Jul 09, 2026

2026 Mid-Year Market Outlook

Executive Summary

Since our prior edition, the Iran conflict and fragile ceasefire have reshaped the macro backdrop across energy, inflation, and Fed policy. Growth held up in the first quarter, supported by AI investment and defense spending, but the expansion is narrowing as hiring freezes, real-wage pressure, and private-credit risk weigh on the second half. We expect the Fed to remain on hold through most of 2026, with the inflation spike fading as energy reverses and a first cut likely around the turn of the year. A renewed closure of the Strait of Hormuz remains the key risk, reviving inflation and rate-hike pressure.

Regulatory progress provides an important counterweight. The CLARITY Act could establish a federal market-structure regime, clarify SEC and CFTC jurisdiction, and improve the operating environment for layer-1 networks and DeFi, though full implementation may extend into 2028–2029. Bitcoin’s underperformance has also created the conditions for an advisor-led rebalancing bid, as model portfolios approach lower allocation bands and potential support emerges in the $50,000–$60,000 range. Beyond Bitcoin, leadership is shifting toward productive onchain activity. Agentic finance is moving from infrastructure to distribution, tokenized equities are gaining share on Solana, and capital is beginning to favor protocols whose tokens capture verifiable revenue. Across these themes, dispersion, not broad beta, should define opportunities over the next twelve months.

Market Recap: A Ceasefire Rally, a Hawkish Handoff, and a Deepening Drawdown

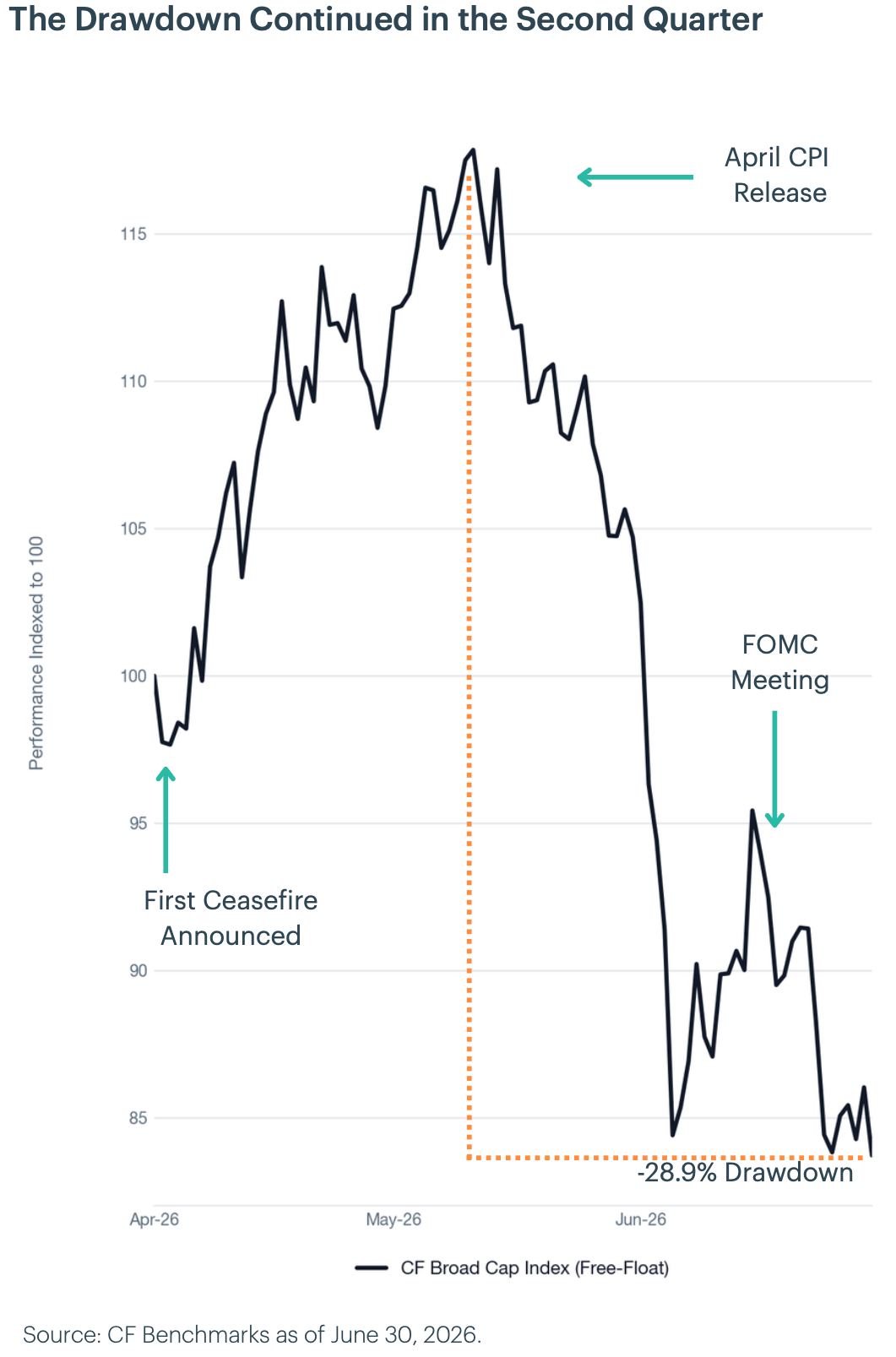

A U.S.-brokered Iran ceasefire, reached mid-April after the February 28 outbreak, triggered a coordinated rally across risk assets, though the Strait of Hormuz remained largely closed. The Federal Reserve held rates steady on April 29 in Chair Jerome Powell's final FOMC meeting, an 8-to-4 dissent, the most fractured vote since 1992, while the Senate Banking Committee advanced Kevin Warsh's nomination to succeed him on a 13-to-11 party-line vote. Bitcoin (BTC) posted its best monthly gain in a year as spot Bitcoin ETFs registered their largest inflows of 2026, and every CF Benchmarks index closed higher, led by the CF Ultra Cap 5 Index's 11.9% gain.

The rebound proved short-lived. April CPI, released May 12, rose 3.8% year over year, the highest since May 2023, as the lingering Iran conflict oil shock fed into energy and shelter costs. FOMC minutes from the April meeting showed officials ready to raise rates if inflation stayed elevated. The Senate confirmed Kevin Warsh as the next Fed chair on May 13 by a vote of 54 to 45, even as a 60-day U.S.-Iran ceasefire framework pulled crude down almost 19%. Spot Bitcoin ETFs recorded their largest monthly outflow of 2026, roughly 2.4 billion dollars, and May reversed April's rebound in full, with every CF Benchmarks index posting a negative return and year-to-date drawdowns back in the 20% to 29% range.

June brought a hawkish handoff and a fragile peace. May CPI, released mid-month, rose 4.2% year over year, its highest in three years. At his first meeting as chair on June 17, Kevin Warsh's FOMC held the policy rate at 3.50% to 3.75% on a unanimous 12-to-0 vote, but updated projections erased the prior 2026 cut and flipped toward a hike, pushing easing into 2027. U.S. and Iranian officials signed the Islamabad Memorandum on June 17 to wind down the conflict, though follow-on talks stalled, leaving crude volatile. Digital assets absorbed the quarter's sharpest hawkish repricing: every CF Benchmarks index posted a steep monthly loss, and year-to-date drawdowns widened to a 34% to 43% range by quarter end.

