May 04, 2026

CF Benchmarks Newsletter Issue 104

- How Late is too late for new US Bitcoin ETFs?

- CME ups crypto pace with new AVAX, SUI futures, ahead of 24/7

- Amundi lists BRR-based Bitcoin ETP on Euronext Paris

Useful

Around two years after the first U.S. spot Bitcoin ETFs solved the mainstream access problem, and as the market for listed digital asset funds there continues to fill out, the next big question that emerges quite naturally is 'which of these access points are most useful?'

It’s a thread we follow in this edition. The crux is that with more than $100bn of assets in aggregate, U.S. Bitcoin ETFs appear to be and are in fact a product category no major asset manager can comfortably ignore any longer; hence a spate of high-profile late entrants seems likely. Morgan Stanley, with MSBT, and Goldman Sachs pushing into adjacent Bitcoin income territory, are the first signs of this expected stream of late comers. But as tempting as that $100bn backdrop is, it also poses a few awkward questions.

To begin with the most obvious one, BlackRock’s iShares Bitcoin Trust ETF (IBIT) benchmarked to CF Benchmarks’ CME CF Bitcoin Reference Rate – New York Variant (BRRNY) has rapidly grown to become the category’s de facto liquidity centre. Our piece excerpted below spotlights that IBIT’s early flow lead was visible inside the first three months, then it grew larger. IBIT’s options market later added another layer of utility for traders, hedgers, structured-product desks and allocators who care about implementation costs as much as headline fees. In that setting, we might conclude that a new Bitcoin ETF needs to show more than a low expense ratio and a familiar logo. It also needs to be ‘useful’. And that leads us to what might be the most awkward question:

‘Is it now essentially too late to easily grab a meaningful part of that $100 billion pie by launching a new plain-vanilla spot Bitcoin ETF?’

It’s a stark question. And full disclosure: there is of course no clear answer, for now. But what is already clear, based on IBIT and other funds in Wall Street’s first cohort of crypto ETFs, is that medium-term flows and options utilization appear to be ‘useful’ indicators.

Other Highlights

- CME Group’s latest expansion of its crypto futures roster adds Avalanche and Sui; and with the countdown to round-the-clock crypto contract trading in its last few weeks, an outline of the implied efficiencies the initiative could serve.

- Bitwise moves further down the asset curve with its new BAVA ETF for Avalanche exposure – incorporating a new in-house staking model – and upcoming BHYP, which is set to bring Hyperliquid into the ETF wrapper for the first time.

- Meanwhile Volatility Shares’ new Chainlink, Cardano, Stellar 2x leveraged ETFs, test the outer edge of payoff design underpinned by CFB’s regulated pricing methodology.

- Amundi has launched the Amundi Bitcoin ETP (Euronext ticker: BTCA) giving investors exchange-traded exposure to Bitcoin through a physically backed product, listed on Euronext Paris.

Is It Too Late to Launch New US Bitcoin ETFs?

Early-flow lessons from the U.S. spot Bitcoin market

Too Big to Trail: The $100bn U.S. Bitcoin ETF Market

Institutional access to Bitcoin has moved quickly since the first U.S. spot Bitcoin ETPs began trading in January 2024. By late April 2026, the U.S. spot Bitcoin ETP market has become large, liquid, and highly concentrated. Public trackers (e.g. this one, provided by Farside Investors) put aggregate assets above $100bn, while BlackRock’s iShares Bitcoin Trust ETF (IBIT) holds around two thirds of these on its own at the time of writing, with net assets of around $63bn.

The Late-Mover’s Dilemma

That leaves late entrants facing a dilemma. The category is now too large for major asset managers to ignore, but it is also mature enough that first-mover advantages may be difficult to overcome. The Morgan Stanley Bitcoin Trust (MSBT) which listed earlier this month, appears to be the clearest current test. Morgan Stanley Investment Management notes that it is the first U.S. bank-affiliated asset manager to offer a cryptocurrency ETP, underlining that there are still plenty of major providers waiting on the sidelines. Among these, Goldman Sachs has also signaled that it too will wait no longer, filing a preliminary prospectus for the Goldman Sachs Bitcoin Premium Income ETF, adding to the sense that large traditional financial institutions are still looking for ways to join the category.

Is it Later Than We Think?

That is why whether it is now too late to launch a U.S. spot Bitcoin ETF is an interesting question.

This article asks whether early ETF flows can help us judge that late-mover problem. If the first 21, 42, and 63 trading days of the January 2024 cohort contained useful information about later asset gathering, then the first few months of a new fund, like MSBT may offer an early, public read on whether a late entrant can still build durable demand.

