Mar 17, 2026

CF Benchmarks Newsletter Issue 102

Demand

At the cusp of 2025/26, our ‘Wall of Filings’ round-up of what was then – and remains now, by any standards – a massive slate of incoming U.S. crypto ETFs, zeroed in on several expected themes visible in the prospective vehicles, which looked set to change the contour of exposure available to investors in the months to come.

- While barely a prediction due to the trend already being well-underway at the end of December, the shift towards multi-asset funds was set to be among the most circumstantial, and it still is.

- The further normalization of staking, was also one of the easier calls, and continues to be roundly vindicated, not least by the launch of BlackRock’s first staking ETF (ETHB) in recent days. As outlined further down, ETHB's pace of asset-gathering could soon place it among the largest staking ETFs.

- Another standout frame: the reemergence of ’40 Act crypto ETFs, despite that structure having been eschewed by issuers at the inception of new product class.

- Payoff-engineering: More granularly, an increase in the variety of exposure types on offer – partly fostered by the 40 Act comeback – as sponsors move towards greater flexibility in how gross returns are structured, was also seen as likely.

The listings tape over the last few weeks has been imprinted with those key trends – often involving new products referencing CF Benchmarks indices.

BlackRock's ETHB | 21Shares' TDOT | New CFB Analytics

BlackRock launched iShares Staked Ethereum Trust ETF (ETHB), its first ETF to include exposure to staking rewards, on March 12th. ETHB is benchmarked to the CME CF Ether-Dollar Reference Rate - New York Variant (ETHUSD_NY). With the trading volumes of some $15 million reported on its first day, and net assets standing at $152.5 million a day later, ETHB is among the fastest-growing funds of the year so far.

Meanwhile, 21Shares listed the first U.S. Polkadot ETF (Nasdaq ticker: TDOT) on March 6th. Although much further down the capitalization and mainstream awareness tiers, TDOT AuM had reached $12 million 10 days after its launch.

Without minimizing the value destruction and potential deterioration of longer-term sentiment from the recent price downturn, it's notable that these institutional products have not subsisted on marginal demand in their first few weeks, which is obviously constructive.

Elsewhere in this edition, you'll find a write-up on the latest analytics based on our partnership with CME Group, enabling provision of exclusive datasets and tools for professional workflows.

ETFs: Basket and Second-Tier Trends Accelerate

BlackRock’s ETHB, 21Shares’ TDOT and 3iQ-backed DXMC expand North America’s crypto ETF envelope well beyond the vanilla zone.

21Shares’ TDOT Passes Demand Test with Flying Colors

21shares Polkadot ETF (Nasdaq: TDOT) which began trading on March 6th, ticks a bunch of the boxes we outlined above. Almost trivially at this point, note it's a ’40 Act fund. More importantly, it is of course the first U.S.-listed Polkadot ETF. This means that among other characteristics, it’s the furthest down the capitalization tier a significant U.S. issuer has ventured with a crypto offering so far.

The fund’s Polkadot reference is our CME CF Polkadot-Dollar Reference Rate - New York Variant (DOTUSD_NY).

DOT: Deep into the Stack

Just as importantly, as a so-called ‘layer zero’ protocol focused on interoperability, Polkadot (DOT) is categorized by our CF DACS—the leading institutional-grade digital asset taxonomy—as a General Purpose Smart Contract Platforms protocol. This places DOT among a very small set of peer networks. In turn, that makes the exposure now available from TDOT even rarer for the ETF wrapper.

In fact, TDOT is quietly one of the toughest tests of Wall Street demand for crypto seen to date. Yet with some $12.6 million in assets on the product page in the second week of its existence, TDOT demand has been firm.

Meanwhile, as much as 100% of the ETF's DOT holdings could be staked, though the amount is variable, and fund docs state that between 40%-70% is more likely, based on an analysis of historical utilization rates.

