Mar 04, 2026

CF Benchmarks Newsletter Issue 101

- CF Benchmarks-Powered xStocks Surpass $25 Billion

- CFB Analysts' Report on Crypto ETF Holdings: Advisors Still Buying

- CF Benchmarks' Factors Research Published by Springer

Clockwork

As soon as the bottom fell out of the crypto market last autumn, the recent 13F season was set up to be a particularly over-scrutinized one. Especially as it would be the first to offer a window into how new holders of institutional crypto entitlements would behave under the sustained pressure of a market downturn. At publication time, Bitcoin had advanced above the $60k-handle lows that becalmed it for weeks, enabling the CME CF Bitcoin Reference Rate - New York Variant (BRRNY) - most liquid institutional price for spot - to print $68,351.53, while it's streaming variant, CME CF Bitcoin Real Time Index (BRTI) indicated $73,542.88. Promising. But with the bulk of losses booked in the preceding quarter, the structural downturn had predictably translated into ETF share sales equating to some 20,000 worth of Bitcoin, by the time the quarterly tallies shown by statutory form 13F data rolled around. There’s frequently something of an ‘information vacuum’ effect surrounding flows between these quarterly data dumps. Typically, for listed products with enhanced public, media and broader financial following, this stokes fervent and theoretical speculation; sometimes spanning from the 4Chan-esque to the surprisingly erudite. If not convincing, certainly thought provoking. Example from the CIO of ProCap Financial, Jeff Park (formerly, at Bitwise):

Everyone is asking: "Is Jane Street why Bitcoin isn't at $150k?"

— Jeff Park (@dgt10011) February 25, 2026

As expected, the answer is trickier than the question. But it's also more structurally unsettling than the conspiracy theory itself—and once you understand the actual mechanics, you won't be able to unsee them👇 pic.twitter.com/iLEeJpDeo4

Answering his own question in the accompanying tweet though, Park points out: “As expected, the answer is trickier than the question. But it's also more structurally unsettling than the conspiracy theory itself.” On the off-chance you’ve not yet had the pleasure, here’s Coindesk’s coverage of said conspiracy (Bitcoin's 10 AM Dump).

That nod to the importance of keeping a sense of reality was echoed by Bitwise CIO Matt Hougan.

The conspiracy theories are wild. First it was Binance and then it was Wintermute and then it was an unknown offshore macro hedge fund and then it was paper bitcoin and. today it is Jane Street and next week it will be someone else.

— Matt Hougan (@Matt_Hougan) February 26, 2026

The real reason bitcoin is down is that a…

If only some level-headed verified market practitioners would take the trouble to gather the best data available that could help shed light on the real dynamics of U.S. crypto ETF flows. And consequently what can justifiably be deduced about the psychology, motivations and strategies of registered holders.

Surprisingly, although quarterly 13F releases precipitate fresh waves of commentary, there’s usually little to no institutional-standard coverage on what they tell us about crypto ETFs.In our research team’s recent report, ‘Tracking Bitcoin's Flows’ Head of Research Gabe Selby, CFA, and Research Analyst Mark Pilipczuk analyze the end-2025 quarter’s statutory holdings disclosure, unearthing fact-based insights that most will find more interesting, solid, actionable, and—crucially—price-constructive than theories in the wild.

Click here to read the report now, or scroll for our showcase below.

Also, in this edition:

- Deepening digital assets participation by CME amid signals it’s considering deployment of a blockchain. The looming launch of 24-hour crypto trading remains the main banner for now

- Recently installed CFTC chair Michael Selig’s first major initiative is the Innovation Advisory Panel, packed with crypto heavyweights. His first big legal tangle could also touch crypto as he tells states pushing back against CFTC-regulated prediction markets he'll see them in court