Measuring Growth: Growth Held the Oil Shock, but Narrows From Here

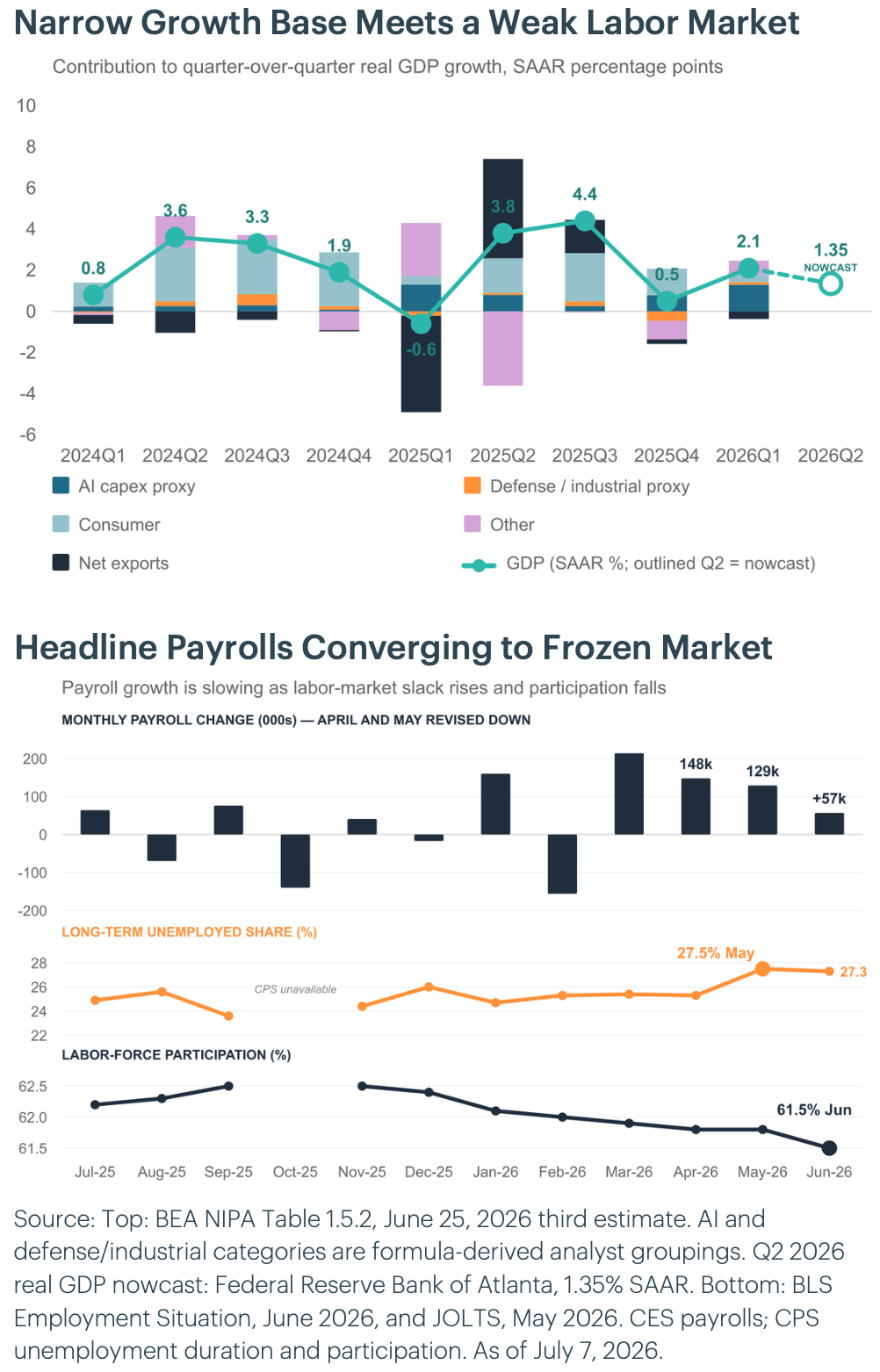

A sustained closure of the Strait of Hormuz, the conduit for a fifth of global oil, would normally raise recession risk sharply. So far, the opposite has happened: Q1 grew 2.1% (BEA), roughly in line with a 2% trend, though the Atlanta Fed nowcast has Q2 near 1.35%. Two demand engines did the work. The first is AI moving from capex to revenue, with the largest platforms posting triple-digit AI run-rate growth and two-thirds of industries now reporting meaningful adoption. The second is a defense supercycle, with Washington proposing a $1.5 trillion 2027 budget near 5% of GDP. The key is composition: that impulse is capital- and procurement-heavy rather than wage-led, so it lifts output without the labor-income acceleration that would force the Fed's hand, and it runs below an AI-lifted potential, which is why solid growth is not inflationary. We see the second half slipping below trend as the narrowing and the labor freeze bite.

The June jobs report confirmed what the internals had signaled. Payrolls rose just 57,000, well below the roughly 115,000 consensus, and revisions cut May to 129,000 and April to 148,000, some 74,000 fewer than first reported. Unemployment ticked down to 4.2%, but for the wrong reason: labor-force participation fell to 61.5%, the lowest since 2021. May's 172,000 was a false dawn; the headline has caught down to a low-hire, low-fire market, where the long-term unemployed share sits at 27.5%, a cycle high, and wages at 3.4% lag prices. The freeze is increasingly an AI story: firms frame hiring through 'operational efficiency,' with work that once took 20 engineers handled by one directing ten agents and a majority of new code AI-generated at some firms. This is the transmission channel we watch: a frozen market can hold the jobless rate flat, then move quickly once private-credit stress reaches small employers.

Portfolio Perspective: Our prior growth outlook is tracking well, we said the first quarter would be the high-water mark, and so far it is, with Q1 at 2.1% giving way to a Q2 nowcast near 1% as the AI-and-defense cushion fades. The expansion is narrowing and AI is hollowing out hiring even as it lifts output, a K-shaped economy. For risk assets that makes dispersion, not direction, the opportunity: broad beta now owns the softening middle as much as the leaders, so selection is everything. We would hold the cycle's AI-infrastructure and defense leaders as tokenized equities through xStocks, and the wider shift through tokenized real-world assets and AI-linked tokens.

Measuring Inflation: Core May Be Overstated: An AI-Era Mismeasurement

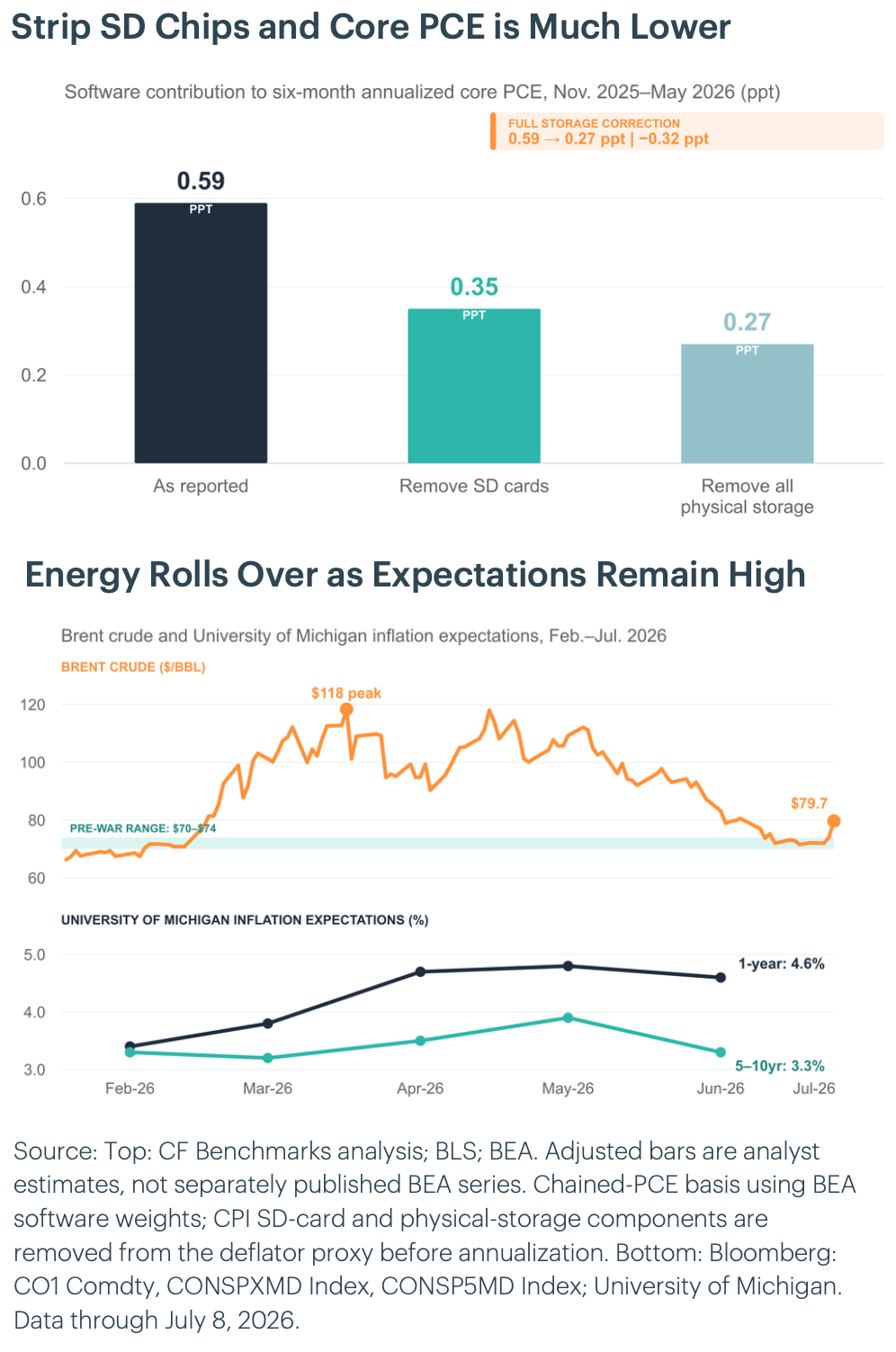

Headline CPI rose to a three-year high of 4.2% year over year in May, and the market had repriced toward a hike, though the soft June jobs report has begun to pare those bets. We think both the market and the consensus are anchoring on an overstated core, and the distortion is mechanical. To deflate PCE software the BEA borrows a CPI index that also captures physical storage, SD cards and hard drives, whose prices surged with the memory-chip shortage, so a goods-price spike reads as software inflation. Because software carries a 1.2% weight in core PCE against just 0.03% in the CPI, the effect is outsized: stripping storage out lowers six-month annualized core PCE by about 0.3 point, and that is before any credit for fast-improving AI software quality. Corrected, the Fed's preferred gauge sits much closer to target than the headline implies, the heart of our contrarian call.

