Mar 29, 2026

CF Benchmarks Newsletter Issue 103

- Kraken's xStocks Will Power Nasdaq's Tokenized Equities

- Hashi: the New Bitcoin Collateral Layer, Priced by CF Benchmarks

- CF Benchmarks Research: Understanding Bitcoin's Split from M2

Patience

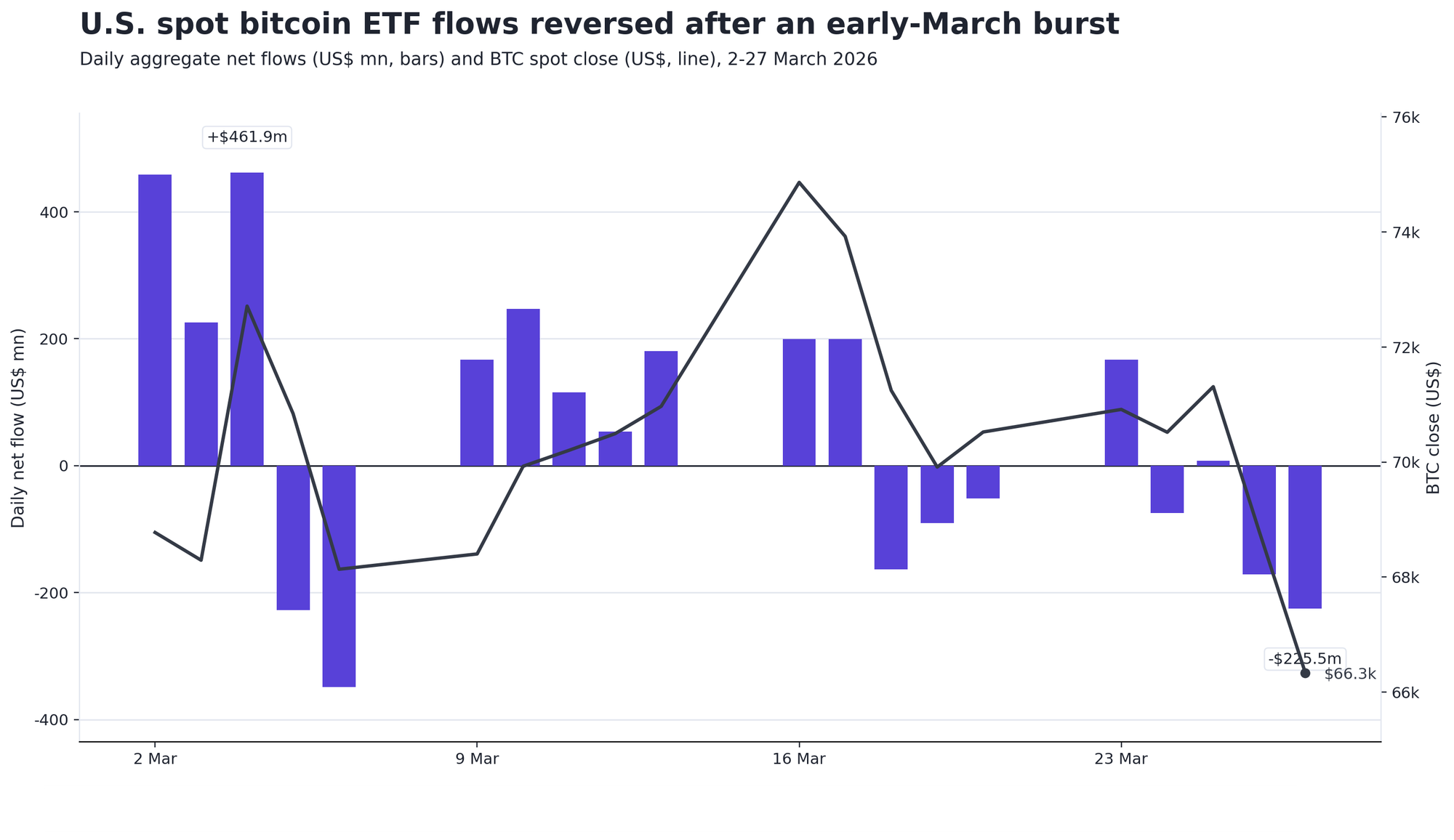

March tallies show how conditional ETF demand has become under the current market regime. U.S. spot Bitcoin ETFs took in $458.2 million on March 2nd, $225.2 million on March 3rd, and $461.9 million on March 4th, a three-session burst of $1.15 billion. Decrypt's 'Bitcoin is Abnormal' commentary captured the same turn in the tape from another angle, noting roughly $1.16 billion of inflows over seven consecutive sessions through March 17th even as Bitcoin struggled to hold gains.