Strong ETF demand, for a staking asset deep into the least-mainstream corners of crypto capitalization and characterization. These are positive signals, given the tenor of recent sentiment, while also underscoring that the currents we teased out as pending at the end of last year, appear to be well underway.

Scotiabank, 3iQ Partner on Portfolio ETF

Although obviously outside the SEC’s purview as a Canadian issuer, 3iQ, which runs some the largest digital asset ETFs in that region – and some of the earliest thematically – was in the mix for one of the most thought-provoking recent launches. The circa C$1 billion AuM group has partnered with Dynamic Funds – an asset manager ultimately owned by ‘Big Five’ lender Scotiabank – to launch Dynamic Active Multi-Crypto ETF (Ticker: DXMC). The fund was listed on Cboe Canada on March 4th.

DXMC represents the basket expression of how North American crypto ETFs are evolving. Dynamic, an 1832 Asset Management business, is running the fund with 3iQ as sub-adviser. DXMC holds an actively managed mix of Bitcoin, Ether, Solana and XRP, and can also allocate part of the portfolio to equities tied to Web3, blockchain and related technologies. (The plan is to hold around 10% in such stocks). Cutting-edge bona fides are rounded off with staking being among strategies for ETH and SOL returns.

Active, Staking, Stocks

DXMC fits the format that, as we noted in December, maps more naturally to investment committee logic and model portfolios, especially as diversified exposure becomes easier to defend than a stack of single-token wrappers. The launch also shows how quickly issuers are moving past the plain spot template, with active selection, staking and equities all inside one listed product.

DXMC is also notable for its fee. A promotional rate of 0.25% will be in place till March 2027, at which point the standard 0.45% will kick in. That will still be well below the average 1.40% (on a one-year basis; excluding subscription and redemption fees) for an actively managed equity vehicle, according to an EY study from 2025.

While a speculative supposition, it makes sense that opting to structure DXMC’s crypto exposure from existing 3iQ funds – all of which reference CF Benchmarks indices – would help keep portfolio transaction costs low, and the management expense ratio (MER) contained.

Meanwhile, due to being housed within Scotiabank, DXMC also quietly becomes the first majority crypto ETF to be issued by a major Canadian bank.

If DXMC’s relatively minimized MER, ported-in crypto expertise and trusted benchmarking have essentially established a template, it’s one that Scotiabank’s peers are likely to trace in the near term.