The cyclical case reinforces the structural one. Energy drove more than 60% of May's monthly CPI gain, and that impulse is already reversing: on our fragile-ceasefire, open-Hormuz base case, Brent has round-tripped to pre-war levels near $70 to $74, which mechanically pulls headline inflation lower through the second half. Pass-through is weak. Most firms cannot push higher energy and materials costs onto customers, and with nominal wages near 3.4% running below the 4.2% headline, real wages are negative, shutting the second-round wage channel. Long-run expectations are drifting down, not up, with the University of Michigan's measure easing to 3.3 to 3.4%. The risk is duration: a ceasefire breakdown that re-arms energy, or margins that hold selling prices firm even as input costs stabilize.

Portfolio Perspective: Our call is contrarian: a correctly measured core plus reversing energy points to underlying inflation lower than the market or consensus believes. Market-based measures have only partly caught up: near-term breakevens and inflation swaps still embed much of the energy spike, which we read as mispriced to the upside, while longer-run measures stay anchored; that gap should close as the prints roll over. The read-through runs through the dollar and real yields, both elevated on the scare and a lid on the debasement trade. If inflation surprises lower and they ease, that lid lifts, and the debasement assets, bitcoin alongside gold, are the cleanest beneficiaries.

Measuring the Fed: A Hold That Resolves Lower

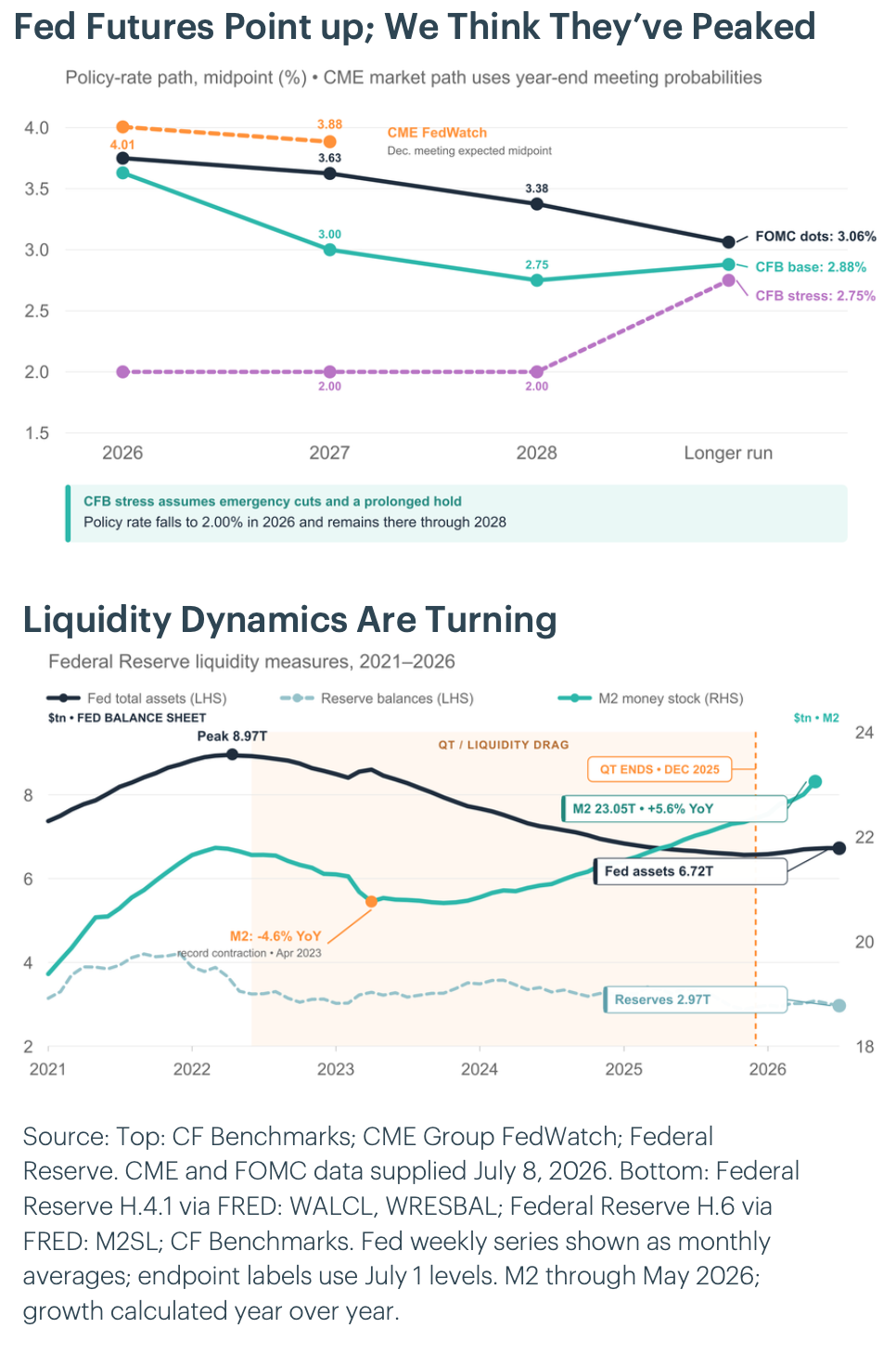

The committee held at 3.50–3.75% in June, a fourth straight hold, then turned hawkish in the projections: the Fed's SEP median dot for end-2026 jumped to 3.80% from 3.40%, with nine of eighteen participants now penciling a hike. We still expect a hold that resolves lower. Headline CPI hit a three-year high of 4.2% year over year in May, but energy drove more than 60% of the monthly gain while core CPI held at 2.9% and shelter cooled to 3.4%, and the shock is already reversing, with Brent back at pre-war levels near $74. Long-run inflation expectations have eased to 3.3%, not the mark of un-anchoring. The Fed can avoid hiking if it reads the spike as pipeline and energy; the hike case builds only if services stick or expectations break higher. The clearest risk is the fragile ceasefire: a breakdown that re-closes Hormuz would re-arm both the oil shock and the dots.

Kevin Warsh, confirmed 54–45 and sworn in as Powell's term as chair ended, paired continuity on rates with a break on process: a 130-word statement, no forward guidance, and task forces to remake the Fed. We read it as deliberate: by signaling hawkishly, he is content to let the bond market carry the tightening, holding the long end elevated rather than moving the policy rate. Through June it worked, with the market pricing the next move as a hike; the soft June jobs report has since begun to pare those odds, an early sign the hold resolves lower, as we expect. On independence, the Court narrowed the premium for agencies generally but preserved a Fed-specific carveout, lowering the immediate tail risk of a White House majority at the Board, especially with Powell holding his governor seat through January 2028. On the balance sheet, QT ended near $6.6 trillion with reserves near $2.9 trillion, and with runoff over and M2 reaccelerating from its 2023 contraction, the liquidity drag has turned into a modest tailwind; longer term Warsh wants a smaller, Treasury-only footprint, while private credit (a 5.7% default rate) remains the channel that would ultimately force the Fed's hand.

Portfolio Perspective: Our prior dovish call was early, but we are more convinced the cycle has peaked. Base case (around 55%): an extended hold that resolves lower, no hike in 2026 and a first cut around the turn of the year, below a Fed median that still implies a hike, against two roughly symmetric tails, a ceasefire collapse that re-arms the oil shock (around 25%) and a private-credit crack that forces emergency cuts (around 20%). For digital assets, the peaked but still-high front end is the pivot: tokenized Treasury and money-market RWAs, the largest on-chain segment, are the cash leg paying that rate today, and the first cut is the catalyst to rotate from tokenized cash out the risk curve into crypto beta. With the energy tail live and the distribution two-sided, we would own that convexity through regulated options on bitcoin and structured payoffs.

