May 04, 2026

CF Benchmarks Launches CF Bitcoin Compounding Basis Index: BTC Exposure With a Basis Overlay

Our new CF Bitcoin Compounding Basis Index (CFCMCBI_BTC) measures spot Bitcoin performance alongside systematic exposure to the CME futures basis.

Introducing the CF Bitcoin Compounding Basis Index (CFCMCBI_BTC)

CF Benchmarks is excited to introduce the CF Bitcoin Compounding Basis Index (CFCMCBI_BTC) a measure of spot Bitcoin performance alongside returns from a rolling basis program in CME Bitcoin futures.

CFCMCBI_BTC is a compounding index because returns accrue directly to the current index value.

As institutional participation in digital assets evolves to reflect demand for more diversified forms of return, the CME Bitcoin futures basis has become an increasingly active part of the market structure, shaping carry, relative value, and the economics of listed and structured exposures.

As such, to ensure that the same standards of transparency, replicability and integrity engendered by CF Benchmarks’ measures of spot Bitcoin are maintained within a strategy combining the Bitcoin basis with underlying exposure, CF Benchmarks has introduced the CF Bitcoin Compounding Basis Index.

BTC + CME BTC Basis

The index is designed to reflect spot Bitcoin performance plus the return from a systematic basis overlay in CME Bitcoin futures. The aim is to achieve constant exposure to the basis. Therefore, the overlay is short in contango regimes and flips long during backwardation.

In practical terms then, CFCMCBI_BTC is intended to be the benchmark of BTC exposure when that is combined with a basis overlay, rather than a simple measure of spot alone. The CF Bitcoin Compounding Basis Index is the first transparent, replicable and regulated Bitcoin benchmark with an integral overlay of the CME Bitcoin basis.

Capturing Bitcoin’s Basis

In futures markets, basis is the premium or discount embedded in a futures contract relative to spot. When futures trade above spot, the market is in contango. When they trade below spot, it is in backwardation.

For institutions active in both Bitcoin’s spot and futures markets, the spread is a distinct component of the return profile attached to Bitcoin exposure. This means that it is a material determinant of how products and strategies related to the Bitcoin basis need to be structured.

This is the need that the CF Bitcoin Compounding Basis Index addresses. Rather than market participants having to devise customized and essentially non-standardized solutions for capturing the Bitcoin basis alongside spot exposure, our compounding basis index turns the strategy into a rigorously tested, replicable and high-integrity benchmark of a defined Bitcoin return profile.

What the index measures

The index combines spot Bitcoin performance with a systematic futures-basis overlay. The constant underlying Bitcoin exposure is measured using CF Benchmarks’ CME CF Bitcoin Reference Rate (BRR). BRR is the most liquid, regulated benchmark for Bitcoin risk settlement, being the reference price utilized for settlement of CME Bitcoin futures and options.

This architecture is a central distinction for CFCMCBI_BTC. The index is not simply another Bitcoin price gauge, and it is not a standalone basis series detached from spot exposure. It is a benchmark designed to measure spot Bitcoin performance together with the return contribution of a rules-based basis overlay.

In this way, CFCMCBI_BTC provides the market with a benchmark for a return profile that sits beyond outright beta alone. It also gives issuers, allocators, and benchmark-aware managers a cleaner way to describe and reference a type of Bitcoin exposure that has become increasingly familiar in institutional settings.

Benchmark Design Fundamentals

The methodology is designed to be systematic and transaction-based rather than discretionary, as outlined below:

- The implied basis is derived from observed CME Bitcoin futures transaction data during a 60-minute TWAP window

- The calculation uses a volume-weighted median approach across six 10-minute partitions

- The index rolls gradually over three roll steps

- The portfolio will ‘stand aside’ if the current front-month signal does not align with the majority sign of the previous five days.

Mechanics Matter

Those mechanics matter because they make the benchmark operationally legible. The process draws on observed CME Bitcoin futures transaction data, applies a transparent calculation framework, and uses a simple confirmation filter before entering a new position. The result is a benchmark designed to be transparent, replicable, and aligned with institutional expectations around methodology discipline.

