Jun 15, 2026

BVX Compresses as BTC Round-Trips a Three-Year Inflation Shock

Weekly Index Highlights, June 15, 2026

This was a week of loud headlines and a quiet close: despite inflation hitting a three-year high and a U.S. strike on Iranian targets midweek, most assets recovered to finish near where they started. Bitcoin (BTC) added 0.45% and the seven major single assets spanned less than four percentage points. We read it as a round-trip. The macro and geopolitical shocks moved the tape intraday and reversed by the weekly close, helped by the announcement of a U.S.-Iran peace deal late Sunday that will bring an immediate and permanent termination to the conflict and reopen the Strait of Hormuz, with an official signing ceremony set for Friday, June 19, in Switzerland. The prior week's defensive positioning unwound, implied volatility fell back toward a rising realized, and the only real differentiation came from inside the market: a decentralized-AI bid that made Infrastructure the week's widest sub-category.

Market Performance Update

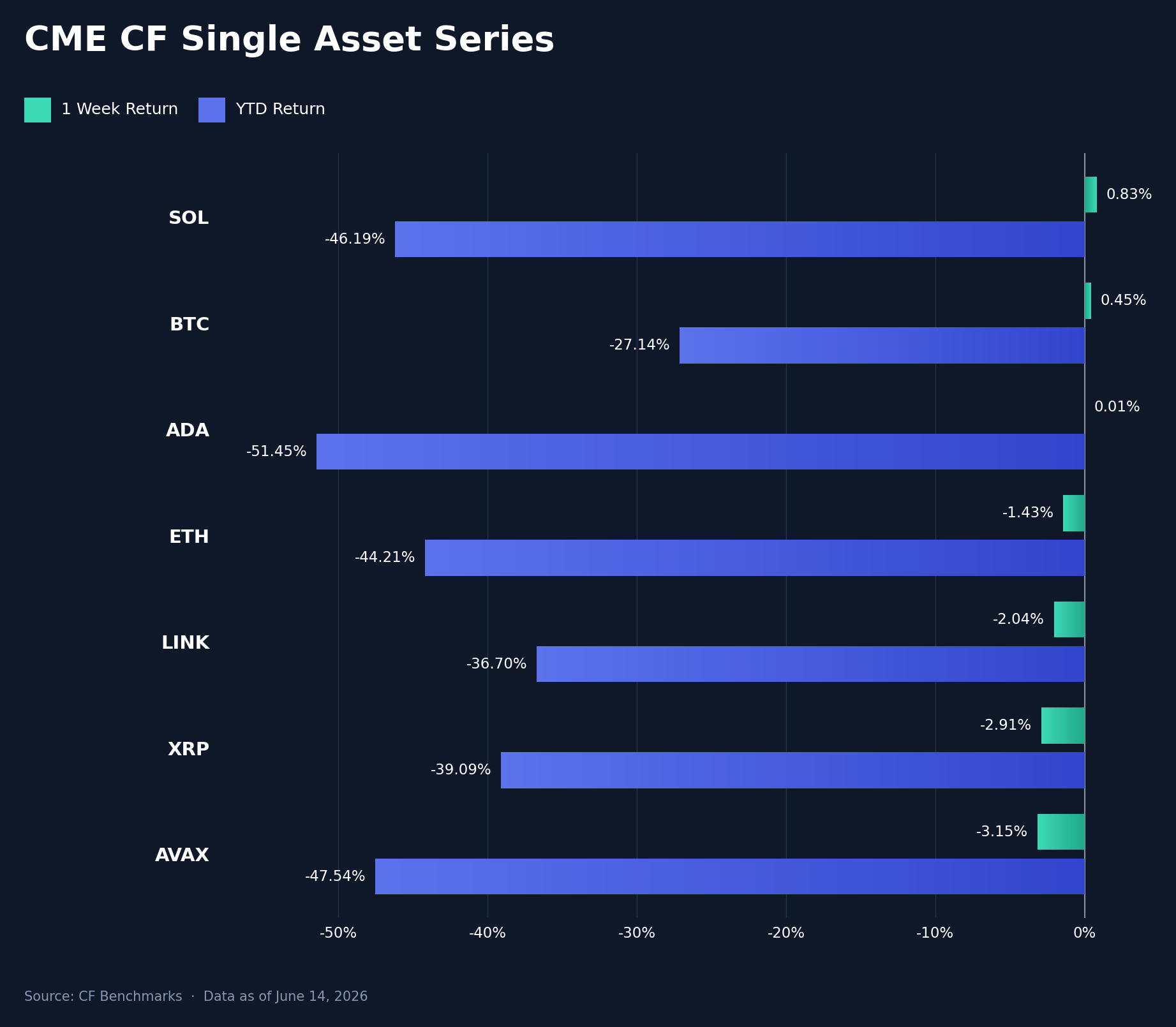

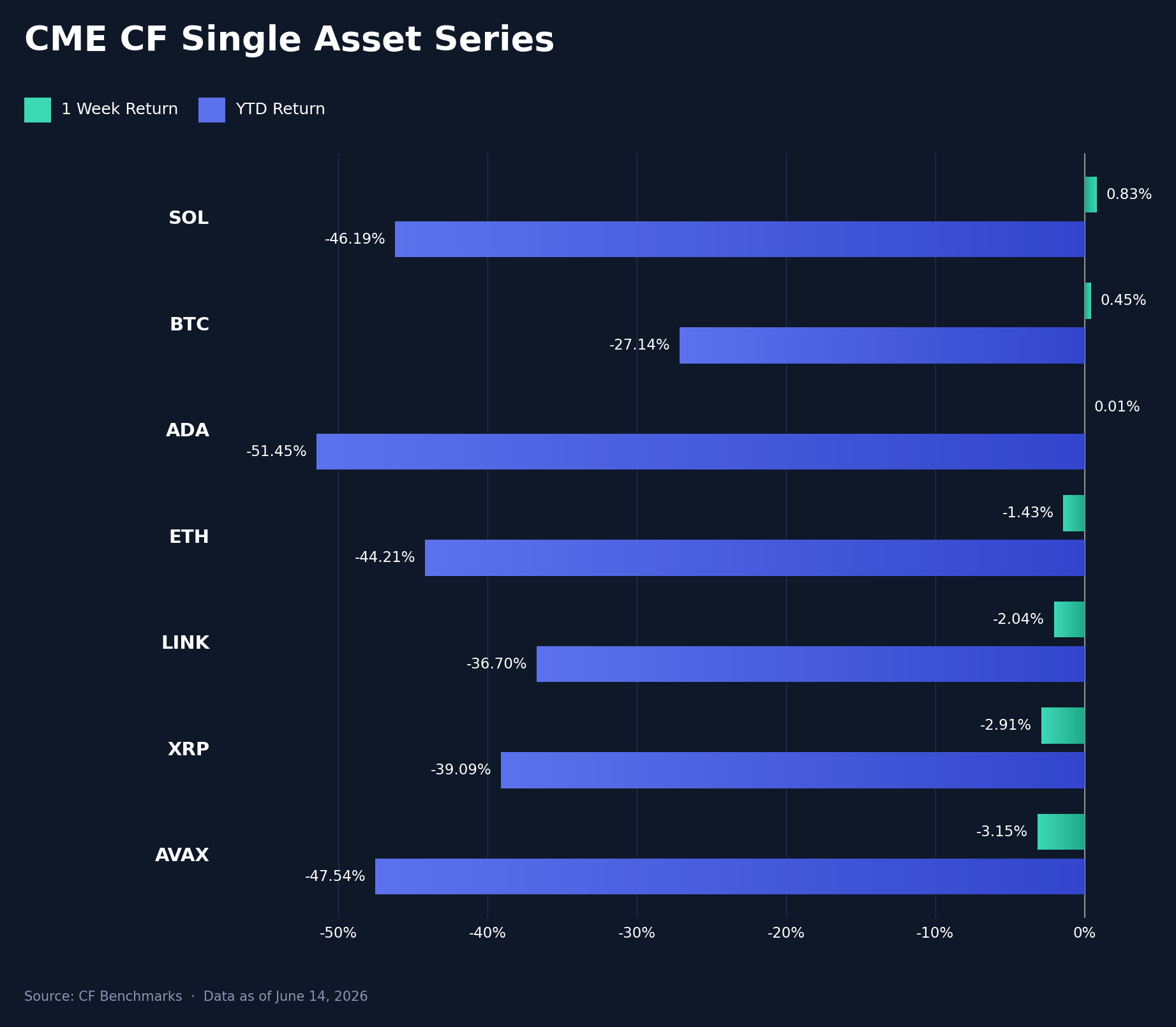

The seven CF Single Asset constituents finished tightly bunched and close to unchanged, a spread of just 3.98 pp separating Solana (SOL) at +0.83% from Avalanche (AVAX) at -3.15%. Bitcoin (BTC) added 0.45% and Cardano (ADA) was flat at +0.01%, while Ether (ETH, -1.43%), Chainlink (LINK, -2.04%) and XRP (-2.91%) gave back modest ground. That near-flat close masks a violent intraweek path. May headline CPI printed 4.2% YoY on June 10th, the highest in three years, with energy more than 60% of the monthly gain as the Iran conflict pushed gasoline up 40.5%; BTC fell about 3.5% into the release and traded near $61,000 as the United States struck Iranian targets the same session, with roughly $1bn of liquidations in 24 hours. The complex then recovered the lot: a cooler core CPI (+0.2% month over month, a tenth below consensus), softer University of Michigan inflation expectations (the 1-year eased to 4.6%, the 5-to-10-year to 3.4%) and a claimed settlement in the Iran conflict on June 14th rekindled sentiment across the space. No major decoupled from the rates-and-geopolitics tape in a way the prints can explain. On a YTD basis the majors remain deeply underwater, from BTC's -27.14% to ADA's -51.45%.