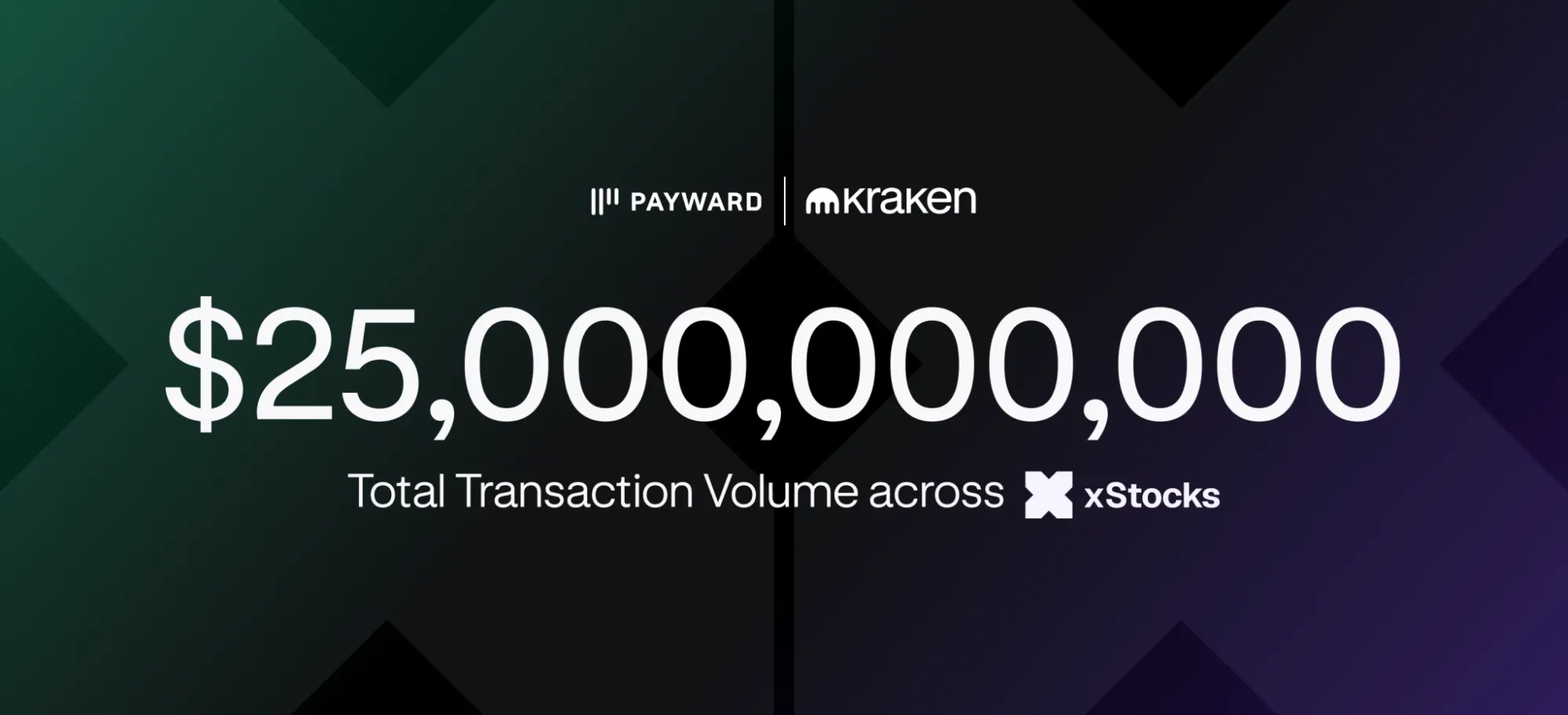

- CF Benchmarks’ regulated index methodology is the engine powering Kraken’s xStocks, which, recently passed the $25 billion-transaction volume milestone. Adjacently, Kraken's LCAP DTF perp, which tracks our CF Large Cap index, enters the regulated perimeter with a listing on Kraken MTF

- What better accolade for a research-driven outfit like CFB, than for our paper—A Factor Model for Digital Assets—to be rigorous enough for publication in an academic journal? Meanwhile, a second piece spotlighting our CF Factor Intelligence suite showcases how live CF Factor Data can be deployed for real-world exposure-mapping and strategic implementation

CME Crypto Trading goes 24/7 in May

After CME's announcement last year that its regulated cryptocurrency futures and options (which all settle to CF Benchmarks indices) will be available for trading 24 hours a day, seven days a week, it's set the launch for May 29th, pending regulatory review. The date emerged in a recent analysts' call which also included an update on its tokenized cash deal with Google. Chairman and CEO Terrence Duffy took the opportunity to drop adjacent headline-grabbing comments about a possible 'CME Coin'.