Measuring the Geopolitical Landscape: The Realignment Outlasts the Ceasefire

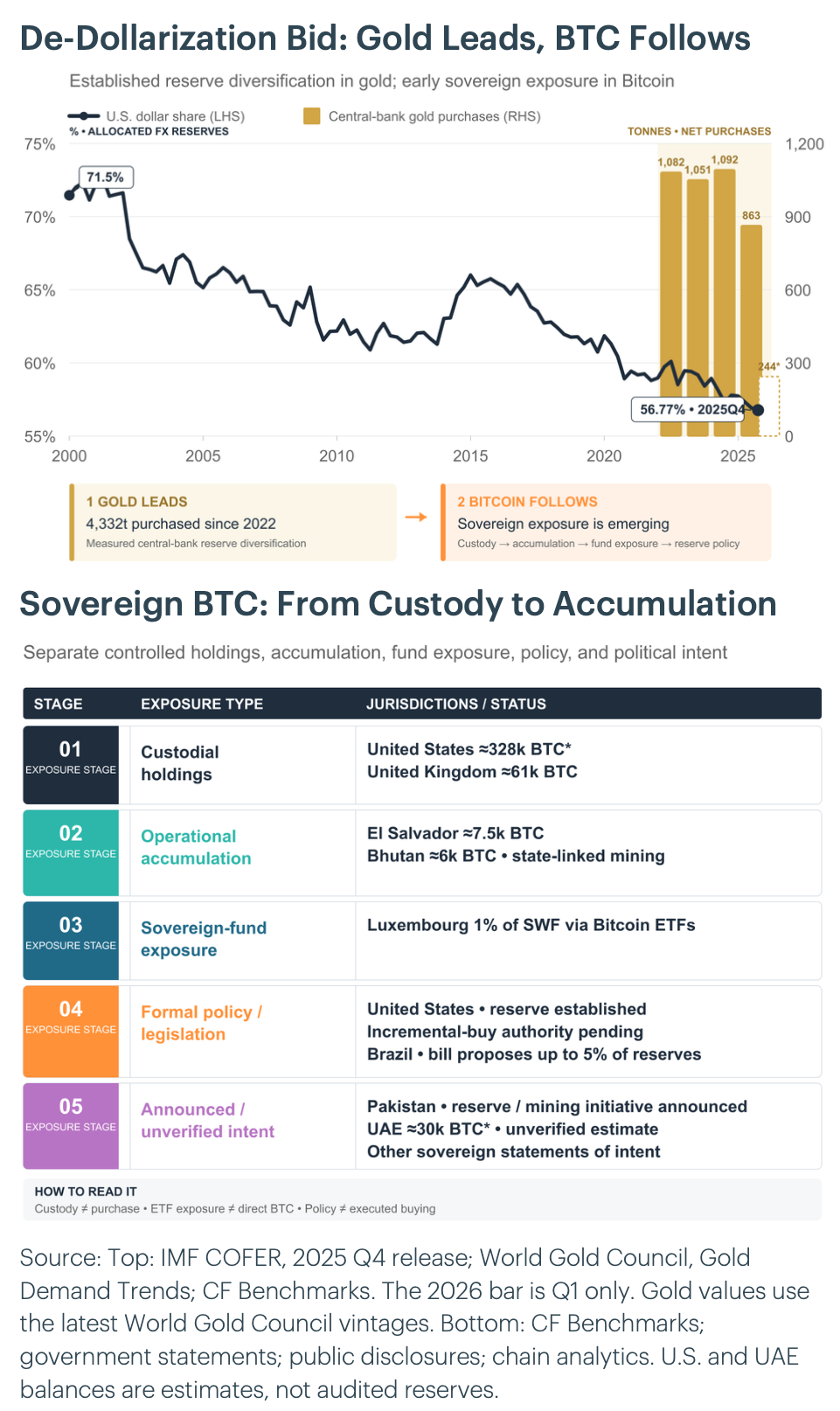

The Iran ceasefire is holding but was strained again this month, a reminder of its fragility even as oil has settled back near pre-war levels and Strait of Hormuz traffic slowly recovers. The war's lasting mark, though, is structural rather than cyclical: it has accelerated a realignment in how states hold reserves. The lesson sovereigns drew from the 2022 freeze of roughly $300 billion of Russian reserves, that dollar holdings can be weaponized, has hardened into policy. Central banks are buying gold at a record pace, with a record 45% of reserve managers expecting to add gold, up from 29% two years ago, and more than 4,000 tonnes purchased since 2022, while the dollar's share of global reserves has slipped to about 56.8%, the lowest since 1994. Add a defense supercycle and a fragmenting trade system, and the through-line is a world deliberately reducing its reliance on any single sovereign's money. That is the lens we now apply to digital assets: the same impulse driving record gold demand is beginning to reach bitcoin.

Bitcoin is the digitally native complement to gold in that trade, hard to confiscate when self-custodied, and the sovereign bid is emerging, though still uneven. Around 23 governments are estimated to hold bitcoin and more than 40 have signaled intent, but the demand is not one thing. Most large state holdings are seized or custodial rather than bought, led by the United States at roughly 328,000 coins and the United Kingdom, while a smaller group, El Salvador and Bhutan, is actively accumulating. A policy tier is now forming: the proposed BITCOIN Act could see the US Treasury buy as early as the fourth quarter, and Brazil is advancing a bill targeting 5% of reserves, with exploratory intent beyond, from Pakistan to other signals. The significance, if that tier funds, is structural: sovereign buyers are price-insensitive and sticky, and against a fixed 21-million supply that issues only about 450 new coins a day, even a marginal slice of official reserves is large relative to available float, removing it in a way the price-sensitive and fast-money flows behind bitcoin's roughly 30% drawdown this year do not.

Portfolio Perspective: The immediate risk cuts against us. This month's renewed escalation is a reminder that a ceasefire break which shuts the Strait of Hormuz for an extended period is the core risk to our outlook: it would re-arm the energy shock, push inflation expectations, rates, and hike probabilities higher, and dampen risk sentiment, a near-term headwind for crypto. We hedge that tail directly, holding a long-crude position through regulated futures that pays off in exactly the scenario that would hurt the rest of the book. Look through it, though, and the through-line is unchanged: a fragmenting world in which reserve dollars can be frozen is a structural catalyst for non-sovereign stores of value, bitcoin foremost, the same force behind record central-bank gold buying. We would hold both: bitcoin, hard to confiscate when self-custodied, and tokenized gold, a convenient way to hold and control non-sovereign gold on-chain, off any single government's balance sheet. The reserve bid is gradual and policy-dependent, but its direction is set.

Measuring the Regulatory Environment: CLARITY Act Would Establish a Federal Market Structure Regime for Digital Assets

The CLARITY Act would deliver legal certainty across three areas central to market structure: regulatory jurisdiction, state preemption, and consumer protection. The bill would classify most digital assets as commodities, drawing a clear line between SEC and CFTC authority and creating the definition of a digital commodity that developers and service providers have lacked. A federal intermediary registration framework would establish unified categories for exchanges, brokers, and dealers, replacing the current fifty-state patchwork with a single compliance floor. Consumer protection provisions, spanning asset segregation, disclosure standards, and conduct rules, would set a uniform baseline the existing framework fails to provide. The core architecture has stabilized; remaining substantive work involves reconciling the Senate Banking and Agriculture committee texts, finalizing transition provisions for existing registrants, and settling protections for developers building on decentralized protocols. Gray areas would persist for certain products as they come online, but the treatment of most crypto assets would become materially clearer.

We are expecting new committee text released in July, with Senate floor consideration to follow if the process holds. The principal risk to that timeline is political, not substantive: an ethics provision tied to the administration is the last outstanding issue, with White House agreement not yet secured as of early July. Failing that agreement, the Senate could advance the bill independently and press the President to accept it. Post-enactment, core provisions come online within 18 months, while rulemaking-dependent measures track final rule publication. Given agency bandwidth and comment periods, our realistic window for full operability is 2028 to 2029, with non-rulemaking provisions arriving sooner.

Portfolio Perspective: Within the digital asset landscape, the clearest beneficiaries are layer-1 protocols and DeFi tokens. Legal certainty around token classification gives developers the confidence to build and launch onshore, directing activity toward established layer-1s such as Ethereum and Solana. DeFi tokens stand to re-rate as litigation overhang lifts and on-chain volumes migrate back to US-accessible venues.