Volatility Analysis

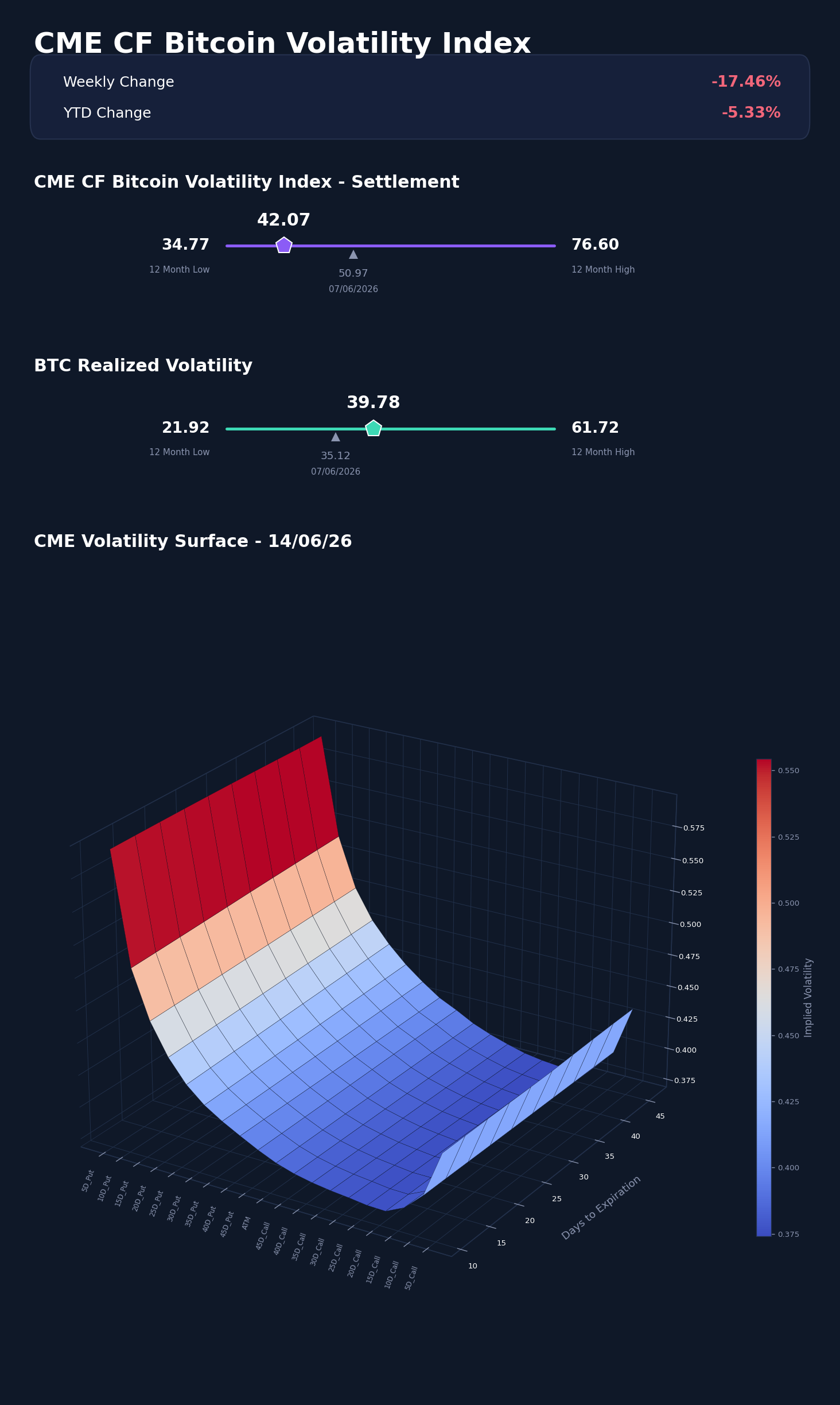

The volatility surface told the round-trip story more cleanly than spot did. CME CF Bitcoin Volatility Index Settlement (BVXS) fell from 50.97 a week earlier to 42.07, a drop of about 17.5% w/w and 8.90 vol. points, even with the Iran strikes and the CPI print landing midweek; implied vol spiked to 47.27 on June 9th and then bled lower for the rest of the week. Realized volatility moved the other way, rising from 35.12 to 39.78 as the daily ranges widened. The result was a sharp compression in the implied-realized spread, from about 15.85 vol. points a week ago to 2.29 now, the narrowest gap in months. Implied vol sits 7.30 points above its 12-month low of 34.77 and well beneath the 76.60 high; realized, at 39.78, is closer to the middle of its 21.92 to 61.72 band. The configuration is the signature of a market that has stopped paying up for protection it expected to need: forward-looking vol has normalized toward, and almost into, the volatility actually being delivered. That the spread closed while spot finished flat is consistent with our read of the week as the unwind of the prior week's stress rather than the start of a fresh one.

Market Cap Index Performance

Breadth confirmed the same near-flat, macro-neutral week. The free-float-weighted tiers finished within a whisker of unchanged, CF Ultra Cap 5 at +0.06%, the CF Institutional Digital Asset Index at +0.02%, and the free-float Large and Broad Cap indices at -0.17% and -0.18%; the whole six-index set fit inside a 1.21 pp range. The macro and geopolitical impulse hit the cap tiers together and they recovered together, which is why the free-float reads cluster around zero. The one separation was structural rather than macro: the diversified-weighted indices lagged their free-float counterparts, with CF Broad Cap Diversified (-1.07%) trailing CF Large Cap Free Float by 0.90 pp. That gap is small-cap and long-tail composition, the diversified weighting holding more of the lower-beta, weaker names; a market-wide inflation and conflict shock would not single out the tail, so we do not read it as a macro signal. Spot Bitcoin ETF flows fit the round-trip exactly, a $91.4m outflow on June 8th turning into an $85.9m, IBIT-led inflow on June 12th that snapped a five-day redemption streak, while ether funds faded to a small net weekly outflow. The late-week stabilization showed up as a modest flow turn, not fresh broad demand. On a YTD basis the indices remain down 31% to 36%.