"So not only are we looking at tokenized cash, obviously, we're looking at different initiatives with our own coin that we could potentially put on a decentralized network for other of our industry participants to use"

CME Group Chairman and CEO Terrence Duffy, quoted in Decrypt.co

With Google's Universal Ledger initiative announced last March, and only slated for a roll out later this year, a blockchain open for CME clients to interact on will presumably take at least as long to pass internal and external committees - once a decision on viability's been made.

{kind=link}

Selig's Crypto-Tinged Mission

CFTC chair's first high-profile initiative maintains regulatory regime-change signaling

Crypto Mold

While Michael S. Selig's December 2025 confirmation as CFTC chair finally filled an unusually protracted and broad leadership gap at the Commission (Acting Chair Caroline Pham was its sole Commissioner for most of 2025) it's taken till recent weeks for clear signals of the likely first steps under new management to emerge.

With an interim role as chief counsel to the SEC’s crypto task force, there was little doubt that the former representative of clients like eToro and blockchain-focused VC, Paradigm (when Selig was a partner at Willkie Farr & Gallagher) would be directionally in a similar mold to SEC chair Paul Atkins. Meanwhile his CFTC bio casts him as harmonizer of SEC/CFTC’s regulatory regimes, while serving as SEC counsel, when he also helped “modernize the agency’s rules to reflect new and emerging technologies, and put an end to regulation by enforcement.”

Still, the long and the circuitous path to Selig’s nomination (an earlier nominee was withdrawn), amid disparate progress versus the SEC, which pulled ahead with a raft of initiatives in the interim (Generic Listing Standards, in-kind for crypto ETFs, innovation exemption proposals, etc.) maintained some uncertainty around whether the commodities regulator would be equally emphatic on modernization. The CLARITY Act/market structure bill impasse hasn't helped. The bill is supposed to be pivotal for the division of SEC/CFTC roles.

Innovation Team

In the end, Selig’s first high-visibility initiative is an Innovation Advisory Committee (IAC) – actually, a renaming of the former Technology Advisory Committee. A comprehensive roll call of heavyweights announced last month includes Terry Duffy (CME), Arjun Sethi (Kraken), Adena Friedman (Nasdaq), Brian Armstrong (Coinbase), Frank LaSalla (DTCC), Jeff Sprecher (ICE), David Schwimmer (LSEG), plus representatives of Cboe, Uniswap, Chainlink, Anchorage, Bullish, Grayscale, Kalshi and Polymarket.

From the accompanying statement: “The IAC’s work will help ensure the CFTC’s decisions reflect market realities so the agency can future-proof its markets and develop clear rules of the road for the Golden Age of American Financial Markets.”

At a minimum, this brain trust can provide the practical (and perhaps optical) pathways for the commission to move ahead with banner priorities flagged in ‘project crypto’:

- The reduction of mismatches over regulation of ‘novel’ intermediaries (chiefly. crypto platforms)

- Clearing the way for spot crypto trading on futures exchanges

- Offering a path for certain overseas crypto exchanges to legally offer derivatives to U.S. traders

- With CME crypto exposure soon to be available around the clock (see above) the push to make CFTC rules truly workable for 24/7, globally continuous markets (operational resilience, margining/liquidation expectations, supervision coverage) is set for added impetus

- Tokenized collateral: completion of a pilot program launched under Acting Chair Caroline D. Pham, testing the use of certain digital assets, (BTC, ETH, USDC, et al) as collateral in derivatives markets

Prediction Showdown

Meanwhile, Selig’s most vigorous reaction to pertinent events on his watch so far relates CFTC-regulated prediction market operators, like Kalshi and Polymarket. Many are facing an at least two-pronged challenge. On the one hand, opposition from Casino operators, native American tribes and state gambling regulators, pushing back against these firms’ ability to operate under federally regulated authority. On the other, consumer protection and regulatory standards campaigners are calling on policymakers and regulators to ensure the operators abide by the same standards as licensed sportsbooks.