Measuring Bitcoin's Relative Value: The Advisor Bid for Bitcoin

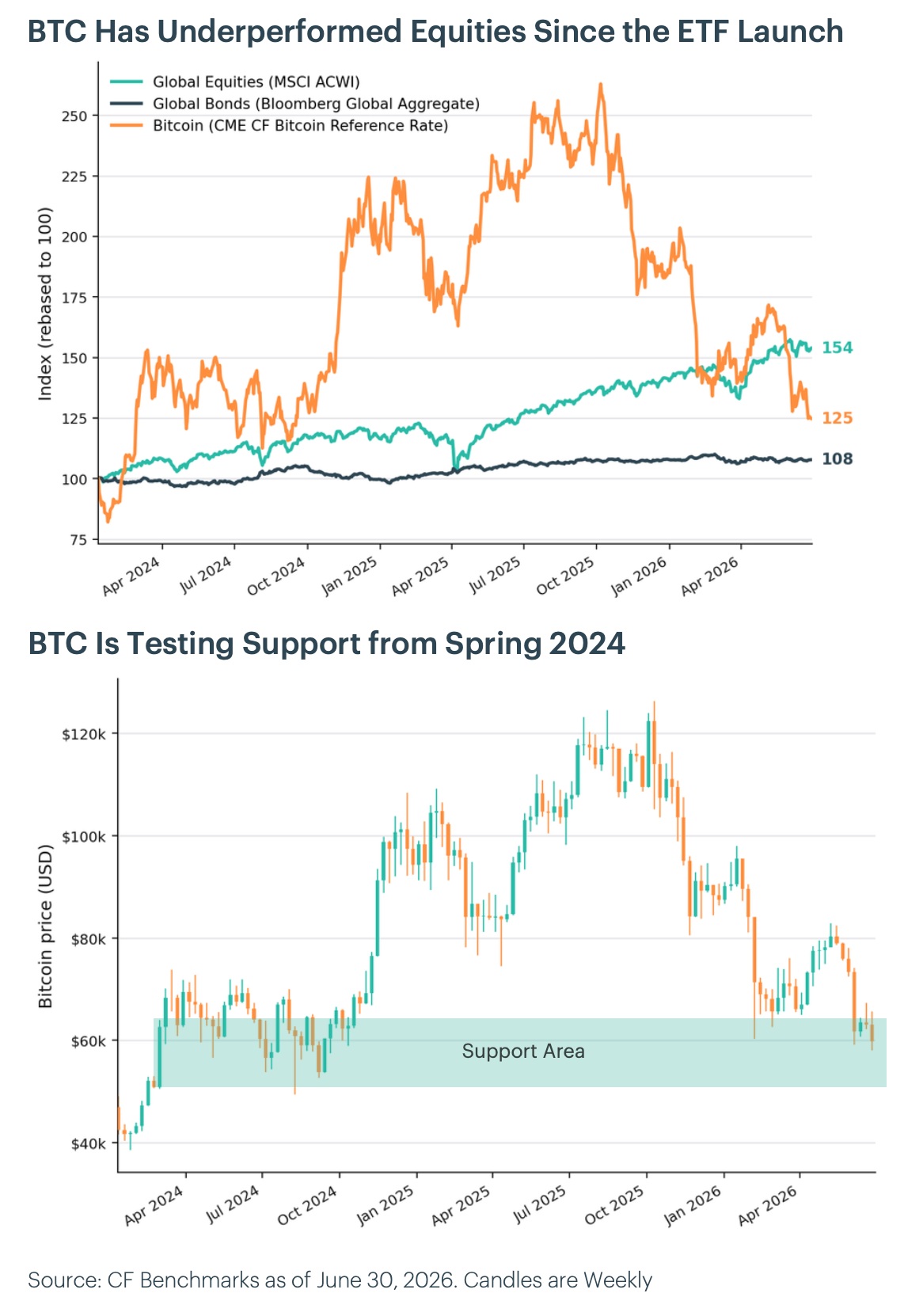

Our view is that the advisory channel should begin converting Bitcoin’s underperformance into structural demand as model-portfolio rebalancing windows arrive. The wider the gap between equity strength and Bitcoin weakness grows, the larger that potential demand becomes. As of June 30, 2026, Bitcoin traded near $59,300 on the CME CF Bitcoin Reference Rate, roughly 53% below its October 2025 high near $125,000. Rebased to January 2024, global equities now sit at 154 and global bonds at 108, while Bitcoin has fallen back to 125, ceding to equities the lead it held through 2025. That handoff creates the setup for the thesis.

The mechanism is rebalancing discipline, not sentiment. Bitcoin typically sits in model portfolios at a strategic 1% to 3% weight, reallocated on a quarterly or threshold-triggered basis. Consider an advisor who placed a client at 2% Bitcoin alongside 59% global equities and 39% bonds. The entry point determines where the next bid may sit. A January 2025 allocation has seen Bitcoin fall 37% against a 32% equity gain, drifting the sleeve to roughly 1.04% and putting the 1% lower band within 4% of today’s price, near $57,000. A March 2025 entry drifts to 1.10%, with the 1% trigger near $53,800. A July 2025 entry, struck closer to the cycle high, has already breached the 1% band at the current price. The 1.5% band is breached in all three cases, and restoring the full 2% weight would require buying close to 95% of the remaining position, turning relative weakness into a countercyclical purchase.

For allocators, the point is that advisor-held Bitcoin may behave less like tactical risk and more like a rebalanced portfolio sleeve. The current divergence sets up an outsized potential rebalancing flow at the next allocation cycle. The principal risk is behavioral: a prolonged drawdown that breaks advisor discipline would remove the bid precisely when it is most needed.

Portfolio Perspective: Bitcoin’s underperformance has delayed the advisor bid, but it may also be setting it up. As Bitcoin lags equities, model portfolios with strategic crypto allocations should drift toward their lower bands. Once rebalancing windows open, allocators may need to add exposure back toward target weights. That creates the potential for countercyclical demand into weakness and adds a flow-based support layer around the $50,000 to $60,000 range. The key evidence to watch is spot Bitcoin ETF flow data: sustained net inflows during drawdowns would suggest that advisor-led rebalancing demand is beginning to emerge.

Measuring Agentic Activity: Natural-Language Agents Meet Tokenized Assets and Stablecoin Rails

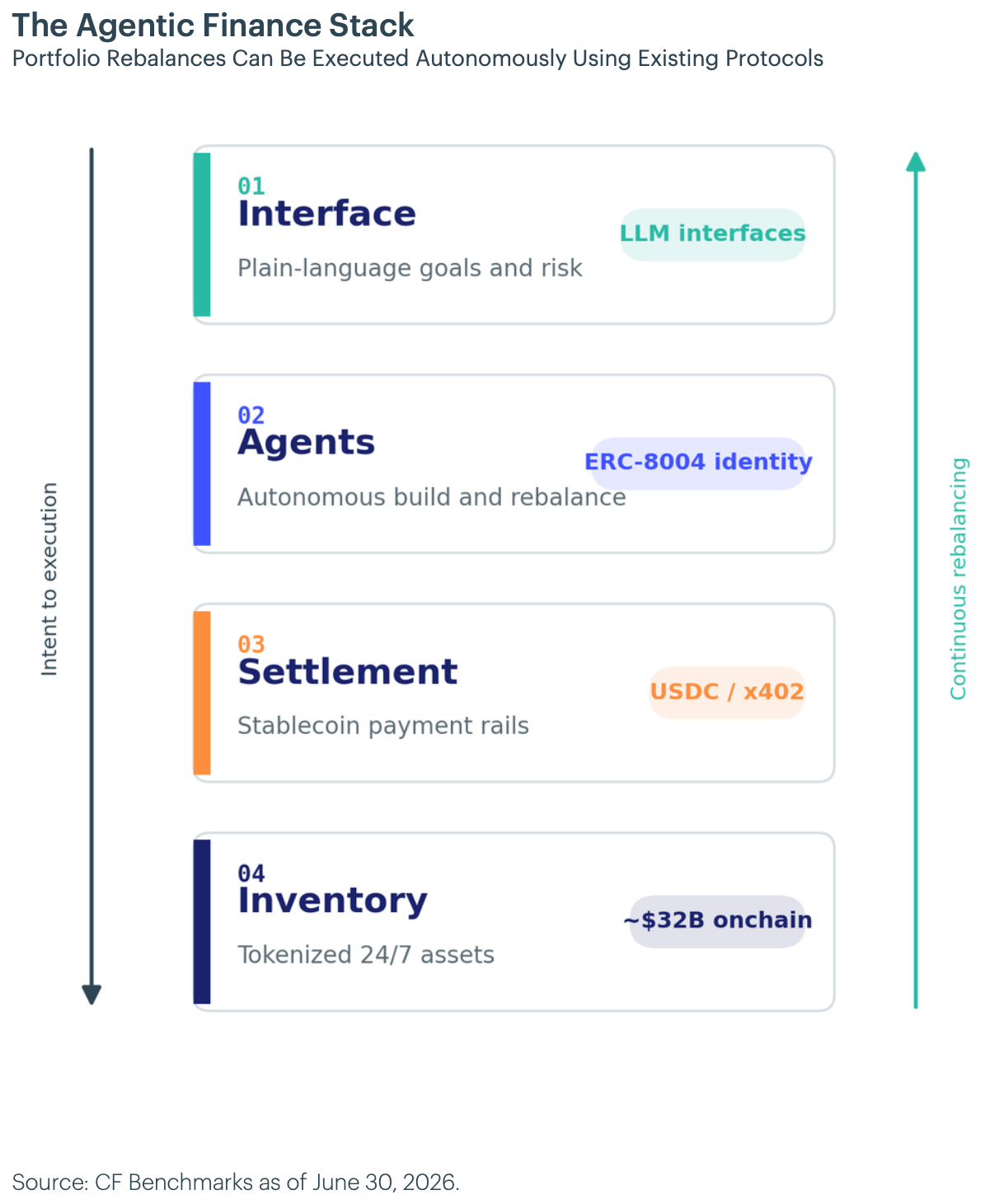

We expect the next twelve months to reward distribution over innovation, as the agentic finance stack matures into shared infrastructure that any platform can assemble rather than build. The four layers shown in the exhibit, running from the natural-language interface through autonomous agents, stablecoin settlement, and tokenized inventory, have matured to the point where a new entrant can assemble a product from existing components rather than build the rails itself. That lowers the cost of participation and, in our view, makes broad platform adoption the base case rather than the accelerated one.