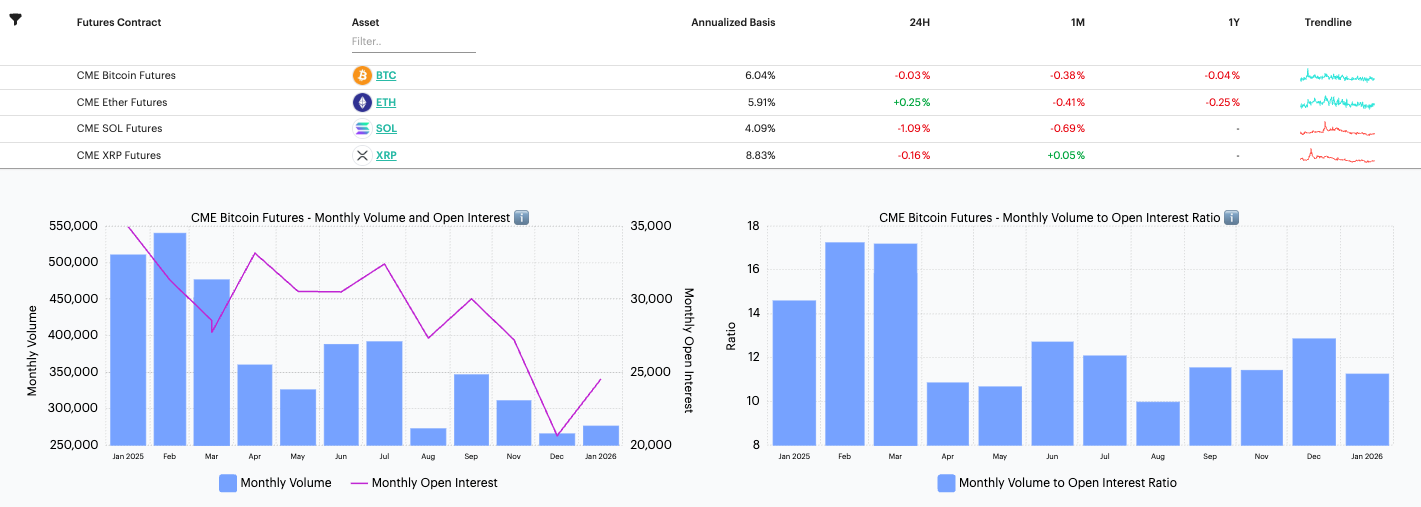

Meet Our New CME Bitcoin Basis and Options Screeners

We’ve added two freely available futures basis and options analytics, based exclusively on CME crypto contract volume and open interest.

CF Benchmarks has expanded its public analytics offering with two new derivatives pages: a Bitcoin Basis Screener and a CME Bitcoin Options Screener.

As CF Benchmarks is the sole provider of regulated settlement rates for CME crypto contracts, readers have for some time already been able to explore the CME Bitcoin options volatility surface in granular detail, with our fully directional 3-D visualizer.

Now, we've added dashboards for in-depth analysis of CME Bitcoin Open Interest and Volume, and multiple configurations of the CME futures basis – for all crypto futures available for trade at the venue. Both dashboards are updated daily, making the market easier to inspect, without requiring users to build these view themselves.

Every Basis, Multiple Views

The Basis Screener tracks futures basis across CME Bitcoin, Ether, SOL and XRP contracts. It begins with a comparative snapshot of annualized basis across contracts, then places that signal alongside monthly volume, open interest and the ratio between the two. As such, seen in context, the dashboard offers a cleaner view of carry, leverage demand and the shape of participation in listed crypto futures.

For instance, at the most rudimentary level, these views enable anyone to discriminate between a move in annualized basis accompanied by rising open interest and one that appears in thinner trading. A steep curve with broad participation suggests a different signal than a similar curve supported by lighter activity. The screener makes such distinctions easier to see by bringing pricing, activity and positioning onto one page.

CME BTC Options Unmasked

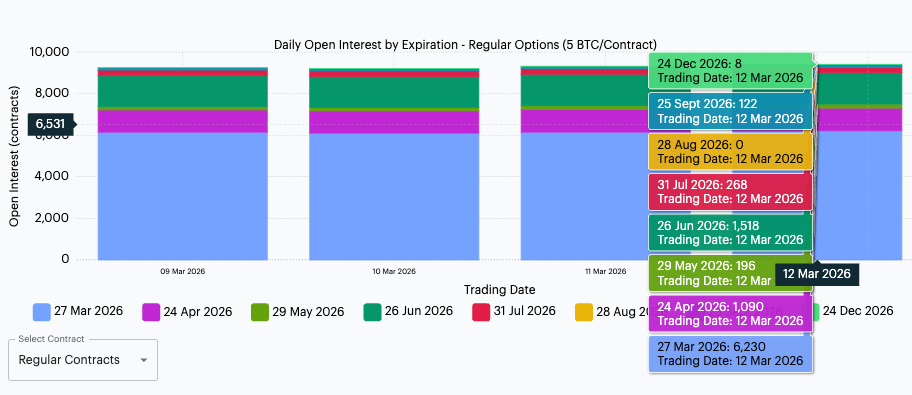

The CME Bitcoin Options Screener extends that logic into the primary institutional BTC options chain. This dashboard tracks daily and monthly volume and open interest, with filters for date, contract type and contract size, while breaking open interest out by expiry, so users can see where positions are accumulating across the maturity curve. These views enable easier identification of concentrated activity, and reveal which expiries are carrying the most weight.