Last month the CFTC filed an amicus brief (third-party opinion) in a Ninth Circuit case involving North American Derivatives Exchange (AKA Nadex, one of the oldest event contract markets) and the State of Nevada, asserting “exclusive jurisdiction” over event contracts. Selig in an accompanying video: “To those who seek to challenge our authority in this space … we will see you in court.”

CFB-Driven xStocks Surpass $25 billion; Switch to Always-On Perps

Exponential

To know Kraken’s xStocks is to trade Kraken’s xStocks. Ironically, given the increasingly exponential volumes of these tokenized equities transacted (by non-U.S. clients only) while xStocks are increasingly ubiquitous to buyers and sellers of the products, they’re only known indirectly—through brand recognition—by the majority of crypto participants who have yet to trade them.

xStocks are of course very evident on Kraken trading apps and platforms (also widely across DeFi and self-custody wallets) but those are currently the only places to witness xStocks’ 24/7-365 prices, powered by CF Benchmarks’ regulated Real-Time Index (RTI) methodology.

In under eight months xStocks have in fact now become the largest interface for tokenized equities, with $25 billion in total transaction volumes recorded across centralized and decentralized exchanges, and as DeFi mint/redemption activity.

And with new assets listed every month, these fully collateralized tokenized stocks are likely to maintain their leadership of the rapidly expanding market, where 8 out of the top 11 tokenized equities owned by unique holders are xStocks. They also account for 68% of the top 25 tokenized stocks owned by unique holders.

Always On

The roll-out of Kraken perpetual futures on these tokenized underlyings (the always-on switch) underpins that lead in participation terms. As the first ever tokenized-equity perpetual futures—also backed by CFB’s regulated Real-Time Indices — it means our transparent, high-integrity, high-reliability pricing now touches the most liquid traded equity indices in the world—via SPYx (S&P 500), QQQx (Nasdaq 100) and also spot gold via GLDx—plus many of the same heavily traded U.S. equities available through underlying xStocks, e.g. NVDA, AAPL, GOOGL, TSLA, HOOD, MSTR, and CRCL.

Kraken MTF, LCAP, and Perp Stack

Adjacently, Kraken’s recently listed LCAP perpetual futures contract, which tracks CF Benchmarks’ CF Large Cap Index via Reserve Protocol’s LCAP DTF, has now fully entered the regulated perimeter. It’s been listed on the Kraken MTF, unlocking access to the tokenized LCAP basket for regulated EU-domiciled institutional investors for the first time.

Click below to read about the LCAP MTF launch.

CFB’s Factor Model is now a Chapter in a Math Journal

CF Benchmarks’ ‘A Factor Model for Digital Assets' paper was published by Springer Nature, placing our factor research within a formal academic standard.

CF Benchmarks Leads Crypto Factors Research

As surprising as it may seem, CF Benchmarks has conducted one of the longest-running programs of published research into factor-based investing for digital assets. It began with an empirical analysis of validated crypto data sources for the investigation of factors applicable to the digital asset class. This research was published within the paper A Factor Model for Digital Assets, in December 2024. Most crucially, the model isolated the presence and confirmed the robustness of at least 6 factors within the digital asset class – Size, Value, Momentum, Growth and Liquidity – essentially establishing the first comprehensive institutional-grade factor model for digital asset investing.

The CF Factor Intelligence product suite, including our factor framework and the CF Factor Data Series, a quantitative data set enabling the capture of discrete performance components attributable to given factors, was rolled out from mid-2025.