Factors Analysis

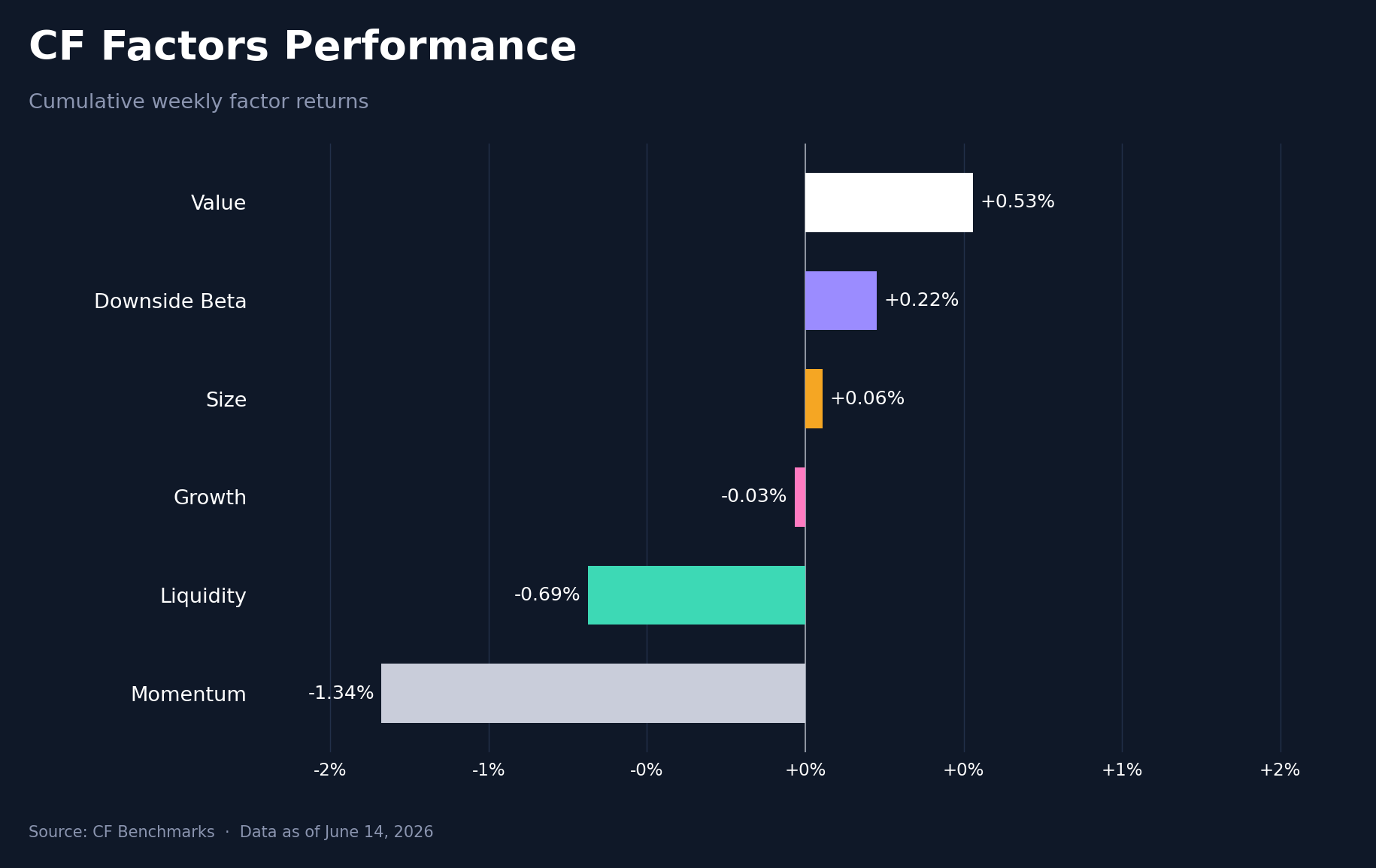

Within the week, factor returns were tightly packed, Value the best at +0.53% and Momentum the worst at -1.34%, a spread of only 1.87 pp. The story is in the week-on-week rotation, which was large and pointed one way: the unwind of the prior week's risk-off positioning. Downside Beta swung from -3.56% to +0.22%, a 3.78 pp reversal and the biggest of the set; Size, the prior week's clear leader at +3.38%, faded to +0.06%, a 3.32 pp give-back; and Momentum reversed from +1.24% to -1.34%, down 2.58 pp. Value flipped from -2.03% to +0.53%. Read together, these are the mirror image of a defensive week: the bid for large, low-beta quality that dominated the prior week's selloff drained out, and the most beaten-down, high-beta exposure stopped underperforming. The rotation is consistent with stabilization rather than a new risk impulse in either direction; no factor ran far enough this week to claim leadership, and the dispersion is too narrow to read as a style call. The cleaner signal is that the market spent the week giving back the factor tilts it put on under stress, not building new ones.

Read our latest weekly crypto factors report: Factor Friday - June 12, 2026

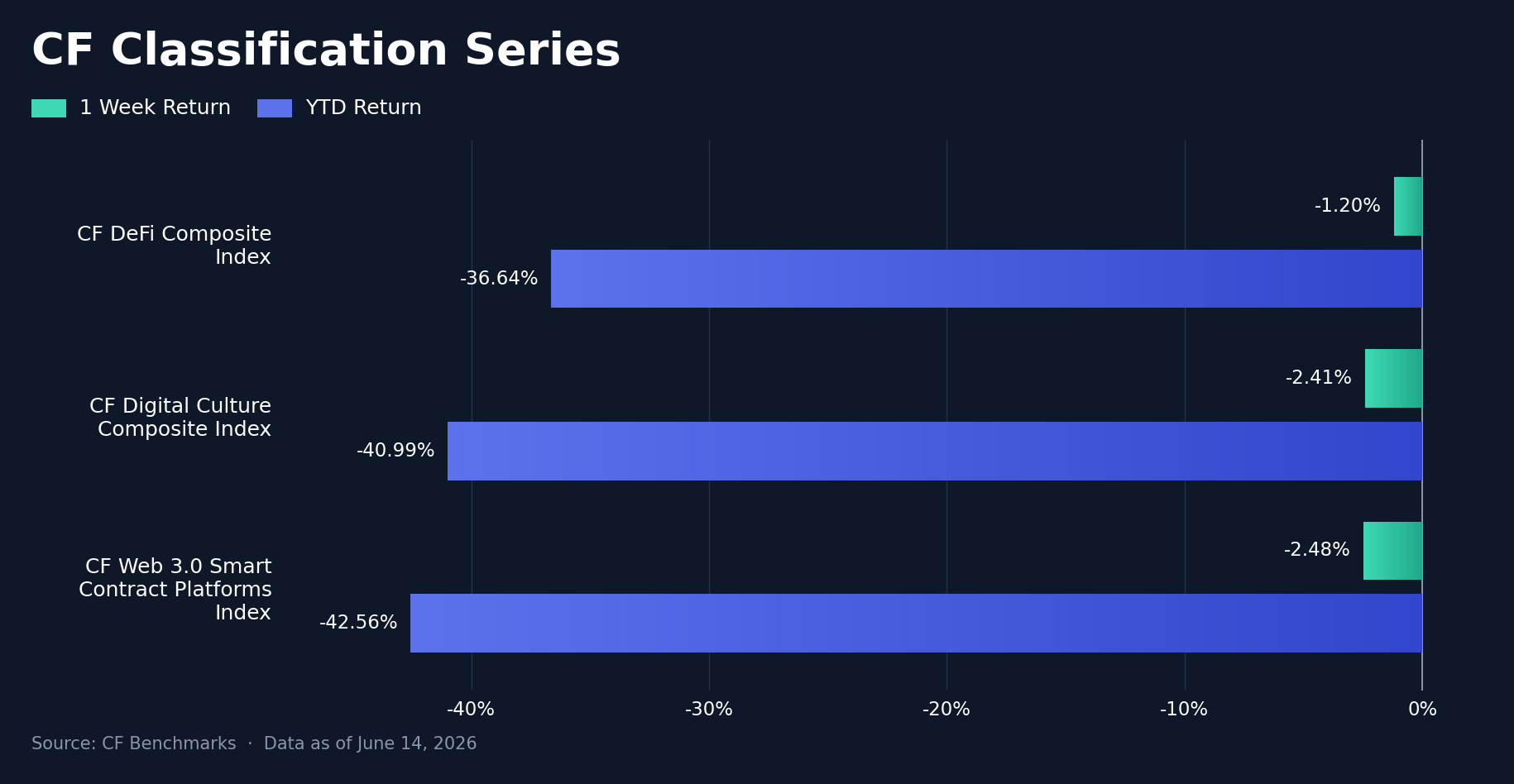

Classification Series Analysis

The three thematic composites all finished lower but in a narrow band. The CF DeFi Composite Index held up best at -1.20%, ahead of the CF Digital Culture Composite (-2.41%) and the CF Web 3.0 Smart Contract Platforms Index (-2.48%), a leadership spread of 1.28 pp between DeFi and the smart-contract platforms. DeFi's relative resilience fits the week's one constructive industry thread, a lending-product launch from Curve that lifted several Finance names, while the smart-contract platforms tracked the heavier large-cap alternative layer-1 tape. On a YTD basis the ordering is the same and the gaps wider, DeFi at -36.64% against Digital Culture at -40.99% and the platforms at -42.56%. None of the three separated enough this week to mark a thematic rotation; the read is modest, broad-based softness with DeFi the marginal outperformer.