Predictably, with Bitcoin having tumbled below the long-respected support level of $74k in early February and having remained becalmed beneath ever since, the short-term bid reflected by a fleeting bout of flows was doomed.

Bitcoin’s institutional close on Friday, March 27th as depicted by the CME CF Bitcoin Reference Rate – New York Variant (BRRNY): $66,828.24.

Farside’s daily data show U.S. spot Bitcoin ETFs lost $171.3 million on March 26th and $225.5 million on March 27th. Adding the daily totals from March 23rd through March 27th leaves the week negative by roughly $296 million. With Bitcoin back on the $66k handle, the market is evidently still trading like a risk asset; when oil, inflation, and the dollar turn against it. The recent flow profile illustrates that ETF demand persists, albeit patience is wearing thin.

Figure 1 - U.S. Spot Bitcoin ETF Flows - March 2 - March 27

Durable Verdict

As ever cumulative totals provide the durable verdict on institutional demand. Since launch, U.S. spot Bitcoin ETFs have taken in $55.9 billion net, with iShares Bitcoin ETF (IBIT) the biggest BTC ETF in the world in terms of its assets – benchmarked to BRRNY - alone accounting for $63.1 billion and GBTC offsetting $26.0 billion, through persistent redemptions. Ether remains much smaller at $11.55 billion cumulative net inflows, and late March softened there too, with $92.5 million of outflows on March 26th and $48.5 million on March 27. Solana is earlier in its cycle at $981 million cumulative net flows, and it also saw redemptions on March 27th.

All told, the read-through isn’t complicated. Institutions have not walked away from Bitcoin. They are allocating tactically, pulling size forward when macro pressure eases, then cutting exposure fast when that pressure returns. For Bitcoin, ETF flows still provide the shortest path between macro conditions and spot demand. A market built on regulated wrappers can still trade like a nervous one. That’s another sign of asset normalization.

Also in this edition: the rapid evolution of xStocks, as Kraken's new partnership with Nasdaq coincides with the exchange's bid to transact tokenized equities on its stocks order book; what CFB-powered Bitcoin collateral on Sui's Hashi could mean for credit-attuned institutions; and how the CFTC is maintaining its new active cadence.

xStocks Head to Nasdaq’s Order Book

The 'where next?' question for CFB-powered xStocks is partly answered by Payward's new partnership with Nasdaq.

xStocks x Nasdaq

Eight months and $25 billion in transaction volume after launch, Kraken’s xStocks offering is about as far as it could possibly be from being credibly dismissed as the side experiment in crypto distribution that it may have been seen as, in those now distant first few weeks of June 2025.

CF Benchmarks’ regulated index methodology is the CPU powering the xStocks pricing circuitry.

Click below to catch the latest CFB Talks Digital Assets podcast featuring xStocks.

With interoperability, 24/7 availability, composability, low-costs and other blockchain characteristics already rooted in xStocks' crypto-native foundations, the recently announced partnership between Kraken parent Payward and Nasdaq is one answer to the key question of ‘what’s next?’, albeit obviously not an exhaustive one.

Tokenization Approved

In fact, the news raises ever more fundamental questions about the likely further evolution of Kraken xStocks, and perhaps the tokenized equities project more broadly.

Chiefly: whether (or ‘how long?’) the tokenized equity layer will remain in a parallel infrastructure; or whether it will move into the plumbing of incumbent exchanges (and if so, ‘how soon?’)

