Dec 14, 2025

CF Benchmarks Newsletter Issue 97

Write-off

For active yield-driven participation, where attention on chart indicators persists, signs that range compression are becoming entrenched among large and mega caps is becoming a key theme, following several weeks of downdrafts.

The chart for our usual Bitcoin proxy, a continuation model for prompt CME Micro Bitcoin futures (MBT) (settled to BRR) has not needed much editing since the last Newsletter edition a fortnight ago. The snapshot below is from just before the 4 pm Chicago close on Friday, December 12th.

CME Micro Bitcoin futures continuation (delayed data) daily, 22:00 UTC

As we suspected at the end of November, sentiment has baulked at the $92k-$98k range, where attention was established following consolidation (presumably, including lots of optimistic orders) between late-April and early-May - preceding the groundswell of constructive sentiment that wrought two record highs. Now though, the 200-day simple moving average persists in its recently appointed role of structural resistance at approximately $103k, reinforced by confirmed pivots (former supports) as well as the psychologically charged $100k handle.

P&L

Meanwhile, structural P&L anxieties are reportedly piling additional pressure on sentiment. Glassnode analysts say their multivariate cost-basis models for Bitcoin show more recent buyers are being pushed to the brink, particularly as longer-term holders increasingly opt to realize profits:

“During the recent bounce, >1-year holders increased their realized profit (30D-SMA) above $1B per day, peaking at a new ATH of over $1.3B. Together, these two forces—time-driven capitulation by top buyers and heavy profit-taking by long-term holders, explain why the market continues to struggle reclaiming the STH-Cost Basis.”

From Glassnode’s ‘The Week On-Chain’, Dec 10, 2025

Arbs Sidelined

Glassnode also echoes a widely reported reduction in overall Bitcoin liquidity, noting a drop of in its measure of 30-day spot relative volume to the lower bound of the range. Compounding this may be indications of sidelining from 'large' participants. Looking at Friday’s December contract Last Price at $90,315, the daily basis appears negligible and unpromising. (BRR printed at $90,145.06 on Friday). Assuming large scale desks participating in size will typically seek to hold till final settlement (December 26th) to lock-in relatively low-risk profit from the spread, Bitcoin doesn’t currently look like a particularly attractive market for this specific arb.

BVXS: Down Not Out

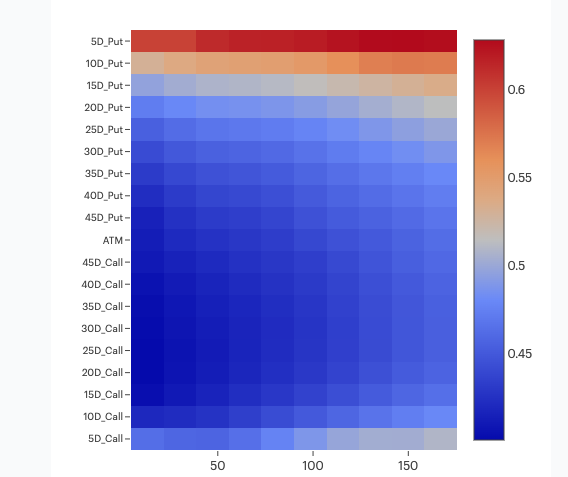

A more precise read of institutional Bitcoin sentiment can be garnered from our CME CF Bitcoin Volatility Index – Settlement (BVXS) page. The main chart depicts the gauge continuing to descend from ‘orange-alert’ highs around 60 on November 21st, closing this week at 45.67, and down around 2% on the day. From analytics available lower down on the page though – the Volatility Surface and 30-day constant maturity skew – it’s clear positioning remains skewed to downside protection at the front end: anxieties may have largely subsided, but the mood is still cautious.

The heat map from the BVXS page pictured below shows 5–15D put implied vols. sit near the 60% end, while equivalent-delta calls are closer to 45–50%.

CME Bitcoin options put/call heat map - 20:59 UTC, 12-12-2025

This looks like classic left-tail premium, consistent with demand for downside hedges, and dealers short downside gamma in very short tenors. Based on the snapshots alone, expectations seem tilted to continued chop at best, while dealer hedging warns of potential for further sharp dips. For sustained topside, this scenario needs to flip to call-chasing from put demand, and that’s not evident yet, from the surface alone.