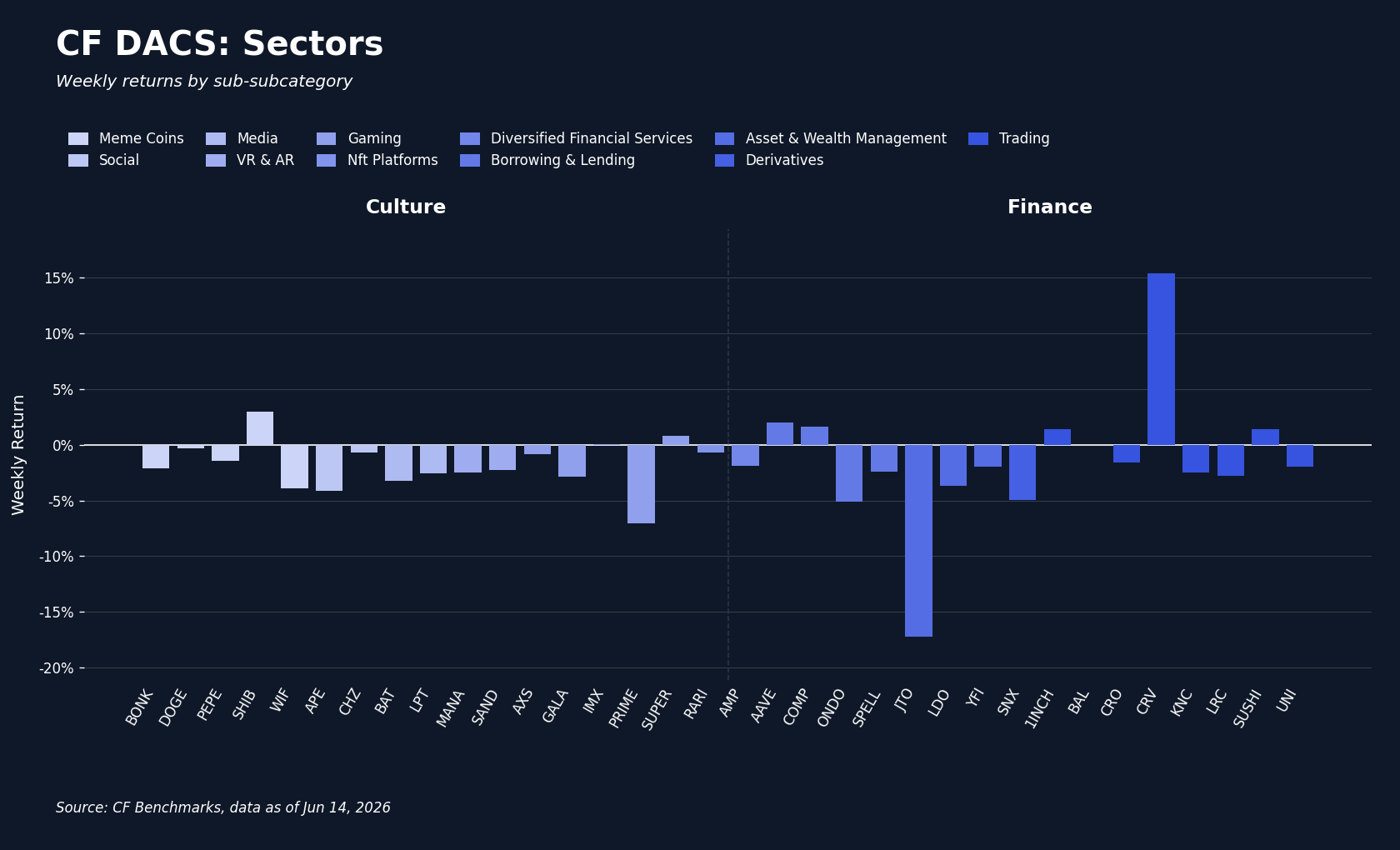

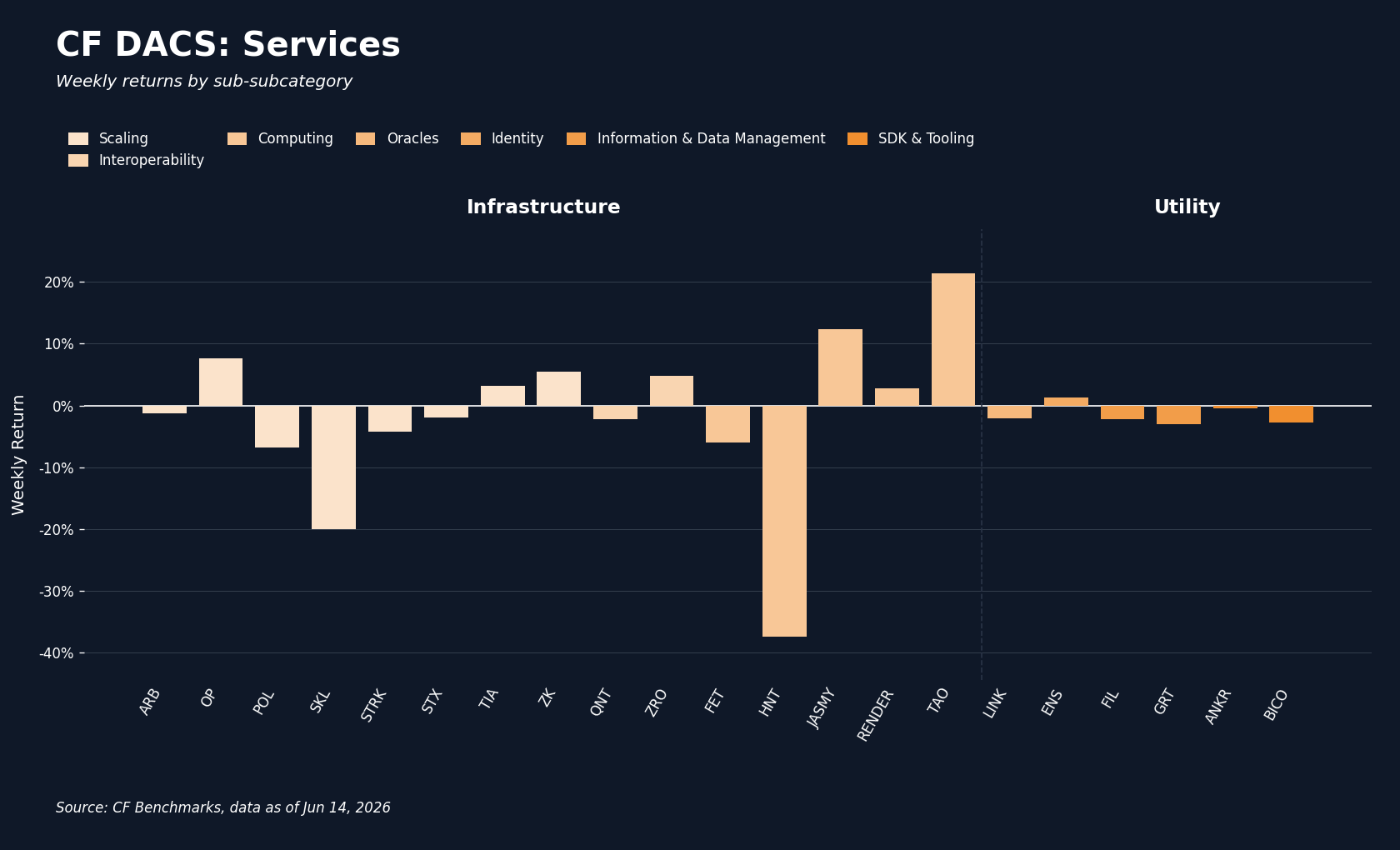

Sector Analysis

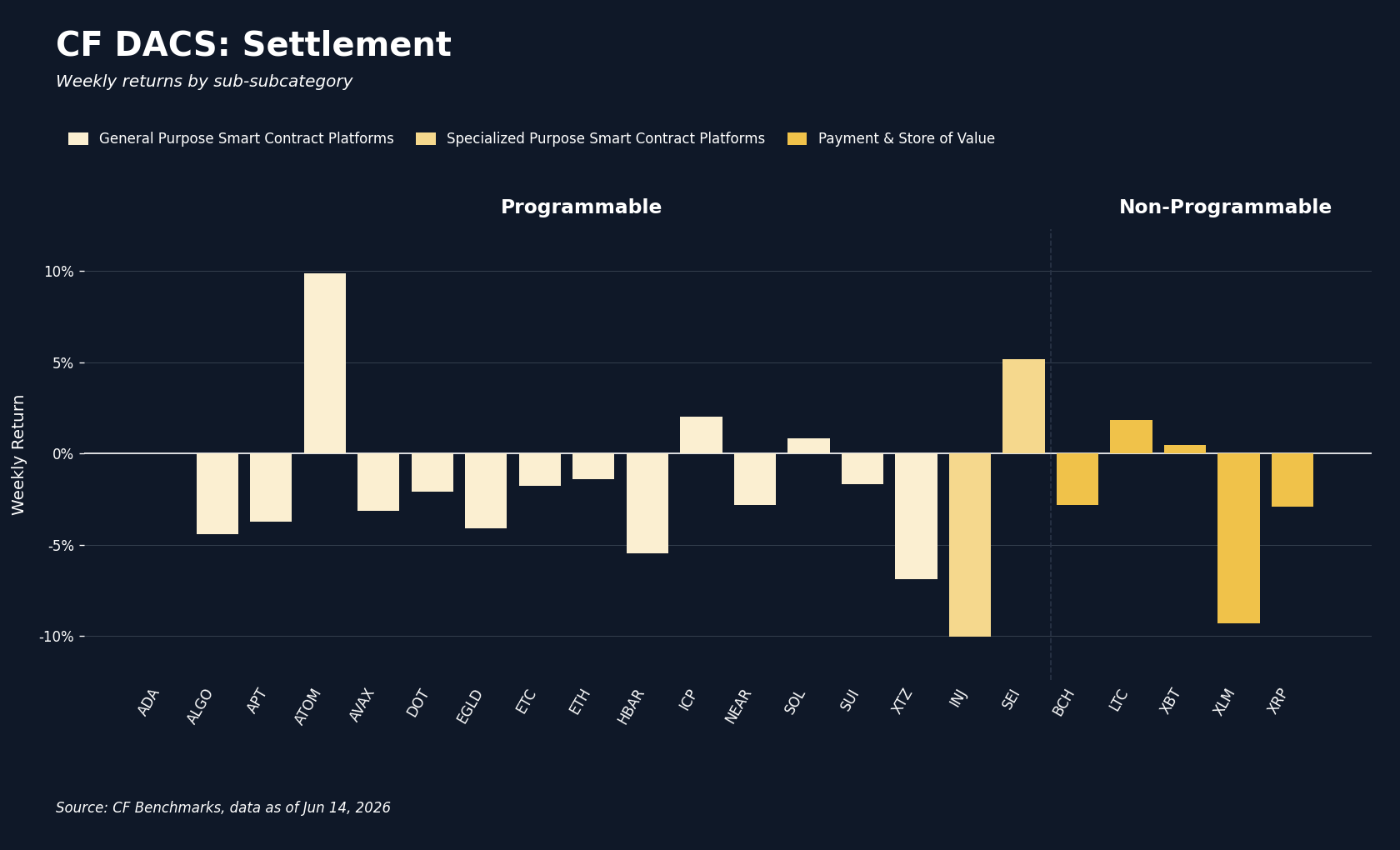

The CF DACS sub-category averages were the picture of a flat week, all six clustered between Finance at -1.41% and Non-Programmable at -2.55%. The averages conceal the most striking dispersion of the week. The widest token-level spread, 58.76 pp, sat entirely inside Infrastructure, between Bittensor (TAO) at +21.41% and Helium (HNT) at -37.35%. Both moves were catalyst-driven and pulled in opposite directions. TAO led a decentralized-AI bid after the US government barred foreign-national access to Anthropic's two most capable models on June 12th and the company pulled them; participants rotated toward AI networks framed as outside single-vendor and single-jurisdiction control, and TAO posted its largest gain in months. At the other extreme, HNT extended an idiosyncratic