Another recent development has again provided the answer. Under the Nasdaq-proposed and, now, SEC-approved framework, tokenized securities can trade in the Nasdaq Market Center together with their traditional counterparts, on the same order book, with the same execution priority, the same CUSIP, the same material shareholder rights, the same market-data treatment, the same surveillance stack, and DTC still underneath settlement.

This means tokenization is moving closer to becoming a change in issuance, record keeping, and transfer mechanics inside the existing market rather than as a detour around it. (I.e., compared to existing synthetic wrappers or offshore look-solutions).

Institutional rationale

As such, the institutional rationale for xStocks is becoming clearer still. Kraken has already shown there is appetite for equity exposure with crypto-native traits: round-the-clock access, transferability, self-custody, and on-chain utility. The Nasdaq link takes that demand and points it toward a regulated U.S. pathway built around issuer rights, interoperability, and exchange discipline. Tokenized equities are being pulled toward the same controls that govern ordinary shares.

Nasdaq currently expects it will take till the first half of 2027 for its equity-token services underpinned by the xStocks infrastructure to become operational. Even so, the tokenized share is now moving closer to the exchange rather than further from it.

Note that from inception, xStocks have been built from the ground up to be institutionally ready. Including tried and trusted, demonstrably secure, regulated pricing.

Hashi Turns CFB-Priced Bitcoin into Collateral

Hashi’s launch on the Sui network puts native BTC into programmable collateral workflows for credit origination and lending, with stablecoins inside the structure as well.

CF Benchmarks is supplying the CME CF Bitcoin Reference Rate (BRR) and its New York, Asia Pacific, and real-time variants into that stack, so valuation, monitoring, and liquidation sit on regulated reference rates rather than venue-by-venue pricing.

Click below to read our post on the launch of the Hashi dev net.

Hashi Brings Institutional Credit Clarity

It’s worth outlining at a high level here how this evolution tilts the institutional conversation. Treasury strategies and ETF allocations turned Bitcoin into a familiar holding. Credit markets require something harder. Lenders need collateral calls that can fire on time. Borrowers need terms they can inspect before capital is posted. Both sides need a price they can defend when a position goes wrong. Within Hashi, native Bitcoin remains on the Bitcoin network, loan logic is enforced in smart contracts, LTV parameters and liquidation rules are set in code, and real-time oracles update valuations continuously.

All this enhances that always-needed though often tacitly addressed critical prerequisite for credit markets: trust. Hashi is in fact the antidote to the failure of centralized collateral models, opaque credit structures, and hidden trust assumptions, as it essentially compresses that trust surface.

Hashi’s Smart Infrastructure

The platform reduces the model to two explicit assumptions — the Sui validator set and the governing loan contract — then adds a guardian layer as a secondary control. It also plans custody-layer Bitcoin insurance. That does not remove risk. It does make the risk legible.

As this architecture gains traction, Bitcoin moves on from its passive reserve asset architecture, and closer towards it’s long sought profile as a collateral asset, that can support financing activity without disappearing into a lender’s black box. That is obviously an institutional enhancement, as the major capital counterparties are again looking for ways to finance against BTC at scale, without repeating 2022.

Hashi is an attempt to answer that question in code, with CF Benchmarks’ regulated pricing doing a large share of the heavy lifting.

New CFTC Task Force Amid Gathering Prediction Storm

Prediction markets shaping up to be a key arena for SEC-CFTC coordination.

Seemingly intent on making up for ground lost during a year with no permanent leadership, the CFTC continues its recently established cadence of initiatives on a channel regulated crypto asset participants ought to be tuned to.

CFTC Launches Innovation Task Force

More specifically, the new CFTC-SEC choreography we spotlighted in the prior edition now has a live test case. On March 24th, chair Michael Selig launched the CFTC Innovation Task Force focused on crypto assets, artificial intelligence, and prediction markets, and said it would coordinate with the SEC and its Crypto Task Force. A week earlier, the SEC and CFTC had issued a joint interpretation clarifying how federal securities laws apply to certain crypto assets and stating that the CFTC will administer the Commodity Exchange Act consistently with that interpretation. Coordination is moving from speeches into operating process.