It's worth noting that the page is also built to be interrogated rather than merely viewed. Individual maturities can be inspected directly, with the chart surfacing contract counts for specific expiries on interaction. Around larger expiry dates or more volatile trading periods, that makes the screen materially more useful than a static aggregate.

The screenshot below shows how contract-level detail is revealed through interactive inspection of the Daily Open Interest module.

To be clear, these new dashboards don't replace the deeper work done on trading desks or by specialist research teams, though they do put useful derivatives structures into public view in a clear format, that any user can easily inspect.

Brief Signal, Fast Structure for CFTC + SEC

A CFTC-instigated Joint Harmonization Initiative with the SEC, is worth keeping tabs on.

Coordinated

If Michael Selig’s early posture at the CFTC looked like regime-change signaling, he’s quickly shifted the narrative on to concrete steps, with the inking of a Memorandum of Understanding for the coordination of oversight across areas of overlapping CFTC and SEC authority.

Precipitated primarily by the simmering wider debate about the regulation of digital assets (amid presumed inter-agency spats too, under their prior leadership) the new Joint Harmonization Initiative will span rulemaking, examinations and enforcement.

Workstreams are now in motion to address key pivot points like product definitions, clearing and collateral, dually registered venues and intermediaries, reporting, and a “fit-for-purpose regulatory framework” for crypto assets and other emerging technologies.

Resolution in Sight, but no CLARITY yet

Following on from Selig’s establishment of the Innovation Advisory Committee (IAC) last month, the agreement points to a more favorable current regulatory direction in Washington than stalled progress of the CLARITY/markets structure Act might suggest.

The initiative helps operationalize the IAC and could yet pave the way for a genuine resolution of the tangible muddle that crypto counterparties sitting across spot, derivatives and tokenized products have navigated for years – including mismatched definitions, duplicated registrations and overlapping supervisory demands.

While there’s little sign (as yet, says Reuters) of a break in the holding pattern that CLARITY/market structure has been in for around two months, at least the SEC-CFTC relationship is moving from broad alignment in tone to active coordination in practice. That’s constructive at the margin for institutions building inside the U.S. regulatory perimeter.

BlackRock’s iShares Staked Ethereum Trust ETF sees Solid Debut

CME CF Ether-Dollar Reference Rate - New York Variant (ETHUSD_NY) is the benchmark for BlackRock’s first staking ETF.

BlackRock Enters Crypto Staking

CF Benchmarks congratulates BlackRock on the successful listing of its iShares Staked Ethereum Trust ETF (ETHB) a further step forward for the crypto asset class, as the largest investment manager in the world launches its first product providing exposure to staking rewards.

Solid Debut

With reported first-day trading volume (on March 12th, 2026) above $15 million, ETHB exhibited a solid opening for a newly listed crypto ETF in current market conditions, indicating firm demand.

ETHUSD_NY Again

BlackRock has notably opted to use the regulated CME CF Ether-Dollar Reference Rate - New York Variant (ETHUSD_NY) – published and administered by CF Benchmarks – for valuation of ETHB’s underlying Ether exposure, a continuation of the partnership between the world’s largest asset manager, in terms of assets under management (AuM), and the largest provider of crypto indices, as measured by assets under reference (AuR).

Utilization of ETHUSD_NY extends an established relationship between BlackRock and CF Benchmarks across digital asset investment products, including iShares Bitcoin Trust ETF (IBIT), iShares Ethereum Trust ETF (ETHA) and iShares Bitcoin ETP (IB1T) all of which deploy regulated CF Benchmarks indices for their reference prices.

By embedding ETHUSD_NY within ETHB, BlackRock is expanding its Ether ETF format to include staking, while retaining a benchmark architecture already embedded throughout its digital asset product suite. Separation of the Ether price valuation and Ether staking rewards functions affords the clearest possible discrete visibility and accuracy into the valuation of ETHB’s underlying asset.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.