Feb 03, 2026

CF Benchmarks Introduces CF Factor Data, Enabling Institutional-Grade Factor-Based Crypto Investing for the First Time

How our new CF Factor Data covering Growth and Value can be implemented for long-only digital asset portfolio investing.

Institutional Factor Investors are Coming

As digital assets mature and institutional adoption accelerates, it is cogent to expect that institutional investors will increasingly require the same facilities, frameworks and functionalities that are available for investing in traditional assets, when they're undertaking investments in digital assets.

More specifically, investors are likely to increasingly seek to quantify to a greater degree of certainty, the risk and return drivers of assets in the digital asset universe, how such exposures behave across regimes, and indications of how to govern those exposures over time – with the same ease and clarity that is achievable with traditional assets.

Our History of Factor Research

Meeting these anticipated needs has been the premise of CF Benchmarks’ long-running quantitative research on factor-based investing for digital assets.

This research has progressed at a steady pace, achieving several concrete milestones over a few short years. Beginning with the successful isolation and validation of robust risk premia within digital asset markets, followed by the construction of a factor model for digital assets, through Fama-French based time-series regression studies, and Fama-McBeth based cross-sectional regression studies, our work culminated in the introduction, in late-2024, of the first institutional grade factor model for digital assets.

This validated factor model supports the measurement of crypto risk premia and the decomposition of performance.

Next, in order to provide a functional framework through which the model could be practically integrated into a variety of institutional investment activities, CF Benchmarks launched, in June 2025, the CF Factor Data Series, the first factor-based product within our CF Factor Intelligence suite of data products.

The CF Factor Data Series is a systematic framework for understanding the drivers of return and risk in digital asset markets, providing a toolkit to enable performance attribution, portfolio construction, and thematic screening across a range of style factors.

As such, the CF Factor Data Series has operationalized CF Benchmarks validated factor model into daily, consumable data—factor premia time series, cross‑sectional factor scores, and factor exposures—so that CIOs and PMs can integrate factor diagnostics into a day‑to‑day workflow.

Factor Portfolios: Institutional Next Step

In the remainder of this article, we will focus on the next logical step towards our goal of enabling practical deployment of our crypto factor model through executable portfolio constructions that provide targeted factor exposure; specifically, by presenting research-based portfolio implementations that serve as scalable gauges of the CF Factor Data Series within a digital asset context.

Beginning with the Growth and Value factors, we will demonstrate how long‑only deployment of factor portfolios, derived from our factor research, translates into concrete new facilities and tools that enable investors to better understand and manage digital asset portfolios.

Why Long-Only?

In factor investing, long–short factor portfolios are a canonical tool because they isolate a risk premium in a controlled way. In digital assets, this diagnostic layer is particularly important. It allows investors to attribute P&L to systematic drivers rather than token‑specific narratives, and to observe how premia behave through recoveries, drawdowns, and risk‑on phases.

However, these long–short constructions are not how most institutions express factor views in practice. Constraints around shorting, leverage, borrow availability, derivatives funding, and venue risk mean that, for the majority of allocator mandates, factor exposure is ultimately implemented through long-only portfolios.

Long-only is the default institutional pathway because it is easier to custody, report, scale, and oversee. In practice, long‑only factor exposure is typically implemented via ranking‑based allocations that hold more of what scores highly, benchmark‑relative tilts that preserve portfolio structure while introducing measured factor bias, or overlays on top of strategic core holdings. The key point is that implementation is defined as much by portfolio engineering choices as by the factor signal itself.

In the next section, we will lay out the key structure and reasoning underpinning what we have determined to be the most salient design choices for implementation of long-only factor-based portfolios, together with detailed descriptions of long-only investment variants provided as examples of this deployment.

From Factor Scores to Portfolio

Firstly, we should note that, in essence, long‑only factor portfolios are widely understood to be shaped by specific design levers: universe definition, signal preparation, constituent selection and weighting method, and rebalance frequency. These levers control concentration, turnover, capacity, and benchmark alignment.

CF Large Cap Universe

To ensure that our results are replicable and grounded in a liquid, capacity-aware investment universe, we define two investable universes. The first is what we will refer to as ‘CF Large Cap’. It is based on the flagship index of CF Benchmarks’ CF Capitalization index series, The CF Large Cap Index.

The CF Large Cap universe represents assets capturing approximately 95% of total crypto market capitalization, supporting scalability and replicability.

GLS-Compliant Universe

The second universe is more restrictive. We have termed this the ‘GLS‑Compliant’ universe, as it focuses on assets with qualifying futures contracts trading on regulated venues – Designated Contract Markets (DCMs) like those operated by CME Group or Coinbase – over a trailing window, reflecting stricter product‑level constraints.