The index is typically calculated at 4:00 p.m. London time*, using the CME CF Bitcoin Reference Rate (BRR) for its spot component, and CME Bitcoin futures inputs for the basis overlay. This combination keeps the benchmark anchored to a defined reference price for Bitcoin, while capturing the basis signal from the primary CFTC-regulated Bitcoin futures market.

*The index Calculation Time will be amended by the Index Administrator on days when the CME is maintaining limited trading hours for Bitcoin Futures.

Click here to read or download the complete CF Bitcoin Compounding Basis Index (CFCMCBI_BTC) Methodology Guide.

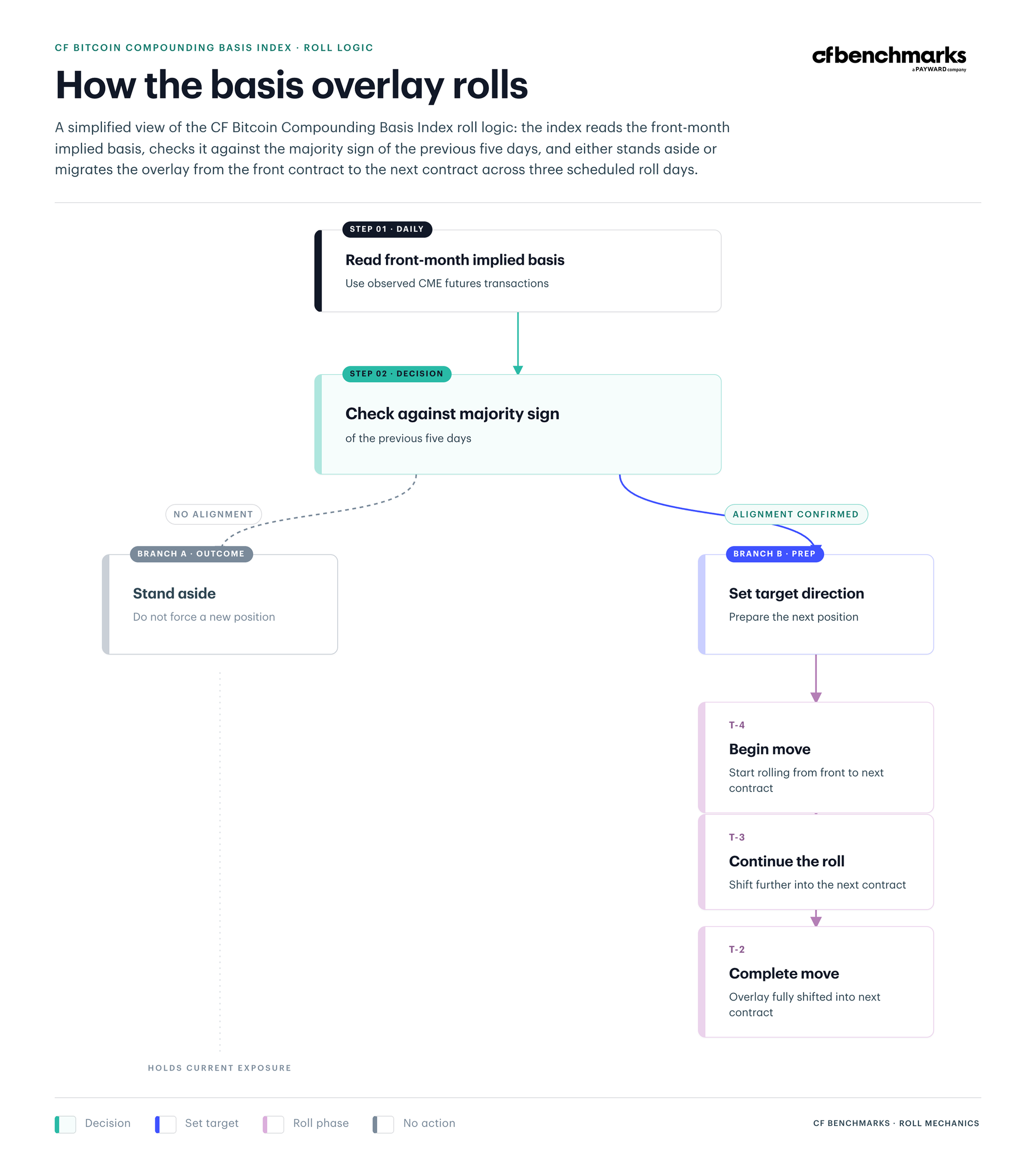

How the Overlay Rolls

The roll regime is an important part of the design because it keeps the methodology systematic without making it abrupt.