The Big Picture for Large Caps

Insights from CF Benchmarks Quarterly Attribution Reports - December 2025

We can zoom out for a wider large-cap view with the aid of the Normalized Index Performance chart below. It's provided by CF Benchmarks Head of Research Gabe Selby, CFA, and Research Analyst Mark Pilipczuk, in their Quarterly Attribution Reports – December 2025, published earlier this week. It quantifies how much of a ‘write-off’ this quarter has been, likely setting the basis of sentiment, to a large extent, for the next.

Normalized Index Performance Chart - September - December 2025

Noting a quarterly outcome where greater diversification of exposure resulted in higher losses, the analysts said: “At the same time, correlations between digital assets and major equity benchmarks rose toward the 0.5 range, reinforcing crypto’s increasingly equity-like risk profile even as it maintained low correlations with bonds, currencies, and commodities.”

FOMC Splits

This scenario looks set to persist unless disrupted, positively or negatively by fresh fundamental catalysts. Particularly now that the most widely anticipated macro risk event of recent weeks, the Fed decision, on Wednesday, December 9th, has passed. It brought the third consecutive quarter-point benchmark rate cut, but the move had been rapidly priced in advance, when it became clear FOMC consensus was pointing lower.

Summarizing the main watch now, for potential near-term policy-driven sentiment, the CF Benchmarks Research team write:

Absent clearer evidence of disinflation any rebounds in large caps are likely to be tactical; however, with rate cuts now largely priced out, a sequence of benign data that delivers further disinflation without a growth scare could create meaningful upside alpha as markets scramble to reprice a renewed easing path.

From CF Benchmarks Quarterly Attribution Reports - December 2025

Separately, Pilipczuk had told Bloomberg ahead of the FOMC announcement that prices could receive fresh positive impetus if committee members’ views converged on the need for a further cut within months, rather than opting for a protracted period of assessment:

“We believe there’s some room for upside here should the Fed signal that there is potential for another cut before the June meeting. That becomes more likely if the labor market continues to soften and inflation expectations stay in the 2-3% range.”

Unfortunately, the possibility of such signaling faded post-decision, as officials voiced “strongly opposing views” on rates policy going forward in the wake of Wednesday’s cut.

Click below for a summary of the CF Benchmarks Quarterly Attribution Reports - December 2025 – or click the button to download the PDF version.

Read on for more institutional crypto insights and CF Benchmarks-related news, including:

- Kalshi leads white-hot crypto prediction market, powered by CF Benchmarks

- JPMorgan, Morgan Stanley float IBIT-tied structured notes

- ETF launch train accelerates, even as pipeline extends

Kalshi Leads Surging Crypto Event Contract Market, Powered by CF Benchmarks

Kalshi’s CFTC‑regulated event contracts, anchored to CF Benchmarks indices, are standardizing binary crypto payoffs—turning market probabilities into a first‑class dataset.

Below, we explore the nature and scope of the crypto prediction market opportunity, within the domain of U.S. regulations, where Kalshi is the dominant player.

Prediction Trading Is having a Moment

The exponential surge in prediction trading volumes has been one of the most remarkable turnouts of the year.

Notional combined weekly volumes on the two leading platforms, CFTC-regulated Kalshi and Polymarket (a decentralized blockchain-based platform) hit consecutive record highs in mid-October – reported by Bloomberg here, and cited in a report by Crypto.com here – topping out in the week ending October 20th, at $2.3 billion. That’s above the roughly $1.9 billion prior record set on November 4th, 2024, the day before the U.S. Election.

With January-to-October 2025 nominal prediction market volumes of around $28 billion, total 2025 volumes are likely to be close to $30 billion. That compares with the $16.3 billion annual nominal volume traded on Polymarket alone in 2024.

Building for Continued Explosive Growth

Against this backdrop of surging demand, the seemingly continuous stream of deal news in the space right now is unsurprising.