This GLS-Compliant framework is based on the Generic Listing Standards (GLS) for Commodity-Based Trust Shares rules that were approved by the U.S. Securities and Exchange Commission (SEC) in September 2025. These allow national securities exchanges (such as NYSE Arca, Nasdaq, and Cboe BZX) to list and trade specific, qualifying commodity-based exchange-traded products (ETPs), including those holding crypto assets, without requiring individual, case-by-case approval from the SEC.

Signal Matters

Underlying these careful universe determinations is the realization that signal preparation matters. Factor scores derived from on‑chain descriptors can be volatile, so our research has explored score smoothing via rolling medians over different windows. Weighting methods then map the score into a portfolio: a positive‑screened, market‑cap weighted approach expresses the signal most aggressively. Then, score‑weighted portfolios distribute exposure more evenly; and benchmark‑tilted portfolios preserve benchmark shape while adding controlled factor bias.

Introducing Factor Portfolios: Long-Only Growth and Value Implementation

With that implementation lens in place, the next step is to package the Growth and Value signals in a transparent, rules-based long-only format that investors can easily implement.

As such, this format is designed to provide institutional-grade long-only exposure to specific crypto risk premia, using the Growth and Value factors defined within the CF Factor Intelligence suite and CF Benchmarks’ published factor research. The methodologies emphasize replicability and governance: construction choices are made explicit, and portfolio outcomes are managed through the same practical levers discussed above—universe definition, score smoothing, constituent selection and weighting, caps, and rebalancing—so investors can understand and manage the resulting exposures through time.

Within this framework, Value seeks to identify protocols that appear inexpensive relative to their economic scale, using combinations such as fees relative to TVL and daily active users relative to market capitalization. Growth seeks to identify protocols with accelerating network adoption and activity, using measures such as fee growth and active‑user growth over a defined horizon.

Long-Only Variants

In order to provide concrete implementation examples for portfolio managers, we have devised three scenarios based on two long-only institutional investment variants.

While intentionally streamlined, we have striven to make these variants as representative as possible of the scenarios, challenges and resultant decision-making process portfolio managers will face when attempting to implement factor-based frameworks for long-only investing.

Each variant uses the same underlying factor scores, but the variants differ materially in how ‘signals’ (from the scores) are translated into portfolio constituents and weights, and how implementation constraints are managed.

We will examine the variants below.