It should be stressed that MSBT is a test case and not the whole story.

What early flows can and can’t show

This study uses public flow, trading, issuer, and options data. From the outset we should be clear about what these data sets can show us to avoid being misleading The data can help us assess observable demand signals. They cannot identify end-investor type, advisor platform source, model-portfolio inclusion, internal bank-channel allocation, or the causal driver behind each daily flow.

That caveat is important because ETF flows are not a pure measure of long-term conviction. They can reflect seed capital, tactical trading, arbitrage activity, issuer relationships, tax-sensitive holders, fee changes, platform availability, market timing, launch curiosity, and wider market ‘regime’ at the time of a fund’s launch.

So, our test here is deliberately modest. Early flows do not dictate destiny. They can, however, show whether initial demand persisted once launch noise started to clear.

The working windows are 21, 42, and 63 trading days after launch or spot conversion. That gives us approximate one-, two-, and three-month readings while avoiding calendar quirks.

Same Bitcoin, Different ETFs

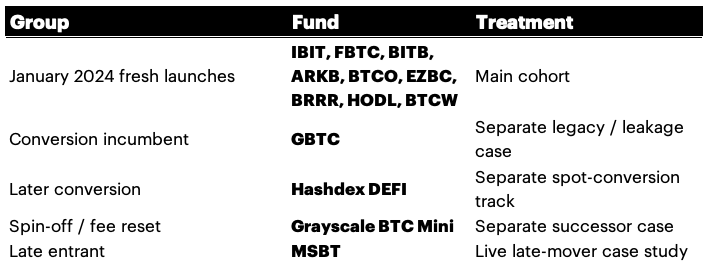

Another proviso: it’s important to note that while the cohort of brand new spot Bitcoin funds that were simultaneously listed in January 2024 is an important one, it’s not the only one. Bear in mind that not all U.S. Bitcoin ETFs started from the same place, and these differences can have consequences for early flows.

The January 2024 fresh launches are the cleanest cohort for testing early-flow persistence. Other funds need separate treatment because their launch circumstances were different. In the table below, we’ve summarized the key cohorts and how their differences denote specific treatments within our exploration.

Table 1 – Key U.S. Bitcoin ETF Cohorts

The main comparison should focus on the nine fresh January 2024 launches. Meanwhile, GBTC, BTC Mini, DEFI, and MSBT remain in view, but each needs its own product-history lens.

Signs of Hierarchy

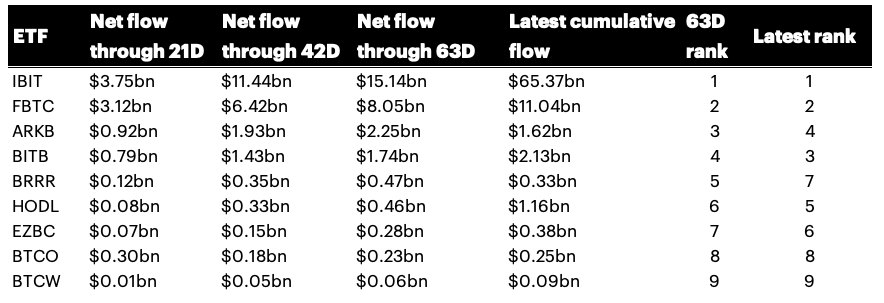

All that said, a cursory look at the first three months of flows for the main group already suggests the emergence of observable tiers.

The January 2024 fresh-launch cohort produced a clear hierarchy by the 63rd trading day, as illustrated by the table and graphics below.

Table 2 – January ’24 Cohort 3-Month Flow Performance

Click here to continue reading on our website.

CME Adds Sui, AVAX Futures

Newest CME Futures Offer AVAX, SUI Exposure

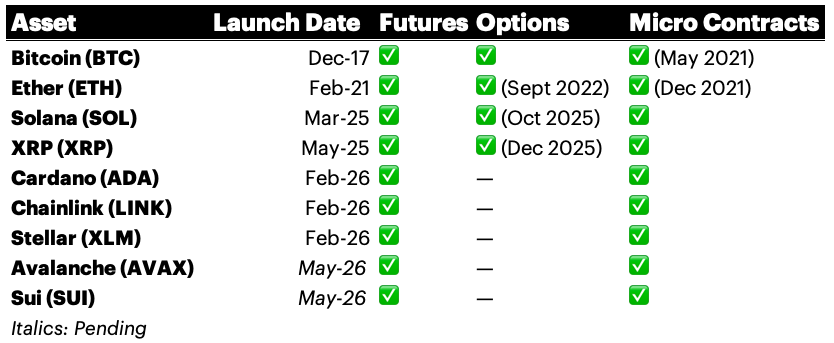

CME Group is set to continue its accelerated expansion of crypto asset exposure with the launch of Avalanche and Sui futures on Monday May 4th. In line with the most recent set of digital asset futures debuted on the leading derivatives marketplace, both larger and Micro contract sizes will be available from launch. AVAX futures will be sized at 5,000 AVAX, with Micro AVAX at 500 AVAX. SUI futures will be sized at 50,000 SUI, with Micro SUI at 5,000 SUI.

