sports offerings.

Kalshi’s focus on the crypto segment and choice of CFB’s regulated benchmarks for contract settlement, strongly points to it having determined that price transparency, reliability and trust are an increasingly important competitive differentiator.

The Opportunity

All told, now seems to be a timely juncture to explore the exact nature and scope of the crypto prediction market opportunity, within the domain of U.S. regulations, where Kalshi is the dominant player.

Event Contracts vs. Prediction Markets

In the regulated domain, the distinction between more broadly defined ‘prediction markets’, and the specific product class known as event contracts, is critical.

Event contracts sit at the intersection of derivatives and prediction markets. They use market prices to express probabilities, but unlike most prediction markets, they are federally regulated, exchange-listed instruments, with auditable settlement sources. This distinction matters because institutional adoption depends on the quality of the benchmark, not merely the expressiveness of the event.

Event contracts (as listed on a CFTC-supervised DCM like Kalshi) therefore represent a subset of prediction markets—one engineered for financial-market use, supervised distribution, and replicable settlement. For regulated entities, the distinction is one that can’t be overlooked.

The Institutional Definition

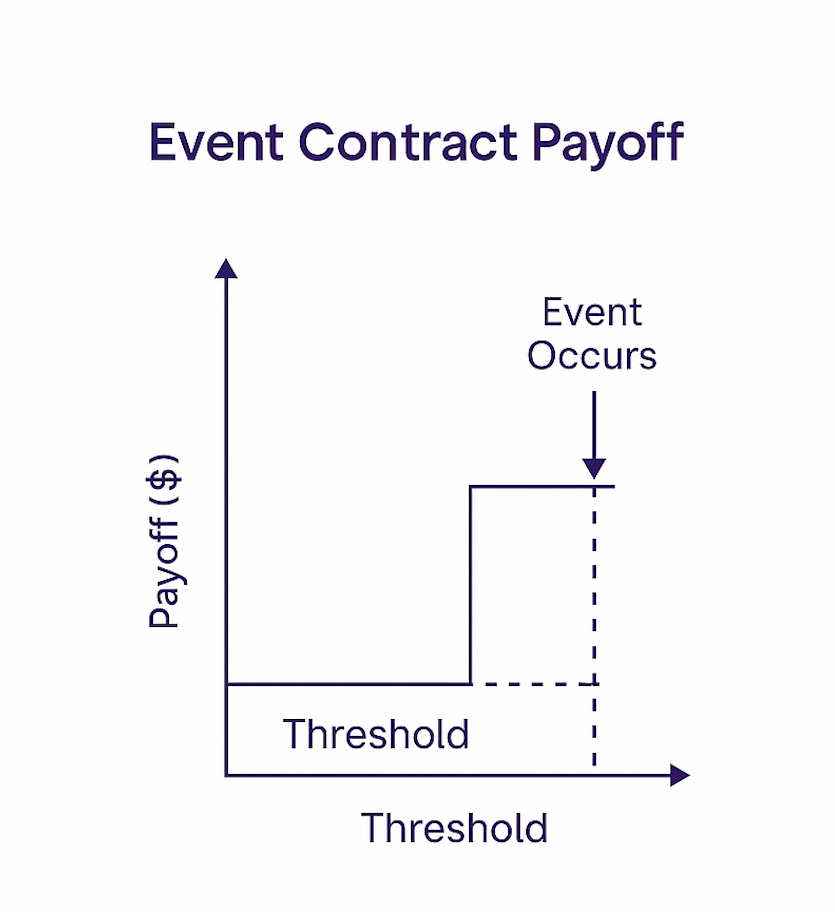

At their core, crypto-linked event contracts are identical to digital options: binary payoffs contingent on a reference price exceeding or remaining within a threshold at expiry.

If needed, see the schematic below for an intuitive visualization of the payoff mechanism in this option contract category.

The Institutional Solution

One reason why crypto event contracts now merit institutional consideration is the availability of auditable, manipulation-resistant benchmark settlement.