Whether it’s the recent raft of announcements by leading prediction market operator Kalshi, about deals with Google, CNN, CNBC and others; trading platform operator Robinhood launching a derivatives exchange with market maker Susquehanna, aiming to expand its range of prediction contracts; or London-listed Plus500 becoming the clearing partner for CME Group and FanDuel’s new event contracts platform - it’s increasingly clear operators are building the infrastructure for continued market growth.

Regulated players

This explosive growth has been accompanied by the increasing advent of regulated entities in the space, both established—chiefly CME Group—and emergent—like Kalshi Inc., which received its Designated Contract Market (DCM) authorization in November 2020.

As the first, and so far, the only, DCM focused exclusively on prediction trading, Kalshi has gained an outsized level of attention, and, predictably, the lion’s share of the regulated portion of the market.

This has made Kalshi the de facto model for prospective entrants into that market, particularly those inclined towards the regulated pathway. Potential newcomers may be existing DCMs (or less commonly SEFs) as well as those seeking regulated status, as the most straightforward way of participating in the prediction market opportunity with the least amount of friction.

The Crypto Element

More broadly, digital asset platforms are the most notable subset of both recent and likely upcoming prediction market entrants. Combined with Polymarket’s use of blockchain architecture to offer markets tied to both crypto and real-world assets, a deepening convergence with digital asset markets is among the easiest trends to predict.

Kalshi’s Edge

Meanwhile, founded in 2018, Kalshi's seven-year headstart has provided it with deep market, customer, commercial, and legal expertise, contributing to its significant lead over rivals.

Among a wide range of prediction markets Kalshi offers, its crypto segment—for which CF Benchmarks is the proud provider of regulated indices—is a critical element.

While Kalshi does not publicly break out segment volumes, reported figures (e.g., from Cointelegraph, here) suggest its aggregate trading volume has expanded rapidly in 2025. The platform recorded approximately $4.5 billion in monthly trading activity in late 2025, up from around $1 billion per month earlier in the year and seen running at a multi-tens-of-billions annualized pace by year-end.

With Kalshi’s recent tokenization launch targeting liquidity pools estimated to be billions of dollars deep, the crypto segment is evidently non-trivial, even if, for now, it’s smaller than the firm’s core macro, politics, and sports offerings.

Kalshi’s focus on the crypto segment and choice of CFB’s regulated benchmarks for contract settlement, strongly points to it having determined that price transparency, reliability and trust are an increasingly important competitive differentiator.

The Opportunity

All told, now seems to be a timely juncture to explore the exact nature and scope of the crypto prediction market opportunity, within the domain of U.S. regulations, where Kalshi is the dominant player.

Event Contracts vs. Prediction Markets

In the regulated domain, the distinction between more broadly defined ‘prediction markets’, and the specific product class known as event contracts, is critical.

Event contracts sit at the intersection of derivatives and prediction markets. They use market prices to express probabilities, but unlike most prediction markets, they are federally regulated, exchange-listed instruments, with auditable settlement sources. This distinction matters because institutional adoption depends on the quality of the benchmark, not merely the expressiveness of the event.

Event contracts (as listed on a CFTC-supervised DCM like Kalshi) therefore represent a subset of prediction markets—one engineered for financial-market use, supervised distribution, and replicable settlement. For regulated entities, the distinction is one that can’t be overlooked.