Pertaining to Predictions

Prediction markets could be the sharpest place to watch that change. Selig has already taken a firm line, filing an amicus brief in February to defend the CFTC’s exclusive jurisdiction over prediction markets and writing that nearly 50 state cases are trying to narrow federal authority.

On March 12, the CFTC followed with an advance notice of proposed rulemaking on event contracts. That is a rare combination of litigation posture and rulemaking posture aimed at the same segment.

Prediction Battle Begins

It comes as political pressure is rising just as fast. Senators Adam Schiff and John Curtis have introduced the Prediction Markets Are Gambling Act to prohibit CFTC-registered entities from listing sports and casino-style event contracts. As well, California moved earlier this week to bar gubernatorial appointees from using nonpublic information on platforms such as Kalshi and Polymarket.

So, the agencies are trying to draw workable jurisdictional lines at the same moment that Congress and the states are escalating the public fight over where financial hedging ends and gambling begins.

CFTC regulated prediction markets include the largest in this set, in trading volume terms, Kalshi, which uses CF Benchmarks indices for crypto settlement. These operators sit close enough to derivatives, platform design, political controversy, and public-market structure that agencies cannot finesse the boundary question for long.

If they can make the federal split work, firms building across spot, derivatives, and tokenized products will have a clearer map of where each regulator intends to stand.

In any case, those like Kalshi, with a regulated pricing set for one of their most contentious markets, crypto, would appear to have an edge.

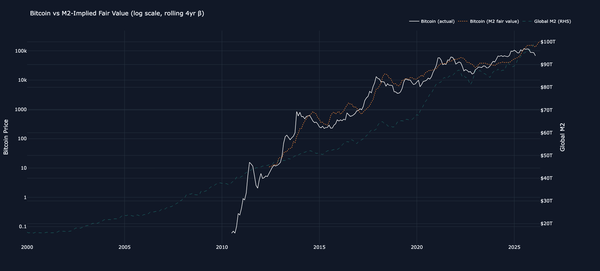

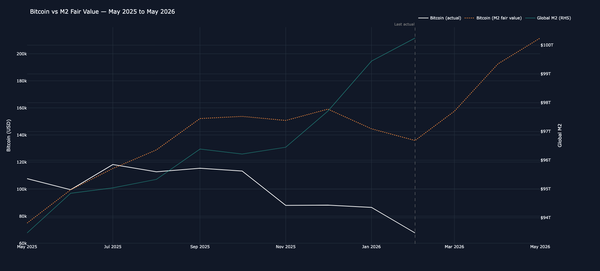

When M2 stops explaining Bitcoin

We showcase a report by CF Benchmarks’ Head of Research Gabe Selby, CFA, and Research Analyst Mark Pilipczuk – ‘The M2-Bitcoin Relationship: What the Data Actually Shows’.

M2-BTC Decouple

For most of the past decade, Bitcoin and global M2 moved with enough consistency to make liquidity a usable valuation frame. A report by CF Benchmarks’ Gabe Selby, CFA, and Mark Pilipczuk puts the rolling four-year correlation mostly in a 0.4 to 0.6 range. Then 2025 broke the pattern. Over the prior twelve months, global M2 rose more than 12% while Bitcoin fell roughly 12%. (See excerpted images below). This is the question the report is trying to solve.

Gold Shines a Light

The report compares Bitcoin with gold and global equities rather than treating the break as a Bitcoin-only mystery. Gold and equities responded to the liquidity backdrop in more conventional fashion. Bitcoin did not. The residual Z-score work makes that plain: Bitcoin moved sharply negative relative to its M2 fair value, gold climbed to historically elevated positive readings, and global equities stayed better aligned with liquidity. In other words, the liquidity bid seems to have found alternative destinations.

The report then lays out three routes by which the relationship could reconnect: a return to Federal Reserve balance-sheet expansion, a renewed appetite for growth risk, and a reversal in ETF flows. That last point is especially relevant now. The report notes $3.5 billion in net outflows from U.S. spot Bitcoin ETFs from November 2025 to January 2026, the worst three-month stretch on record, and argues that ETF flows have become the main transmission line between macro conditions and Bitcoin’s price. That is a sharper institutional framing than the usual “money printer” shorthand.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.