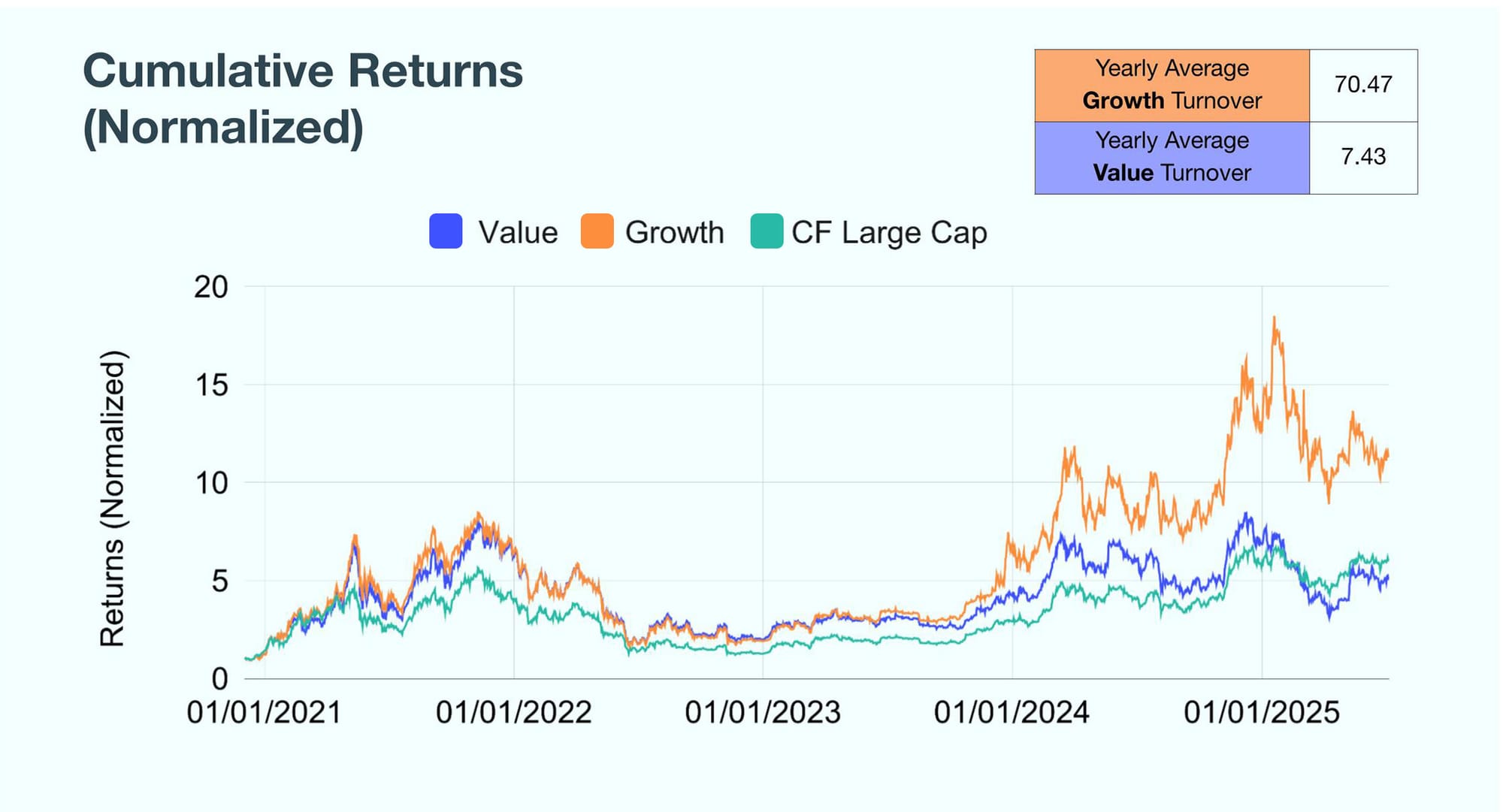

Variant 1: High‑Conviction Screen

This design starts from the CF Large Cap universe and applies a strict positive screen: only assets with positive factor scores are eligible. Constituents are then weighted by market capitalization. Score smoothing over a longer window (e.g., a 180‑day rolling median) and annual reconstitution are used to limit churn, though constituent turnover can remain significant—particularly for Growth—because the signal is expressed explicitly through inclusion/exclusion. The result is a relatively concentrated portfolio profile with strong active expression relative to the benchmark.