CME’s crypto futures settle to CME CF Reference Rates, usually the 4:00 p.m. London reference-rate family. Avalanche and Sui follow that pattern through AVAXUSD_RR and SUIUSD_RR.

Shortest Gap

The cadence of new CME crypto exposures will have reached its fastest yet when these contracts become available for trade. The gaps between new CME digital asset futures launches have narrowed steadily since the inception of Bitcoin futures in 2017, Ether in 2021, and Solana and XRP in 2025. With Cardano, Chainlink and Stellar arriving in February 2026, to be followed by Avalanche and Sui a few months later, five of CME’s nine single-asset crypto futures lines will have been launched in 2026 alone.

Meanwhile, the template of allowing a pause between the listing of full-sized contracts and minis appears to have been dispensed with since the introduction of SOL and XRP futures in 2025.

Prices Down, Volumes Up

CME’s Q1 numbers help explain the expansion. Crypto product average daily volume rose to 310,000 contracts from 191,000 a year earlier, despite lower crypto prices than in Q1 2025. Average daily open interest reached 313,900 contracts, up 25% year on year. The newer Cardano, Chainlink and Stellar futures saw nearly $116 million transacted since launch. Across the crypto product suite, cumulative notional volume passed $7.3 trillion.

Solana and XRP brought in two of the most heavily traded non-BTC/ETH assets. Cardano, Chainlink and Stellar added an older cohort with established communities, listings and institutional recognition. Avalanche and Sui push the set further into smart-contract infrastructure, where investor interest is increasingly tied to network activity, developer ecosystems and the prospect of differentiated on-chain use cases.

CME ‘24/7’

Meanwhile, from May 29th, CME cryptocurrency futures and options are on track to begin trading continuously on Globex and ClearPort. Seven-day clients will still have a daily two-minute maintenance window from 4:00 p.m. to 4:02 p.m. CT on Monday through Friday, plus a two-hour maintenance window on Saturday from 2:00 a.m. to 4:00 a.m. CT. Weekend and holiday trades will carry the next business day’s trade date, with clearing, settlement and regulatory reporting processed on the following business day.

Rational Alignment

The switch will represent an historical fracturing of tradition for CME, but also a rational alignment to the 24/7, 365 nature of spot crypto. Up till now, a position could be closed in the futures market on Friday, watch the underlying spot market move sharply over the weekend, then reopen on Sunday at a very different price. CME’s own analysis cites the March 2025 U.S. Strategic Crypto Reserve announcement, when spot markets added roughly $300 billion in market capitalization and Bitcoin futures reopened with a $10,000 gap. The same analysis found that weekend volatility has remained around 75% of weekday volatility, i.e., crypto does not wait for Monday.

With the widest possible trading window once the change is enacted, institutions will have more ways to express and hedge asset-specific risk. A seven-day trading week also reduces the dead zone between regulated derivatives and spot crypto. The combination moves CME closer to the rhythm of digital asset markets without abandoning the features that made CME relevant to institutions in the first place: clearing, margining, surveillance, contract standards and benchmark settlement.

Bitwise Debuts BAVA ETF With In-House Staking

Bitwise heads further out the curve with new Avalanche fund and tweaked Hyperliquid filing

BAVA Launched with In-House Staking Roll Out

Bitwise continues to lean into its profile as the leading U.S. digital assets focused investment manager with its newest listed U.S. ETF, and the progression of a filing for another that moves it closer to bringing another first-time exposure to the ETP wrapper.

The Bitwise Avalanche ETF (BAVA) launched in April with direct AVAX exposure, a 0.34% sponsor fee and a staking design that targets roughly 70% of the trust’s AVAX for staking. The balance is managed as a liquidity reserve. The fund references the CME CF Avalanche-Dollar Reference Rate – New York Variant.

BAVA also, in effect, debuts a new operating model for ETPs offering staking exposure. Here, staking will be managed through Bitwise Onchain Solutions, an in-house staking arm. It appears to be one of the first instances of a sponsor bringing staking closer to the centre of the stack. The most visible potentials are improvements in oversight, reduced dependency on external providers, and creation of a more direct line between validator performance, liquidity management and shareholder outcomes, alongside a self-evident increased onus on internal controls.