Ahead of expiry, the index first reads the front-month basis signal and checks it against the majority sign of the previous five days. If that signal is confirmed, the basis overlay is then migrated from the front contract to the next contract across three scheduled roll days. If the signal is not confirmed, the index ‘stands aside’ rather than forcing a new position.

That conditionality matters because the index does not jump its overlay from one contract to the next in a single move. It determines direction first, then transitions in stages. That makes the methodology easier to understand as a benchmarking tool and it avoids treating outlier basis signals as entry triggers.

A simplified summary of the strategy is shown in the diagram below.

Figure 1 - CF Bitcoin Compounding Basis Index – simplified roll regime

Institutional Deployment

A benchmark like this is useful because it provides a reference point for a Bitcoin return profile that is already familiar in concept but has not always been available in clean benchmark form.

For issuers and structurers, that may mean benchmark infrastructure for products designed to deliver more than plain Bitcoin beta. For allocators and portfolio builders, it creates a way to distinguish outright BTC exposure from BTC exposure plus a systematic futures-basis component. For managers running benchmark-aware mandates or overlay strategies, it offers a transparent reference for a defined rules-based profile rather than a loose description of “basis capture”.

That kind of benchmark utility can matter at several stages of product and strategy development. It can help define the target exposure more clearly, support benchmarked product design, and provide a more precise frame for communicating how a strategy differs from spot-only Bitcoin exposure.

Conclusion: Benchmark for a Broader BTC Return Profile

The CF Bitcoin Compounding Basis Index (CFCMCBI_BTC) gives the market something more specific than another measure of Bitcoin’s spot price. It provides a benchmark for BTC exposure with a basis overlay, combining spot Bitcoin performance with a systematic CME Bitcoin futures-basis component inside a transparent, rules-based framework.

As institutional Bitcoin markets continue to differentiate between outright beta, carry, and more tailored forms of packaged exposure, TBC is an essential addition to the benchmark toolkit.

Discover More

Click the links below to learn more about the CF Bitcoin Compounding Basis Index (CFCMCBI_BTC)

The information contained within is for educational and informational purposes ONLY. It is not intended nor should it be considered an invitation or inducement to buy or sell any of the underlying instruments cited including but not limited to cryptoassets, financial instruments or any instruments that reference any index provided by CF Benchmarks Ltd. This communication is not intended to persuade or incite you to buy or sell security or securities noted within. Any commentary provided is the opinion of the author and should not be considered a personalised recommendation. Please contact your financial adviser or professional before making an investment decision.

Note: Some of the underlying instruments cited within this material may be restricted to certain customer categories in certain jurisdictions.

Changes to the Token Market Price Benchmarks Series - Market Prices – 21 July 2026

The Administrator has confirmed changes to the Token Market Price Family for the period 14 July 2026 to 21 July 2026.

CF Benchmarks

Softer CPI Reprices July Hike Risk & Lifts Digital Assets

Digital assets extended their recovery over the past week as cooler US inflation prints repriced Fed expectations; the bid was broad across the large cap indices, growth factor leadership returned, stablecoin funding repriced lower, and stress stayed isolated in names hit by token-specific news.

Mark Pilipczuk

Notice of the Demising of CF Dai-Dollar Settlement Price and Spot Rate

The Administrator announces that it will demise the CF Dai-Dollar Settlement Price (DAIUSD_RR) and CF Dai-Dollar Spot Rate (DAIUSD_RTI) which are members of the CF Digital Asset Index Family.

CF Benchmarks

By clicking Accept, you consent to CF Benchmarks's use of cookies.

Visit Cookie Settings to learn how CF Benchmarks uses cookies and to adjust your preferences.