The Institutional Definition

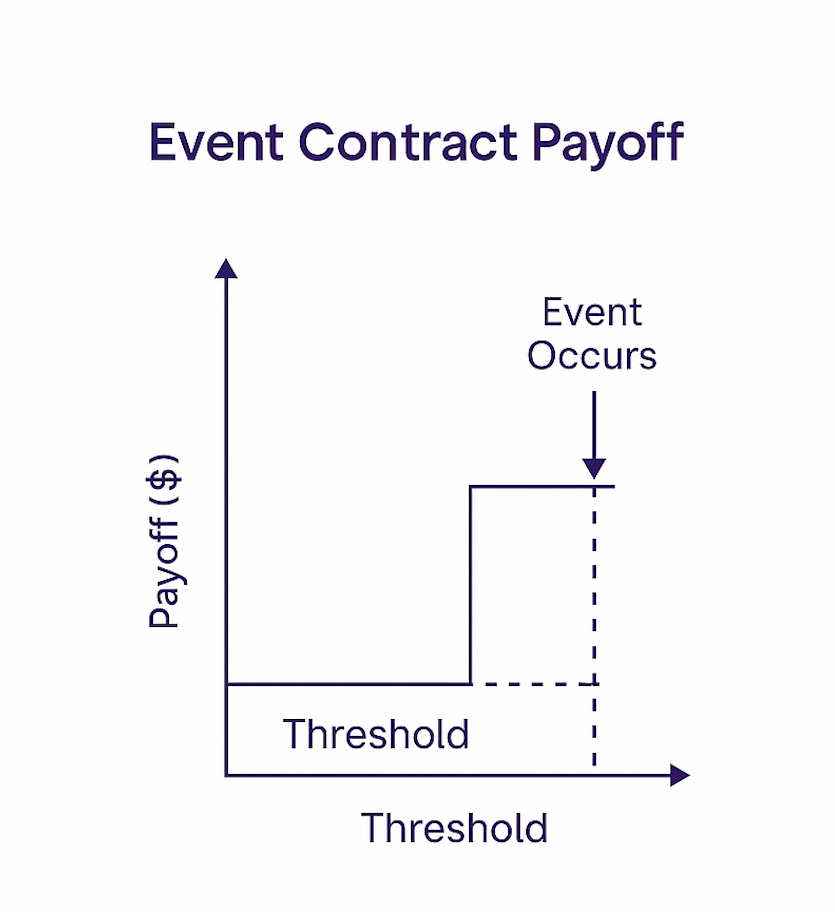

At their core, crypto-linked event contracts are identical to digital options: binary payoffs contingent on a reference price exceeding or remaining within a threshold at expiry.

If needed, see the schematic below for an intuitive visualization of the payoff mechanism in this option contract category.

If needed, see the schematic below for an intuitive visualization of the payoff mechanism in this option contract category.

US Crypto Product Launches Accelerate

With still well over 100 active U.S. ETF filings on the slate at the SEC, it's little surprise that the pace of new regulated product launches has gone up a gear up in recent weeks, even as the pipeline continues to extend. We summarize the CFB-related highlights below.

If 2025 proved crypto can live inside regulated wrappers, the last few weeks showed how quickly those rails are deepening. The CFTC has cleared the way for listed spot trading on federally supervised futures exchanges, the single-asset ETF set has widened (see XRP, SOL), index conventions keep converging on CF Benchmarks’ New York Variants, and ETFs are increasingly the underlier for bank-manufactured exposures. Add one more milestone: broad, rules-driven portfolio ETFs expanding automatically, as assets meet transparent inclusion criteria.

CFTC Opens Door to Spot Crypto on DCMs

- The CFTC announced that spot crypto products will commence trading on CFTC-registered Designated Contract Markets (DCMs)—a first for U.S. federally supervised crypto. (Press release)

- CF Benchmarks CEO Sui Chung framed the change as a pivotal step that brings spot trading into a regime institutions already trust—surveillance-rich, auditable, and rule-consistent. (See Bloomberg’s Dec. 9 Crypto newsletter)

- Why it matters: DCM-listed spot sits alongside futures under the same supervisory umbrella, improving price discovery, market integrity, and operational plumbing. This complements the CME CF New York Variant 4:00 p.m. ET fixes that anchor U.S. crypto NAVs, reducing frictions between end-of-day index marks and ETF creation/redemption workflows.

Franklin Crypto Index ETF (EZPZ) expands via IDAX

- Franklin Templeton has expanded its EZPZ crypto portfolio ETF from BTC and ETH to include XRP, Solana, Dogecoin, Cardano, Stellar Lumens, and Chainlink, following reconstitution of the CF Institutional Digital Asset Index – US – Settlement Price (IDAX).

- With EZPZ following a passive, rules-based methodology, and IDAX synchronized to Generic Listing Standards and other prudential filters (eligibility, liquidity, etc.) the result is an automatic large-cap diversification mechanism. When assets meet thresholds—they enter the index and the ETF, with no ad-hoc judgment calls.