By the end of the period we anticipate that most major brokers and exchanges will have either launched or formally announced an agentic offering. The early movers are already in place: Robinhood opened its platform to customer-supplied agents in May 2026, and Kraken, Coinbase, Binance, and OKX have each shipped developer toolkits. We read these less as isolated launches and more as the first wave of a competitive response that the remaining incumbents will be reluctant to sit out.

The stack also clarifies where the convergence is binding. Agent identity standards such as ERC-8004 and stablecoin payment rails such as x402 are becoming shared infrastructure, which means new entrants compete on interface and execution quality rather than on settlement plumbing. That dynamic favors fast followers.

The signal to watch is whether dollar volume begins to converge toward the activity counts that have already scaled. For allocators, the key takeaway is: value accrues to the rails beneath the applications, the settlement venues, stablecoin issuers, tokenization platforms, and the benchmark layer that agents must rebalance against.

Portfolio Perspective: We expect established layer 1s such as Ethereum and Solana to be the primary beneficiaries of agentic finance growth. Agents will likely settle, hold identity, and rebalance onchain, and that activity concentrates on the platforms with the deepest tokenized inventory, liquidity, and developer adoption. Incumbency, not novelty, captures the demand.

Measuring Tokenization: Tokenized RWAs Are Becoming Solana’s Growth Engine

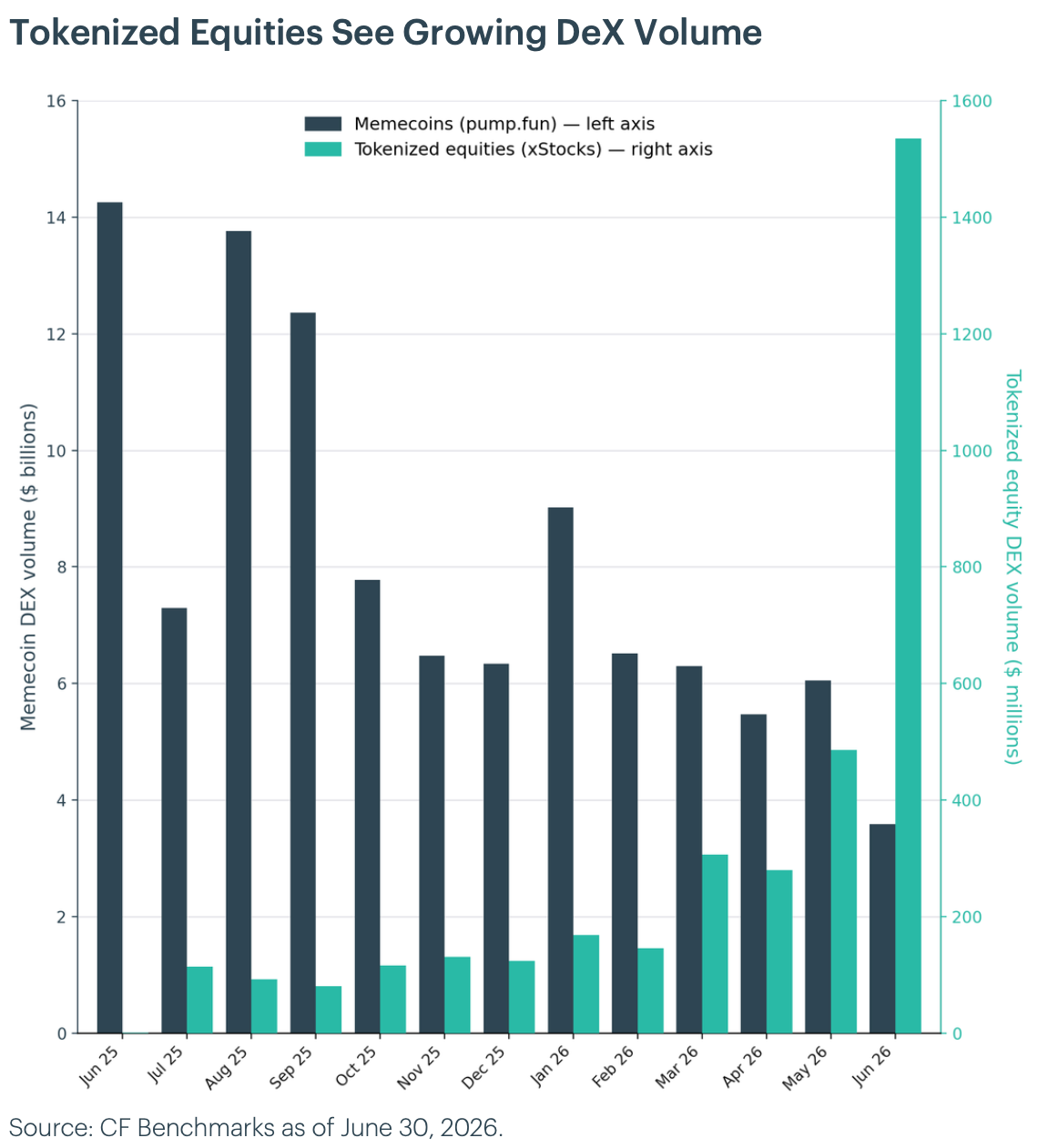

Our view is that tokenized equities will become Solana's primary channel for net-new user acquisition over the next twelve months, displacing the memecoin flow that defined the prior cycle. The evidence sits in the trajectory of xStocks, the Kraken and Backed tokenized-equity product that launched Solana-first on June 30, 2025. Onchain xStocks volume grew from roughly $1.3 million in its partial launch month to $114 million in its first full month, then reached $1.53 billion by June 2026, a step change driven by the SpaceX tokenized-stock debut. Over the same window, pump.fun memecoin volume fell from $14.3 billion to $3.6 billion. The ratio frames it most cleanly: memecoin turnover ran more than 10,000 times xStocks volume at launch and just 2.3 times by June 2026.

The point for allocators is the composition of the buyer, not only the volume line. Memecoin turnover recruited speculative, episodic traders whose engagement evaporated with each cycle. xStocks recruits users seeking equity exposure, a cohort with longer holding periods, larger balances, and a reason to stay onchain beyond a single trade. Holder counts support the read: xStocks holders have grown to nearly 200,000 as of 2026, more than double the 80,000 reported in February, on cumulative transaction volume that has crossed $35 billion, including $12.5 billion traded onchain. Solana captured this flow because sub-cent fees and roughly 400-millisecond finality make onchain equity trading viable where slower, costlier chains could not, and the network continues to route more than 95% of onchain tokenized-equity volume.

The forward case rests on this funnel widening rather than narrowing, and the holder trajectory above is the leading indicator that it already is. Registered onchain-equity structures, such as the Galaxy and Superstate tokenized common stock already live on Solana, extend the addressable base beyond non-US xStocks holders and pull in users who arrive for equities and remain for the broader onchain stack. The principal risk is non-exclusivity, since the same issuers also deploy on Ethereum and EVM networks, so Solana's lead reflects current liquidity rather than contractual lock-in. The signal to watch is sustained holder growth, not a single record month.

Portfolio Perspective: Two beneficiaries stand out. Solana captures the flow, though token demand trails usage. The more direct beneficiaries are tokens in the CF DACS Finance Sector that are native to Solana, where DEX revenue scales as a result of growing tokenized-equity volume.