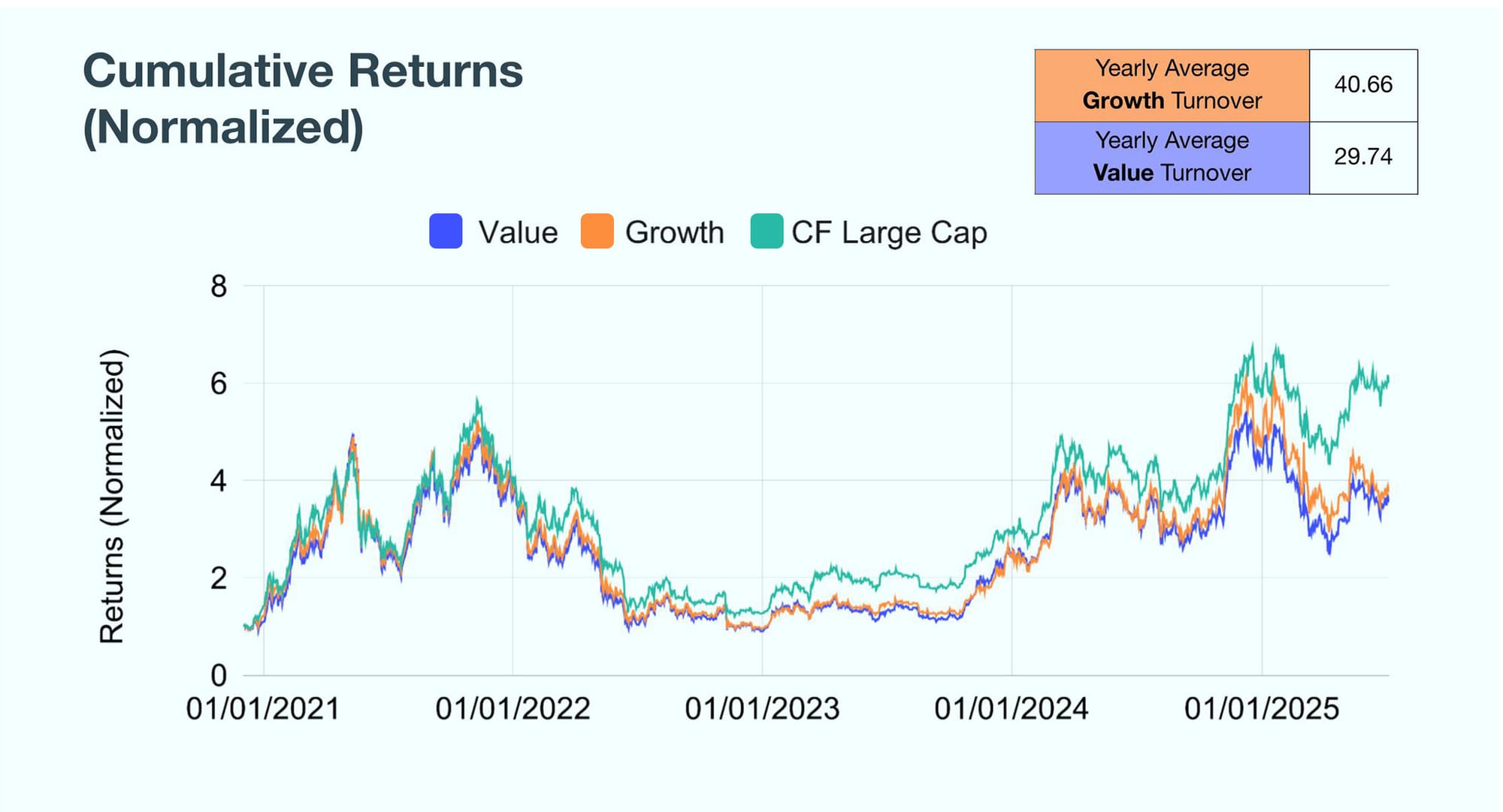

Variant 2: GLS‑Compliant Universe

This design is motivated by deployability constraints and smoother exposure distribution. It uses the GLS‑compliant universe and assigns weights based on factor scores (higher scores receive higher weights and vice versa). A concentration cap (e.g., 25%) is applied across eligible assets to reduce headline concentration risk. In our testing, this approach preserved benchmark‑outperformance characteristics while producing a more balanced representation of the factor signal and lower portfolio turnover relative to screened approaches. The principal trade‑off is reduced breadth in the tighter universe, which can increase volatility.

Variant 3: Core Overlay

This design starts with benchmark market‑cap weights and introduces measured factor tilts based on scores, preserving the benchmark’s overall structure while adding controlled exposure. Score smoothing over a moderate window (e.g., 30‑day rolling median) and explicit caps (e.g.,1/3%) help manage concentration and keep turnover low. The typical profile will be familiar to CIOs and PMs: lower active share, lower churn, and a more muted expression of the factor signal. The expected trade‑off is that benchmark outperformance tends to be more cyclical and less extreme than more active constructions.

A note on interpretation

All charts above are for illustrative purposes and reflect back‑tested portfolio research using the stated methodologies. Back‑tested results are hypothetical and do not represent actual trading. There can be material differences between back‑tested and realized performance. Past performance does not guarantee future results.

Key Takeaways

Hence, CF Factor Intelligence supports two linked institutional workflows. The first is portfolio attribution and risk premia diagnostics, helping investors explain performance, monitor risk exposure, and understand behavior across regimes. The second is replicable portfolio construction: factor scores can be mapped into long‑only implementations that match mandate constraints, whether as high‑conviction satellites, institutionally balanced sleeves, or benchmark‑tilted overlays.

The central design principle across both workflows is governance. Crypto factor signals—particularly those derived from on‑chain descriptors—can be noisy and regime‑dependent. A robust approach therefore makes construction choices explicit, monitors turnover and concentration, and focuses on implementability rather than optimization with hindsight.

Conclusion

In summary, the work described here is about moving crypto factors from an abstract research concept into an institutional workflow. The CF Factor Intelligence framework provides a means of operationalizing those insights into daily premia, scores, and exposures, and of expressing selected premia through long-only portfolio constructions.

For CIOs and PMs, the practical opportunity is to progress from ‘owning crypto’ to intentionally managing systematic exposures. At the implementation level, factor exposure—such as Growth or Value—can be expressed through a range of long-only portfolio constructions, tailored to mandate constraints, including High-Conviction Screens, GLS-compliant balanced sleeves, or benchmark-tilted Core Overlays.

For CIOs and PMs, the practical opportunity is to progress from ‘owning crypto’ to intentionally managing systematic exposures. A combination of factor styles can then be chosen that matches mandate constraints: either a High-Conviction Screen, a GLS-Compliant balanced sleeve, or a benchmark-tilted Core Overlay, among others.

Overall, the foregoing process demonstrates that, factors such as Growth and Value, for example, as defined by CF Benchmarks within the context of digital asset investing, can be treated as verified investable building blocks. Prudent investment managers can evaluate them alongside existing holdings, assess their regime behavior and portfolio role, and—where appropriate—pilot allocations or overlays involving them with a clear governance and reporting framework.

In short, our CF Factor Data product is ready for deployment within institutional crypto.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.