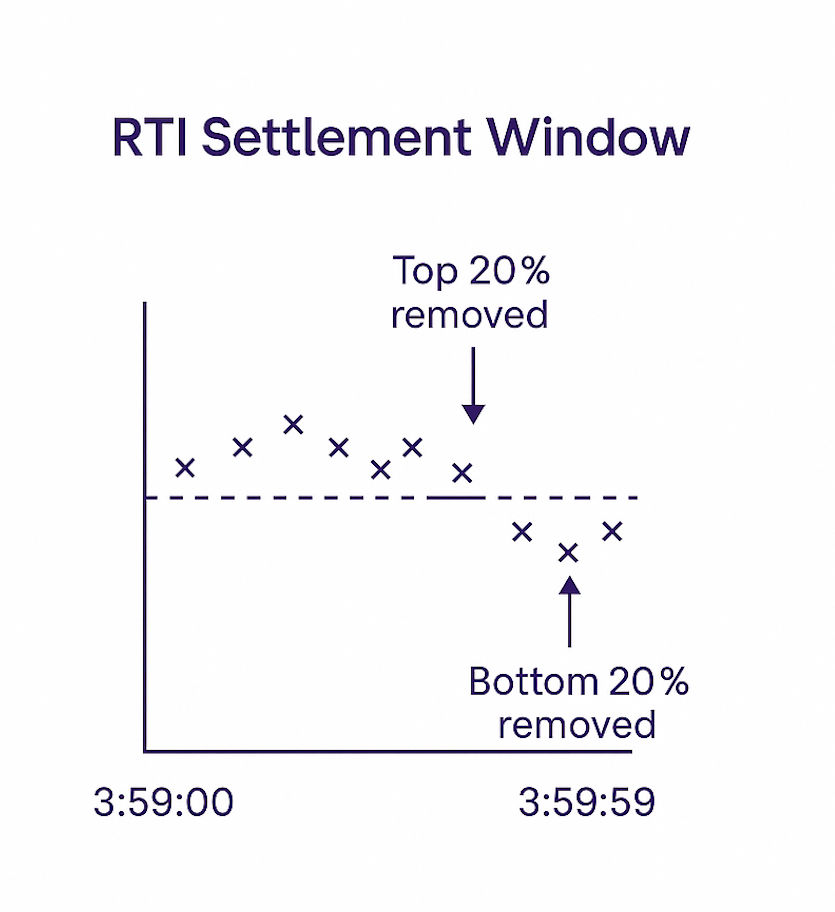

Kalshi’s crypto event contracts settle to CF Benchmarks Real-Time Indices (RTIs) using a one-minute window of per-second observations at expiry.

Additionally, trimmed averaging (excluding the top and bottom 20% of observations) is applied to certain markets, as illustrated in the schematic below.

This design minimizes expiry-pinning risk and anchors settlement to indices that already support regulated instruments, including CME futures and U.S. spot crypto ETFs.

For institutional desks accustomed to evaluating Greeks, slippage, settlement uncertainty, and control-function replicability, the presence of a BMR-authorized benchmark index (from CF Benchmarks) is the structural feature that allows event contracts to function like standardizable digitals rather than bespoke OTC wagers.

Benchmark Quality Defines the Product

Institutional adoption depends on the determinism of settlement. A U.S. event contract must settle to a source that is:

- Replicable (clear rules, observable data)

- Manipulation-resistant (averaging + trimming)

- Governed (index oversight, methodology, assurance reports)

- Compatible with risk controls (model inventory, valuation policies, independent checks)

CF Benchmarks’ RTI suite meets these conditions.

As a UK BMR-authorized Benchmark Administrator whose indices underpin global derivatives (e.g., all CME crypto futures and options) and ETF NAV processes (e.g. BlackRock’s IBIT) CFB provides exactly the kind of institutions already rely on.

In sum: event contracts without benchmark integrity are no better than entertainment oracles. Event contracts with robust benchmarks behave like—and are, in reality, on a regulatory basis—derivatives.

Market Structure Positioning

These characteristics enable crypto event contracts, such as those offered by Kalshi, to occupy a distinct slot alongside CFTC-regulated listed options, in terms of institutional suitability, compared to offshore prediction markets, as outlined in table below.

Below, we set out the key distinctions between crypto event contracts offered by Kalshi (settling to regulated CF Benchmarks RTIs) and other types of prediction markets.