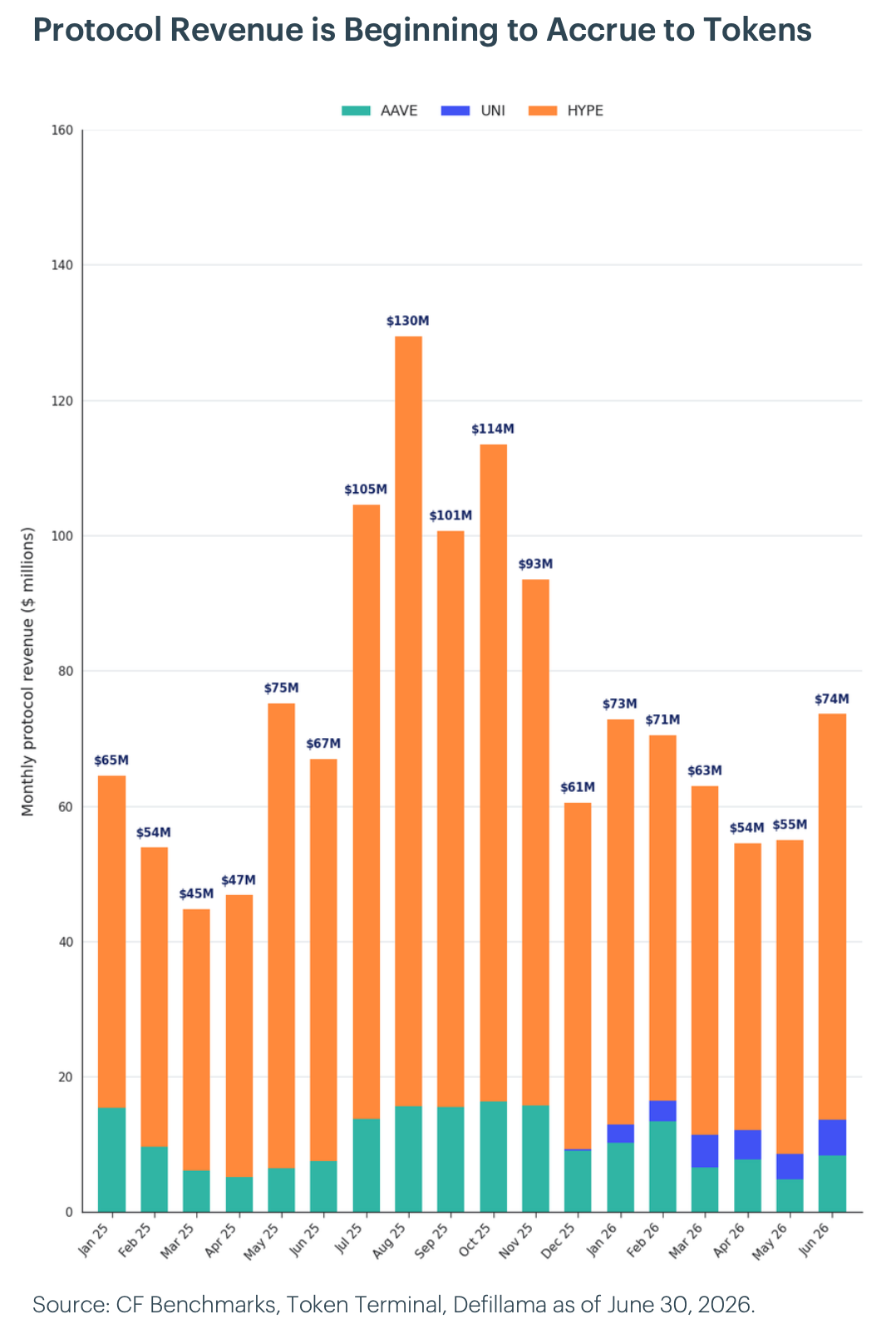

Measuring Protocol Revenue: A Rotation Into Revenue Tokens

Our view is that over the next twelve months, capital within the altcoin complex rotates out of non-cash-generating tokens and into a small group of protocols whose tokens now capture revenue directly. The driver is structural, not technical: three of the industry's largest fee generators activated mechanisms converting protocol revenue into direct token value accrual through late 2025 and the first half of 2026.The designs differ but the outcome is shared. Hyperliquid routes roughly 97 to 99 percent of fees, plus collateral yield, into open market HYPE buybacks. Uniswap's UNIfication proposal switched on the long dormant fee switch and burned 100 million UNI. Aave's Aavenomics 3.0 directs 100 percent of protocol and GHO revenue into automatic buybacks. Each now transmits protocol usage to the token.

The revenue is large and verifiable onchain. Over the trailing twelve months to June 2026, Hyperliquid retained roughly $924 million in protocol revenue, effectively all of it directed to HYPE buybacks, and Aave retained about $138 million. Uniswap's revenue is not yet meaningful over a full year given the December 2025 fee switch activation. That separates the cohort from the speculative long tail and lets these tokens be underwritten on revenue, earnings, and a payout, the way an equity analyst frames a company.

Early price action supports the thesis without confirming it. HYPE, AAVE, and UNI have outperformed a weak altcoin tape, and Grayscale and Standard Chartered have independently flagged the group on cash flow grounds. The principal risk is that revenue proves cyclical: Hyperliquid earnings peaked in the third quarter of 2025 and have since declined, and buybacks remain governance policy rather than a contractual dividend.

For allocators, the takeaway is to differentiate within the altcoin complex on revenue and value accrual mechanism rather than market cap rank. The signal to watch is whether the cohort sustains relative outperformance as fundamentals are repriced.

Portfolio Perspective: We expect that constituents of the CF Broad Cap Index with growing revenues will continue to outperform those without over the next twelve months. Allocators should differentiate within the index on revenue trajectory and value-accrual mechanism, favoring protocols that generate verifiable onchain cash flow and transmit it directly to the token.