- That’s the partnership working as intended: transparent rules, predictable outcomes, and a regulated wrapper – which, ordinarily, will continue to be filled as more assets reach the threshold for inclusion

Bitwise 10 Uplists to NYSE —Tied to CFB Methodology

- The oldest crypto portfolio product is now an ETF. The Bitwise 10 Crypto Index Fund is now the Bitwise 10 Crypto Index ETF (BITW) after uplisting to NYSE Arca from OTC, bringing diversified top-10 exposure to a regulated exchange.

- CF Benchmarks acts as 'Valuation Vendor'—providing 4:00 p.m. ET reference prices used for daily NAV across underlying assets.

IBIT Options Position Limits Widened

- Options on BlackRock's iShares Bitcoin Trust ETF (IBIT) the largest Bitcoin ETP in terms of assets managed, referencing CFB's CME CF Bitcoin Reference Rate - New York Variant (BRRNY) have been stepped up—with positions toward the 1 million contracts area now permitted.

- Why it matters: Higher caps typically tighten spreads and lower hedging costs for MM desks, improving the derivatives market quality around the ETF that now underpins multiple ETF-linked structured notes.

More XRP and Solana ETFs Debut - Benched to XRPUSD_NY and SOLUSD_NY

- Issuer momentum across single-coin funds continues, led by a raft of new XRP ETFs, including funds from Franklin Templeton, Bitwise, and 21 Shares.

- Convergence on XRPUSD_NY standardizes AP/dealer workflows to the 4:00 p.m. ET fix within CF Benchmarks’ IOSCO-aligned methodology—supporting replicability, manipulation resistance, and smoother primary/secondary alignment.

- New Solana ETF listings have also been in the spotlight, including vehicles referencing CME CF Solana-Dollar Reference Rate - New York Variant (SOLUSD_NY). These follow in the wake of Bitwise's Solana Staking ETF (BSOL), launched in late-October (its SOL price component comes from SOLUSD_NY). The choice of U.S. SOL ETFs now includes 21Shares's SOLUSD_NY-powered Solana ETF (TSOL).

- Allocator takeaway: Products that adopt CF Benchmarks’ New York Variants give trading desks a common, regulated EOD convention for hedges and performance cuts. By contrast, proprietary rates can be serviceable, but typically require additional methodology diligence and closer reconciliation for outlier handling.

BlackRock Preps Next ETH Fund Iteration

- The clock is now ticking on BlackRock's iShares Staked Ethereum Trust filing. Following the Trust registration in Delaware on Nov. 19, 2025, an S-1 has now been filed, dated December 5th.

- BlackRock’s iShares Ethereum Trust ETF (ETHA) uses CME CF ETHUSD_NY. Though details are unconfirmed, the staking-enabled variant is likely to retain the price-return anchor and book staking yield separately for clean NAV.

JPMorgan, Morgan Stanley Flag IBIT-Linked Notes

- New Bitcoin notes with payoffs keyed to BlackRock’s iShares Bitcoin Trust (IBIT) continue to roll out, now including paper from JPMorgan. It reflects a shift toward ETF shares as the default reference for structured products. (Coindesk's recap.)

- Morgan Stanley's roughly $104m in IBIT-linked structured notes was sold in November, reinforcing the trend.

- Benchmark provenance: With IBIT calculating NAV using BRRNY, notes priced off IBIT effectively inherit that same daily valuation convention, increasing the assurance of effective tracking, and of course, price-security and governance-based peace of mind.

Institutional Takeaways

- Regulated plumbing expands: With spot crypto moving onto DCMs, institutional desks gain surveillance-rich venues that interlock with futures and ETFs—tightening the loop between benchmarks, hedges, and NAVs.

- Rules-based breadth in a regulated wrapper: EZPZ’s IDAX-driven additions and BITW’s top-10 approach extend access beyond BTC and ETH, without bespoke due-diligence for every coin—methodology does the work.

- Index governance is the differentiator: As single-asset exposure scales (XRP, SOL), standardizing on CF Benchmarks’ New York Variants provides predictable daily marks, robust constituent-venue criteria, and tested outlier controls—lowering operational basis risk.

- Derivatives depth compounds access: Wider IBIT options limits and the rise of ETF-linked structured notes reduce friction for hedgers and wealth platforms that prefer notes or ’40-Act-adjacent wrappers over spot tokens.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.