decline to a record low near $0.43, the continuation of a repricing that began with Nova Labs selling its Helium Mobile consumer arm in early June and founder Amir Haleem stepping down as chief executive on June 5th. Because the two sat at opposite ends of one sub-category, Infrastructure's -1.49% average says little about what happened inside it. Finance was the least-bad sector at -1.41%, helped by Curve DAO (CRV, +15.42%), which rallied after Curve launched its Llamalend v2 lending product on June 10th; that gain offset sharp drops in Jito (JTO, -17.20%) and Synthetix (SNX, -4.98%). Elsewhere the moves were smaller and price-led: Cosmos (ATOM, +9.87%) led Programmable while Injective (INJ, -10.02%) lagged, and Stellar (XLM, -9.32%) dragged Non-Programmable. The week's sector story is dispersion within Infrastructure, not direction across the complex.

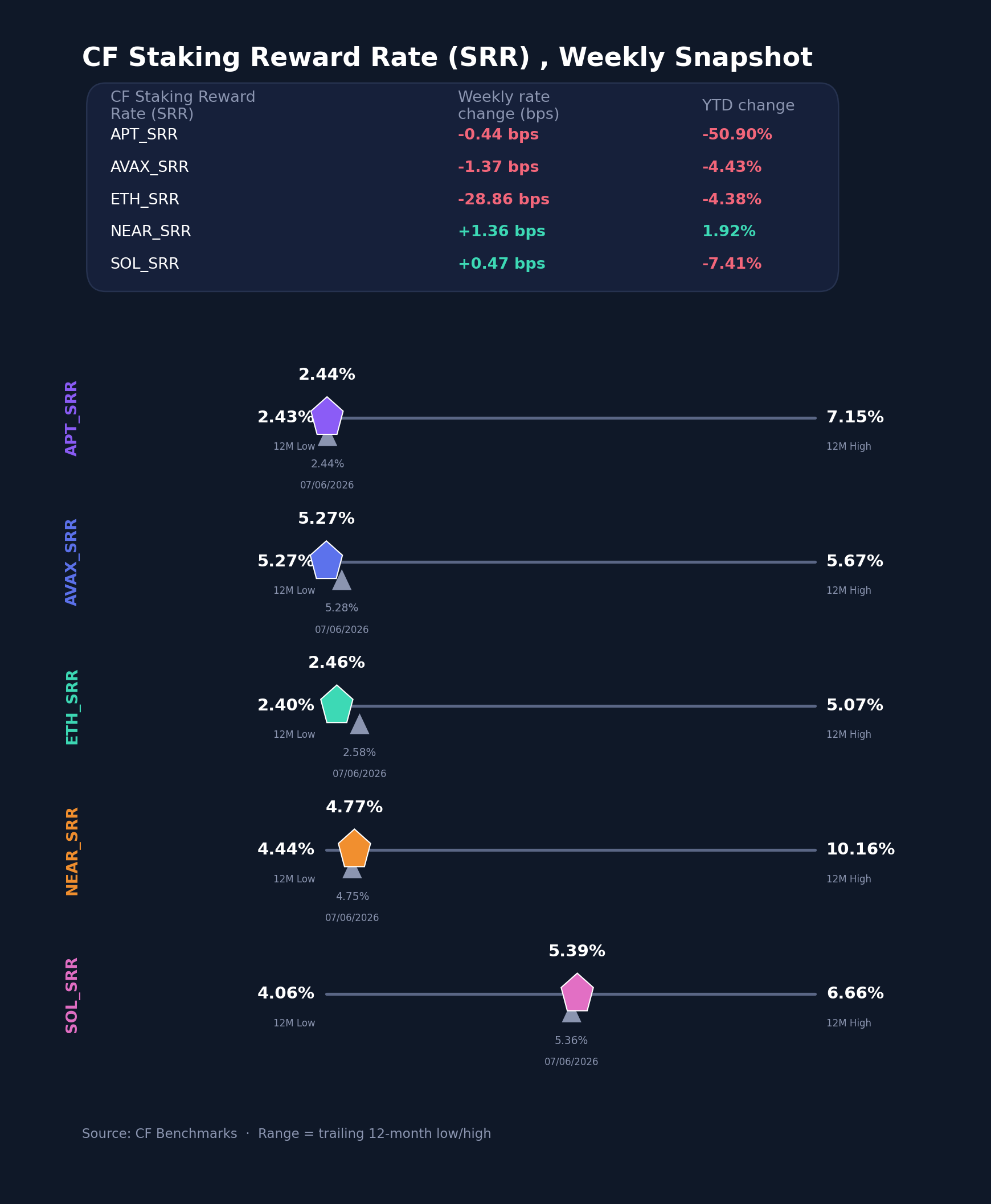

CF Staking Series

Reward rates across the five staking indices were broadly stable. APT (2.4370%), AVAX (5.2683%) and ETH eased while NEAR (4.7717%) and SOL (5.3931%) ticked higher, leaving SOL the highest reward rate of the set and APT the lowest, a spread of roughly 2.96 pp. Ether was the outlier: its reward rate eased from 2.5806% a week earlier to 2.4560%, and its published weekly rate change of -28.86 bps was by far the largest of the set, against single-digit-bps moves elsewhere (APT -0.44 bps, AVAX -1.37 bps, NEAR +1.36 bps, SOL +0.47 bps). The decline left ETH just above APT at the bottom of the reward range and reflects easing network staking yield rather than any change in index construction. SOL and NEAR's small increases kept them, with AVAX, at the high end of the curve. The set as a whole points to a quiet week for staking economics, with the ETH reward-rate decline the only data point worth flagging.