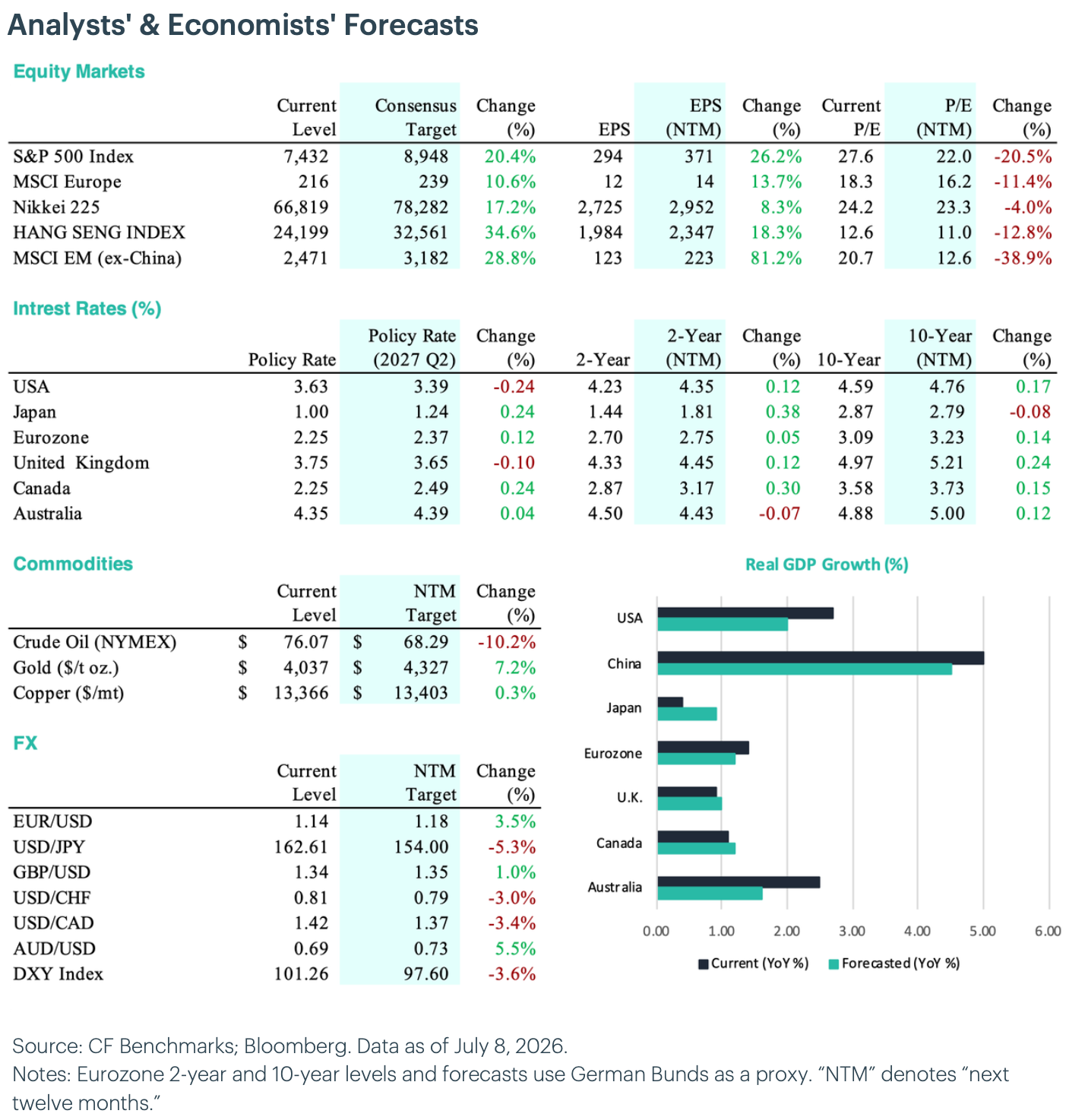

Measuring the Crowd: Consensus Forecasts

Equities: Analysts maintain a broadly positive outlook for equities, with the Hang Seng Index (+34.6%) and emerging markets ex-China (+28.8%) leading major forecasts. European markets (+10.6%) and Japan (+17.2%) are also expected to perform well. U.S. equities are forecast to rise 20.4%, with S&P 500 earnings per share projected to grow by 26.2%. Valuation multiples are expected to contract across major markets, with the S&P 500's P/E falling 20.5%, suggesting price gains are driven entirely by earnings growth rather than multiple expansion.

Interest Rates: Policy rate forecasts show divergent shifts across developed markets, with the U.S. expected at 3.39% by Q2, 2027 (currently 3.63%), the U.K. at 3.65% (from 3.75%), and Australia at 4.39% (from 4.35%). Canada is projected at 2.49% (from 2.25%), while Japan is forecast at 1.24% (from 1.00%). The Eurozone is expected to hold near current levels at 2.37%. Changes in 2- and 10-year yields remain modest, suggesting that global inflation concerns are keeping long rates elevated.

Commodities: Gold is forecast to rise 7.2%, reflecting steady investor demand for real assets amid macro uncertainty. Crude oil is expected to decline sharply (-10.2%), pointing to significantly softer demand expectations. Copper is projected to rise 0.3%, suggesting a modest uptick in industrial activity expectations.

FX: The U.S. dollar is expected to weaken, with the DXY Index down 3.6%. The yen is projected to appreciate sharply (+5.6%) on policy divergence, while gains are also expected in the euro (+3.5%), pound (+1.0%), and Australian dollar (+5.5%). The Swiss franc is forecast to appreciate modestly (+2.5%), while USD/CAD is expected to decline 3.4%.

GDP Growth: Growth forecasts show continued regional divergence. China is expected to lead with growth of 4.5%, while the U.S. is projected at 2.0%. Canada (1.2%) and the Eurozone (1.2%) are forecast to improve modestly, while Australia is expected to moderate to 1.6%. By contrast, Japan (0.9%) and the U.K. (1.0%) are likely to see slower growth.

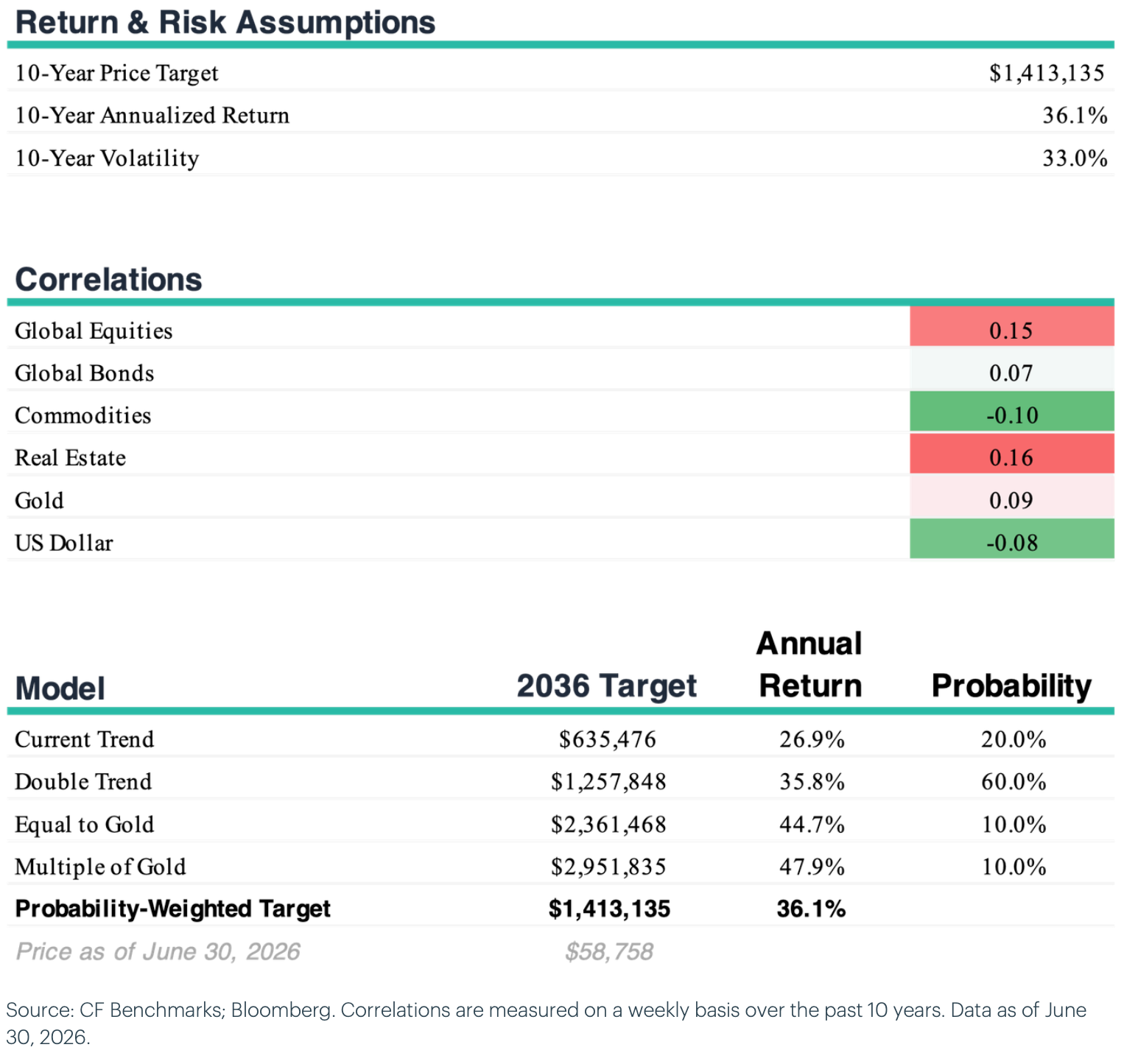

Measuring Return Assumptions: 2026 Bitcoin Capital Market Assumptions

Capital market assumptions provide institutional investors with forward-looking projections of expected returns, volatility, and correlations that guide strategic asset allocation decisions. As Bitcoin matures into an institutional asset class, developing rigorous capital market assumptions becomes essential for allocators evaluating its role within diversified portfolios.

Returns: Our 2026 capital market assumptions project a 10-year annualized return of 36.1% with a probability-weighted 2036 price target of $1,413,135. The price target incorporates probability-weighted scenarios in the store-of-value market, assigning 60% weight to double-trend growth, 20% to current trend continuation, and 10% each to gold parity and gold outperformance.

Volatility: We project long-run volatility using a two-stage decay model that extends the historical compression trend while assuming diminishing marginal declines. The model applies half the historical pace over the next five years (approximately -3.5% annually) reaching 37.0% by 2031, then halves the decay rate (approximately -1.75% annually) to roughly 33.0% by 2036.

Correlations: Our capital market assumptions project Bitcoin's correlations remaining low across asset classes: 0.15 to global equities, 0.07 to global bonds, -0.10 to commodities, 0.16 to real estate, 0.09 to gold, and -0.08 to the US dollar.

To read the our full market outlook report, please click here.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 28 July 2026

Changes to the Token Market Price Benchmarks Series - Market Prices – 28 July 2026

CF Benchmarks

Digital Assets Absorb Hawkish Repricing Ahead of the FOMC

Digital assets traded through a hawkish macro surprise this week but closed mostly higher, with breadth holding across major names and indices. Sector leadership traced to a single regulatory catalyst, not a broad rotation, and implied volatility stayed firmer than realized into the weekend.

Mark Pilipczuk

Factor Friday - July 24, 2026

Beta's four-week grind higher stalled this week as style leadership rotated again: Momentum took the top spot, last week's leader Value fell to the bottom, and Growth stayed July's weakest factor. Size remains the only style factor positive on the year; beta, not style selection, is setting returns.

Mark Pilipczuk

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.