Bitwise notably acquired Chorus One earlier this year, enabling integration of a large institutional staking provider into Bitwise Onchain Solutions. The new unit suggests staking arrangements for BAVA could turn out to to be a template for other products going forward.

BHYP Approaches

Bitwise also last month updated its proposed Bitwise Hyperliquid ETF with the ticker BHYP and a reported 0.67% sponsor fee. The trust would hold HYPE directly, and strike NAV against the CF Hyperliquid-Dollar US Settlement Price (U_HYPEUSD_RR) while pursuing a secondary objective of deriving additional HYPE through staking. Hyperliquid is best known for high-performance on-chain trading, with an embedded central limit order book.

Volatility Shares Floats CFB-Powered LINK, ADA, XLM ETFs

Launches 2x Leveraged Alongside Spot Exposures

Welcome Volatility

Volatility Shares has added a mix and 2x and ordinary 1x ETFs to its broad roster, tied to Cardano, Chainlink and Stellar:

- Cardano ETF (Ticker: CRDD)

- 2x Cardano ETF (Ticker: CRDX)

- Stellar ETF (Ticker: STLR)

- 2x Stellar ETF (Ticker: STLU)

- Chainlink ETF (Ticker: CHNL)

- 2x Chainlink ETF (Ticker: CHNU)

The group’s newest funds are welcome additions to the ecosystem of products benchmarked to our regulated indices. The indices are respectively CME CF Cardano-Dollar Reference Rate - New York Variant, CME CF Stellar Lumens-Dollar Reference Rate - New York Variant, and CME CF Chainlink-Dollar Reference Rate - New York Variant.

The 2x funds target twice the daily performance of the relevant asset, before fees and expenses, over one day. They derive their exposure via futures and other derivatives, collateralized with cash-like instruments.

SEC Signal

A Volatility Shares January registration statement notably covered 1x, 2x and 3x versions of Cardano, Chainlink and Stellar funds. By the time the March 31st amendment completed the registration process though, only the 1x and 2x funds were moving ahead. The choreography is in line with SEC’s recent observed resistance to higher-leverage ETF filings.

As such the SEC may have tacitly and informally signaled the crypto ETF leverage rate it may permit for the time being.

Amundi Bitcoin ETP (BTCA) Lists on Euronext Paris, Priced by CF Benchmarks

Amundi selects CFB index to price first physical crypto ETP

Amundi Bitcoin ETP Lists on Euronext

Amundi has launched the Amundi Bitcoin ETP (Euronext ticker: BTCA) giving investors exchange-traded exposure to Bitcoin through a physically backed product - listed on Euronext Paris.

The ETP's Bitcoin custodian is CACEIS, a Crypto Asset Service Provider (CASP), approved by France’s ACPR, for the custody and administration of digital assets under the EU's MiCA framework.

BTCA is designed to provide access to Bitcoin’s price performance through a traditional securities-market instrument.

Familiar Wrapper for Bitcoin Exposure

The launch provides institutions with another route to Bitcoin exposure in Europe through the ETP format. Rather than requiring direct holding of Bitcoin, private-key management, or direct interaction with crypto trading venues, the product packages exposure inside a listed instrument that can be accessed through existing market infrastructure.

The structure matters for investors seeking operational simplicity. The ETP format does not alter the underlying volatility or risk profile of Bitcoin, but it does change the way exposure is accessed, held, and monitored within portfolios.

The Leading Bitcoin Benchmark: BRR

The Amundi Bitcoin ETP uses the CME CF Bitcoin Reference Rate, or BRR, as its Bitcoin reference price.

Administered by CF Benchmarks, BRR is a Registered Benchmark under the UK Benchmarks Regulation (BMR) framework. It has been calculated since November 2016 and is the most liquid Bitcoin price for institutional risk settlement, having settled some $4.0 trillion in cumulative notional volume of CME Bitcoin futures since inception of the contracts in December 2017.

BRR’s transparent, rules-based architecture and proven replicability furnish Amundi Bitcoin ETP with the most accurate and efficient Bitcoin pricing mechanism available.

Material Addition to Europe’s Listed Crypto Market

Amundi’s Bitcoin ETP is a material extension of listed digital asset access by one of Europe’s largest asset managers. The launch offers investors another physically backed Bitcoin product, with valuation anchored to a benchmark already used across institutional crypto products and derivatives markets.

For CF Benchmarks, the listing reinforces the role of the CME CF Bitcoin Reference Rate (BRR) as the core pricing infrastructure for regulated and exchange-traded Bitcoin exposure.

Discover More

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.