- Cleaner regulatory perimeter than prediction markets

- Simpler Greeks footprint than listed options

- More transparent settlement than CFDs or offshore binaries

- More expressive calendar-risk hedging than perpetual futures or linear swaps

This combination—simplicity and benchmark integrity—explains why crypto-linked events have become an institutionally viable entry point.

The Emerging Event Contracts Data Product

An additional aspect of this fast-growing space is the emergence of data products based on regulated event contract trading.

Prediction-market probabilities are increasingly being treated as market signals. In 2024–2025, Google Finance and Google’s broader search platform began displaying event-market probabilities from regulated and offshore venues, marking the entrance of such data into the mainstream.

For crypto-linked event contracts—especially those settled to CFB indices—this inflection point transforms the data into a dataset.

Briefly, here are a few ways how:

- Traders read probability curves alongside price, OI, and ETF creations/redemptions

- Market makers incorporate calendar-event risk into short-dated vol. surfaces

- Desks track the crypto-ETF inflow/outflow implications of specific price thresholds

- Treasury teams at exchanges, miners, and corporates use the data to hedge quarter-end targets

This is the “information venue” thesis some analysts have highlighted (e.g., at Bernstein).

And again, it’s the benchmark, not the payoff, that determines whether these signals can be syndicated with credibility.

Institutional Use Cases

- Trading desks can use event contracts as time-bounded, low-notional digitals for calendar hedges.

- Risk & control teams benefit from deterministic settlement anchored to FCA-authorized benchmarks.

- Product teams at exchanges and fintech brokers can distribute CFTC-regulated event contracts without building a full options stack.

- Data teams can ingest event-market probabilities as structured signals for model enrichment.

- Crypto treasuries (exchanges, miners, corporates) can express clear quarter-end thresholds.

Event contracts cannot replace equity venues tomorrow—but their information layer already supplements traditional derivative markets today.

Conclusion

The investable simplicity of event contracts hides a kind of structural power. When built on a CFTC-regulated market and settled to robust CF Benchmarks indices, these contracts become institutional digital options, capable of generating tradable payoffs as well as market-implied probability data.

As distribution expands the core determinant of trust remains the same: a benchmarked, auditable source of settlement. In crypto, this is what can enable event contracts to evolve from a niche category into a credible component of market structure and a new class of financial data.

Selected References and Further Reading

Regulatory Foundations and Market Evolution

CFTC (2020). CFTC Designates KalshiEX LLC as a Contract Market.

https://www.cftc.gov/PressRoom/PressReleases/8321-20

CFTC (2022). Withdrawal of PredictIt No-Action Relief.

https://www.cftc.gov/PressRoom/PressReleases/8570-22

Reuters (2023). CFTC rejects Kalshi’s proposal to list political event contracts.

https://www.reuters.com/world/us/cftc-rejects-kalshi-political-event-contracts-2023-09-22/

PredictIt (2023). Legal Updates on PredictIt Case.

https://www.predictit.org/post/legal-update

Mainstreaming and Distribution

Bloomberg (2025). Google Finance to surface Kalshi and Polymarket data.

https://www.bloomberg.com/news/articles/2025-11-06/google-to-offer-kalshi-and-polymarket-data-on-finance-searches

The Block (2025). Bernstein: Prediction markets evolving into information venues.

https://www.theblock.co/post/377866/bernstein-prediction-markets-evolving-into-broader-information-venues-robinhood-kalshi-volumes-surge

Kalshi Growth

Cointelegraph (2025). Kalshi valued at $11B; monthly volumes exceed $4.4B.

https://cointelegraph.com/news/kalshi-valued-11-billion-after-latest-funding

Blockchain.News (2025). Kalshi reaches ~$1B monthly volume earlier in the year.

https://blockchain.news/flashnews/kalshi-prediction-market-reaches-1-billion-in-monthly-volume-forbes-reports

CoinTribune (2025). Prediction markets approach ~$28B total volume by October 2025.

https://www.cointribune.com/en/kalshi-extends-prediction-market-reach-with-tokenized-contracts-on-solana/

Explore CF Benchmarks Single Asset Real-Time Indices and Settlement Rates

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.