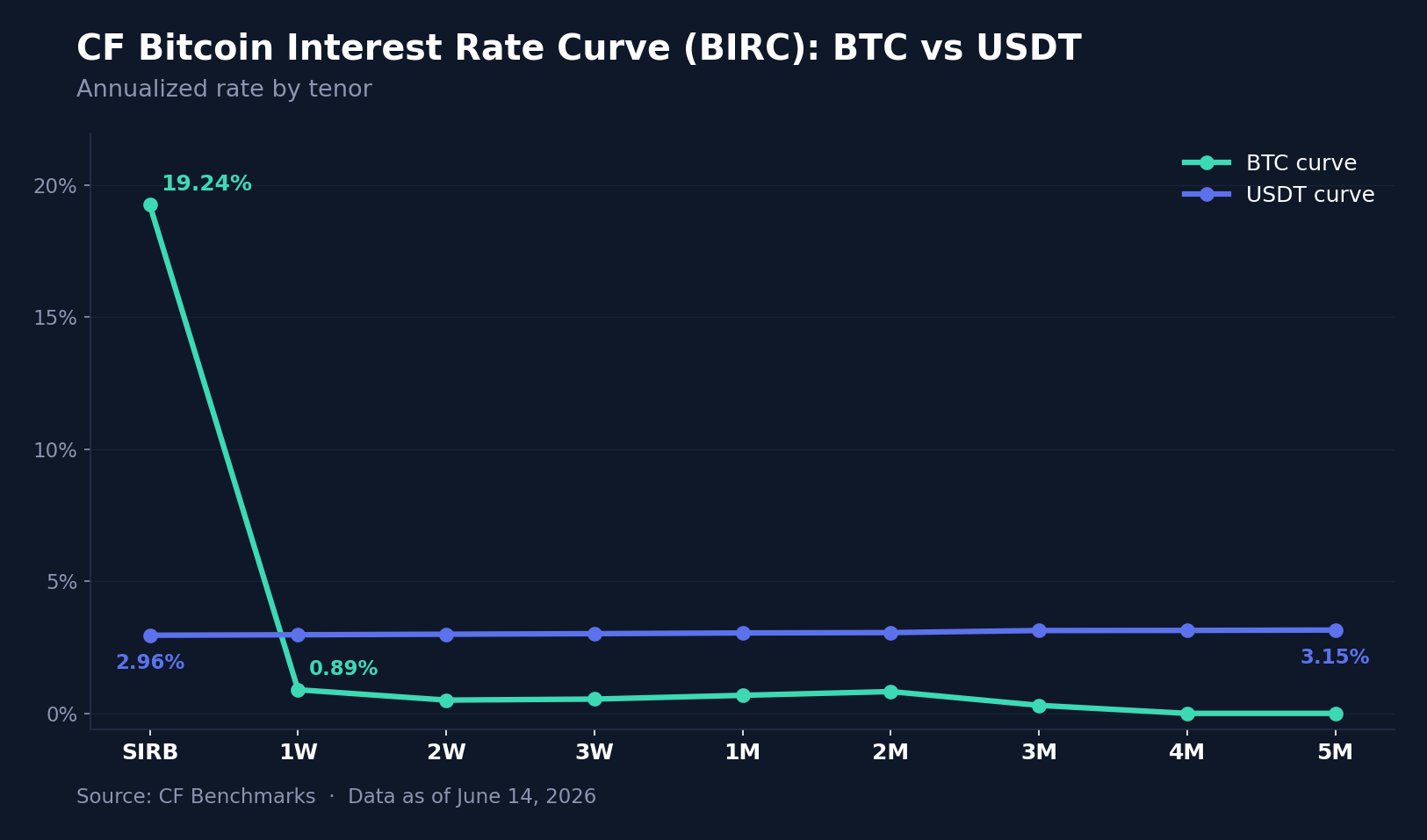

Interest Rate Analysis

The two CF Bitcoin Interest Rate Curve (BIRC) curves diverged sharply, and the action was all in the Bitcoin front end. The BTC spot reference borrow rate (SIRB) spiked 795.1 bps to 19.24%, a front-end dislocation, while the 1-week rate fell 239.1 bps to 0.89% and the 2-week eased to 0.50%; the rest of the BTC term structure sat below 1%, from 0.54% at 3 weeks to 0.30% at 3 months. The shape is an extreme version of the front-end-idiosyncratic pattern: an overnight borrow squeeze in Bitcoin that the term tenors did not follow and in places moved against (the 3-week and 1-month ticked up 14.6 and 16.2 bps while the 3-month fell 16.5 bps). The USDT curve, by contrast, barely moved. It held its gentle upward slope from 2.96% at SIRB to 3.15% at 5 months, with tenor changes of just +1.9 to +5.9 bps across the board. Dollar funding stayed orderly; the stress was specific to spot Bitcoin borrow. We read the SIRB spike as a positioning and collateral event at the very front of the BTC curve rather than a repricing of term carry, since neither the BTC term tenors nor the USDT curve corroborated it.

Taken together, the week is best understood as a round-trip. A three-year-high inflation print and renewed conflict in the Middle East moved the complex hard intraday and then let it back, leaving spot, breadth and the single-asset spread close to unchanged. The more durable signals were internal and pointed to stabilization: the defensive factor tilts of the prior week unwound, implied volatility fell back toward a rising realized until the cushion between them nearly closed, and dollar funding stayed calm even as Bitcoin's overnight borrow spiked. The clearest cross-sectional move came not from macro but from a single industry catalyst, the decentralized-AI bid that split Infrastructure between TAO and HNT. The complex absorbed a loud week and gave little ground; the rotation beneath the surface, not the headlines above it, is where the information was.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Factor Friday - August 7, 2026

Factor Friday: beta faded, with the Market down -0.81%, while capital reached down the risk curve. Liquidity led at +1.36% and Size followed at +1.07%, both sign-inverted, and Downside Beta anchored the field at -2.69%. All three point risk-seeking, and selection set returns, not direction.

Mark Pilipczuk

Bitcoin Drives a Rebound as Breadth Narrows

The CF Free-Float Broad Cap Index rose 4.44% in July as Bitcoin and Ether supplied 5.07 points of a 4.44% return. Softer inflation and new Ethereum exchange-traded product access carried the large-capitalization core, while 18 of 32 constituents fell and free-float weighting produced the gain.

Mark Pilipczuk

Changes to the Token Market Price Benchmarks Series - Market Prices – 04 August 2026

Changes to the Token Market Price Benchmarks Series - Market Prices – 04 August 2026

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.