Most recently, the increasing maturity of the data set has begun to enable longer-run research in the form of long-only portfolio management case studies.

Click below to read the first two of these pieces.

Academic Standard

Meanwhile, in a sign that further corroborates the rigorous standards of the CF Factors research methodology and our factor data set, ‘A Factor Model for Digital Assets’ has been published by Springer Nature as a chapter in the latest edition of Mathematical Research for Blockchain Economy, a series of academic journals.

The edition can be purchased from Springer Nature at the link above. Alternatively, the CF Benchmarks paper is freely available as a PDF download from our website.

Additionally, readers can now stay up date with how CF Factors are evolving in the market with our new weekly report series Factor Friday. Click below to read the latest report and subscribe to the series.

CF Benchmarks Analysts Flip the Bitcoin ETF Holders Script

We showcase Tracking Bitcoin’s Flows, a widely circulated research report based on 13F filings, by the CF Benchmarks Research team – Head of Research Gabe Selby, CFA, and Research Analyst Mark Pilipczuk.

Bitcoin’s emphatic collapse into the end of last year stoked active and widespread debate among investors about the origins of the BTC bear and reasons why it’s largely persisting, even as broader risk markets exhibit signs of relative resilience.

As we’ve seen, a rise in theories – most of them not particularly evidence-based – has been one of the most fascinating outcomes of the downturn. The term “wild” keeps coming up in more level-headed assessments of these takes.

The recent release of statutory 13F form data for the third quarter—filings by large investors detailing their holdings—presents the best opportunity since the downturn began for a more fact-based examination. In turn, it can pave the way for more reliable interpretations of the motivations behind the selling pressure.

Fact vs. Fiction

At an absolute minimum, Selby’s and Pilipczuk’s report separates what filings can show (quarter-end holdings) from what they can’t (intra-quarter timing, intent, non-filer activity). Worth noting in light of the space’s appetite for unmoored speculation: the distinction matters because crypto ETF narratives tend to move faster than evidence.

For example, one implicit takeaway: whilst observers often set much store to the concept of ‘ownership’—in the ETF context it’s often more nuanced; and can have a strong element of intermediation.

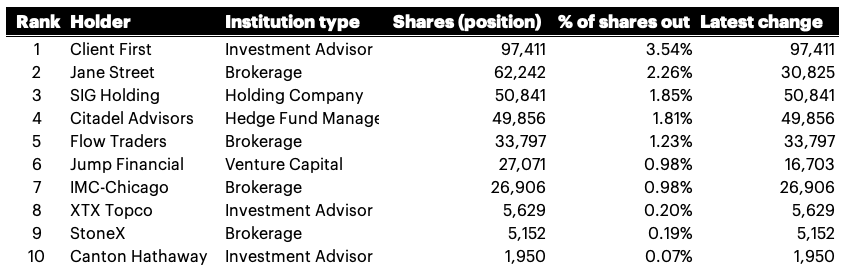

Below is a reconstructed top-holder table for ProShares UltraShort Bitcoin ETF (SBIT) one of the most actively traded inverse, leveraged, futures-linked BTC funds. (You can find the original screenshot on which the table is based in our analysts’ report, here.)

{kind=link}

Figure 1 – Top ProShares UltraShort Bitcoin ETF (SBIT) holders as of 31/12/2025 (13F disclosures)

Note that the top 4 holders accounted for approximately 9.46% of shares outstanding at that time. A fair amount of concentration in just four names.

Also note that the ‘short’ list above is dominated by market makers and trading firms (Jane Street, SIG, Citadel, Flow Traders, Jump, IMC, XTX). The composition is a reminder that inverse/leveraged bitcoin ETF wrappers often function as tools of facilitation: inventory management, hedging, and client flow. In other words, short exposure and hedging capacity exist in ETF form, and are actively intermediated. There’s no durable end-investor view on bitcoin to be gleaned from these alone.

Click below to read more insights from the complete report.

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.